TSMC Q1 2021 Process Node Revenue: More 7nm, No More 20nm

by Dr. Ian Cutress on April 15, 2021 7:00 AM EST

This week TSMC has disclosed its full quarterly financial results for Q1 2021. In those results the company often explains where the revenue demand is for its technologies, and the financial split the demand brings. This number is not correlated to wafer production (although TSMC provides an overall number too), given that smaller process nodes have a per-wafer premium, but it does indicate where the demand is in the market right now. As perhaps to be expected, 7nm takes top billing, however a couple of interesting numbers come out of the data.

The headline numbers from TSMC’s financial disclosures are that the company made $12.92 billion USD net revenue in Q1 2021, up 1.9% from quarter-to-quarter and up 25% year-on-year. This translates to a 52.4% gross margin, which is down 1.6% Q-on-Q and up 0.6% YoY. TSMC shipped 3.36 million wafers this quarter (based on 12-inch equivalent wafers, because some production is 8-inch), or about 1.12 million per month, 8% more per month than the 2020 average.

This quarter TSMC has hit record wafer production, some 50% higher than its recent Q1 2019 low point. In Q1 2019, TSMC had low demand for high-end smartphones, low customer demand due to oversupply/inventory digestion, and Q1 is typically lower seasonally anyway. But as we can see from the historical 5-year graph, traditional production for TSMC has been around 2.5-2.7m wafers per quarter.

It is only recently that TSMC is pushing out over 3m wafers per quarter, indicating a good shift in demand as we are seeing of late. This is buoyed by TSMC’s newest Fab 18 facility which went into 5nm risk production in Q2 2019, and at full production is expected to manufacture 1 million to 1.2 million 12-inch wafers per year.

This uptick in wafer shipments has had a net positive in net revenue as well.

We see a similar dip in revenue as we did with wafers in Q1 2019, but the recent highs from Q3 2020 onwards are set to continue, with TSMC making $12.92 billion USD for Q1 2021 with a 52.4% gross margin. TSMC indicates that the lower gross margin was partly down to a lower level of utilization in its fabs (likely for upgrades/repairs than lack of demand), as well as an unfavourable exchange rate. For perspective, TSMC holds $13.42 billion USD in net cash reserves, down from Q4 due to an increase in short-term loans and issuance of corporate bonds, but has a cash position of $23.47 billion USD.

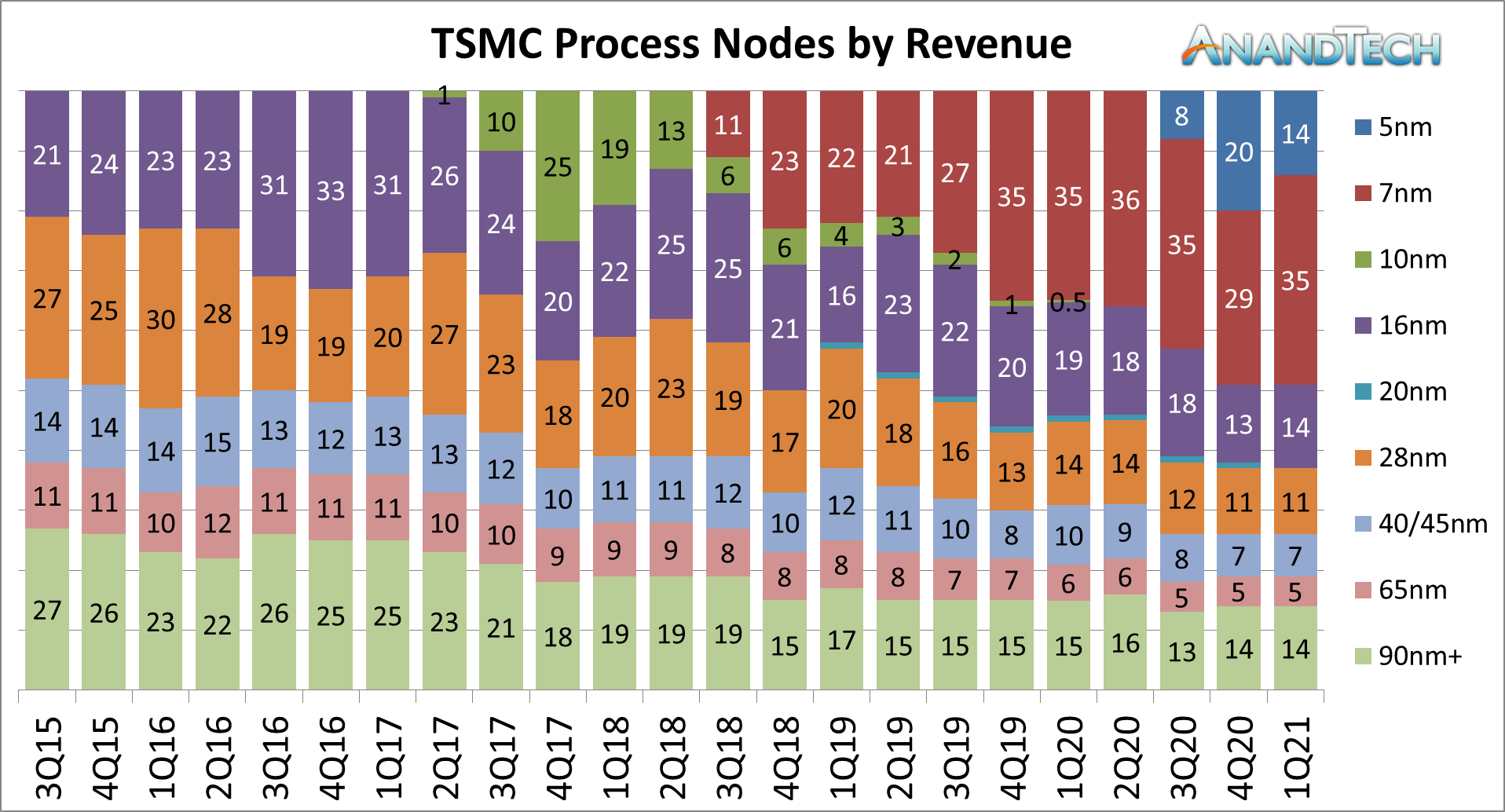

As for where the revenue comes from, for the second straight quarter, in Q1 2021 7nm and 5nm combined accounted for almost 50% of the company-wide revenue. 7nm actually increased its revenue share, while 5nm revenue reduced.

