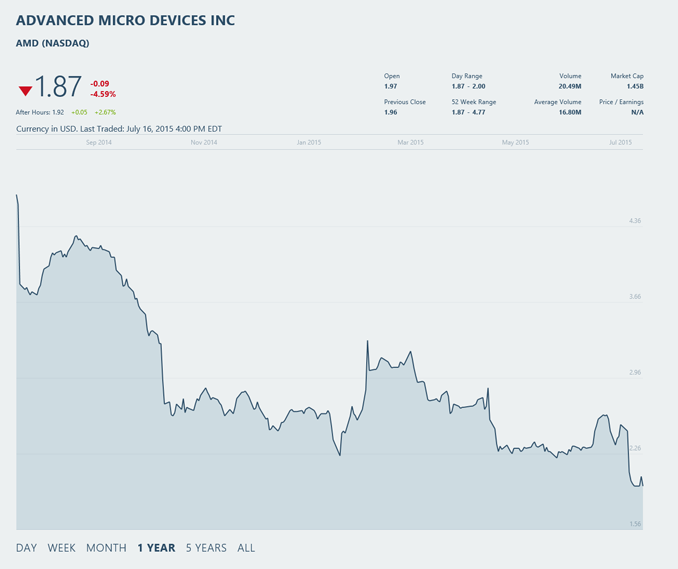

AMD Posts Q2 2015 Results: Revenue Falls Once More

by Ryan Smith on July 16, 2015 7:40 PM EST- Posted in

- CPUs

- AMD

- GPUs

- Financial Results

As financial week rolls along this week, today AMD announced their second quarter 2015 financial results. Earlier this month ahead of today’s announcement the company issued a warning for their Q2 earnings, significantly revising down their projections for revenue and gross margin. As a result of AMD’s earlier warning today’s announcement doesn’t have too many surprises in it, but it’s none the less an important and unfortunately painful quarter for AMD.

| AMD Q2 2015 Financial Results (GAAP) | |||||

| Q2'2015 | Q1'2015 | Q2'2014 | |||

| Revenue | $942M | $1.03B | $1.44B | ||

| Gross Margin | 25% | 32% | 35% | ||

| Operating Income | -$137M | -$137M | $63M | ||

| Net Income | -$181M | -$180M | -$36M | ||

| Earnings Per Share | -$0.23 | -$0.23 | -$0.05 | ||

For the quarter AMD recorded $942 million in revenue. This marks the first time in quite a number of years that AMD’s quarterly revenue has dipped below $1 billion, indicating the challenges the company has faced as the PC market continues to be soft and AMD CPU/APU sales have declined. All told the company’s revenue has dropped 8% compared to Q1, and on a year-over-year basis it has dropped 35%

Unsurprisingly given AMD’s low revenue, operating and net income for the quarter were both losses. On a GAAP basis operating income was a $137 million loss while the net loss was $181 million, both of which are virtually unchanged from AMD’s Q1’15 performance. Meanwhile on a non-GAAP basis the operating income loss was $87 million and the net loss $131 million, both of which were accelerated versus the last quarter. On a year-over-year basis both GAAP and non-GAAP show a significant increase in losses versus Q2’14.

| AMD Q1 2015 Financial Results (Non-GAAP) | |||||

| Q2'2015 | Q1'2015 | Q2'2014 | |||

| Revenue | $942M | $1.03B | $1.44B | ||

| Gross Margin | 28% | 32% | 35% | ||

| Operating Income | -$87M | -$30M | $88M | ||

| Net Income | -$131M | -$73M | $38M | ||

| Earnings Per Share | -$0.17 | -$0.09 | $0.05 | ||

Meanwhile AMD’s gross margin has taken a hit as well. The GAAP gross margin is just 25%, while the non-GAAP gross margin is slightly better at 28%, the difference being due to AMD's $33 million charge to move 20nm products to FinFET. Both metrics are well below the kind of 30-35% margins AMD wants to sustain in the long run.

In discussing their financial results for the quarter, AMD cited the soft PC market as the biggest factor pulling down the company’s performance. Historically in turn Q2 is typically the softest quarter for technology companies, however in AMD’s case it has been especially soft. With AMD’s single biggest product line being APU sales and with those sales weaker than expected, it has significantly impacted AMD’s bottom line.

Of particular note, AMD is stating that they believe the impending launch of Windows 10 was a significant factor in their weak sales for the quarter, as consumers held back on buying new systems until the new OS is out, and OEMs held back in releasing newer designs in order to align those releases with the new OS. This has particularly impacted Carrizo, AMD’s latest generation mobile APU, given that it was released only two months before the launch of Windows 10. AMD is expecting that mobile sales will rebound once Windows 10 launches, though as we’ve seen with the launch of Windows 8 in 2012, that isn’t necessarily a given.

| AMD Q2 2015 Computing and Graphics | |||||

| Q2'2015 | Q1'2015 | Q2'2014 | |||

| Revenue | $379M | $532M | $828M | ||

| Operating Income | -$147M | -$75M | -$6M | ||

Breaking down AMD’