7nm accounts for 35% of all revenue, with 5nm now at 14%. This might seem odd, however TSMC has very few customers with 5nm designs, but plenty for 7nm, suggesting that TSMC is able to have customers bid against each other (along with increasing wafer output). For the last few quarters, reports about TSMC’s 7nm lead time for products, from order to production to shipment, have been extending due to the increased demand. Note that TSMC’s most advanced packaging technologies, such as CoWoS, are typically used in conjunction with 7nm or 16nm silicon, so those revenues are likely in those respective segments as well.

Recently TSMC has stated that it plans to spend $100B over the next three years to increase capacity leading-edge capacity, which includes the $25B-$28B it had already planned for 2021, with $12B of that going onto a factory in Arizona. To put that in perspective, TSMC’s Fab 15 which currently produces 12-inch wafers on 7nm, cost $9.3 billion in 2010, and has the capacity for ~100,000 wafer starts per month.

Revenue from 16nm is decreasing, now going below 15% for a couple of quarters, and showcasing that TSMC is making as much money from 16nm as it is from 5nm and 90nm+ older process nodes.

Also on this breakdown of process nodes, we can see that 20nm has bit the bullet, and now rounds to 0% of TSMC’s revenue. Both 20nm and 10nm are now listed at 0% as companies that produced hardware on these nodes are coming to the end of replacement life cycles for those products.

Demand for the older process nodes is still strong, with 28nm and above being 37% of the company revenue, which combined is more than 7nm revenue. Lots of fundamental electronics still require these process nodes, such as high voltage components, high thermal support/long life cycle hardening, or radio frequency silicon that is mature and low cost. Even TSMC’s interposer technology is manufactured on these process nodes, showcasing that the future is going to be a mix of old and new.

Also on TSMC’s disclosure is revenue by platform. The two major markets here are smartphone (45% by revenue) and high-performance computing (35% by revenue), which have consistently been about 80% of the total revenue for TSMC for over a year. The other 20% is taken up by IoT (9%), Automotive (4%), and others (7%).

Full details can be found on TSMC’s Investor Relations website.

From AnandTech’s perspective, we covered TSMC’s Tech Day 2020 disclosures in late August, covering the following topics:

- TSMC: We have 50% of All EUV Installations, 60% Wafer Capacity

- TSMC and Graphcore Prepare for AI Acceleration on 3nm

- Where are my GAA-FETs? TSMC to Stay with FinFET for 3nm

- 2023 Interposers: TSMC Hints at 3400mm2 + 12x HBM in one Package

- TSMC Expects 5nm to be 11% of 2020 Wafer Production (sub 16nm)

- TSMC’s Version of EMIB is ‘LSI’: Currently in Pre-Qualification

- TSMC Teases 12-High 3D Stacked Silicon: SoIC Goes Extreme

- TSMC Updates on Node Availability Beyond Logic: Analog, HV, Sensors, RF

- ‘Better Yield on 5nm than 7nm’: TSMC Update on Defect Rates for N5

- TSMC Launches New N12e Process: FinFET at 0.4V for IoT

- 3DFabric: The Home for TSMC’s 2.5D and 3D Stacking Roadmap

40 Comments

View All Comments

yeeeeman - Thursday, April 15, 2021 - link

Nice!nandnandnand - Thursday, April 15, 2021 - link

7nm should be a great "budget node" by the time 3nm lands (or a year after).shabby - Thursday, April 15, 2021 - link

Intel: *whimpers*nismotigerwvu - Thursday, April 15, 2021 - link

I knew the older nodes were profitable, but the sheer magnitude is astonishing! It's also interesting to see which processes hang around and become "legacy" and which ones fade away (or almost never really exist like 20 nm, but that wasn't just TSMC).dwillmore - Thursday, April 15, 2021 - link

Maybe I should have replied to your comment with my request for a 'process lifetime' table as we're clearly thinking along the same lines.smalM - Thursday, April 15, 2021 - link

https://fuse.wikichip.org/wp-content/uploads/2020/...at_clucks - Tuesday, April 20, 2021 - link

I wonder who are their 110/130nm customers. It's showing impressive cyclic regularity year after year.1_rick - Thursday, April 15, 2021 - link

A lot of microcontrollers, especially ARM, are on ~40 and 90nm nodes. ST Micro's STM32 series, for example. Microchip's fabs (they produce the ATMega lines seen in Arduinos, and a couple of lines of ARM Cortex-M (Adafruit is big on them, for their Arduino-like Feather line) chips, seem to be 250 and 150nm or so, according to Wikipedia.JoeDuarte - Friday, April 16, 2021 - link

The margins reported are false. They make big margins, but not that big, and the "net revenue" that Cutress reports is just revenue. There is such thing as "net revenue" in financial reporting.dotjaz - Sunday, April 18, 2021 - link

You know very little about financial reporting do you? Net revenue is tied to gross margin. It's reported when your revenue is generated from commissions, ie you don't pay your suppliers unless the item is sold.It's not very relevant to TSMC, but it is a very real accounting terms. TSMC is reporting Gross Revenue.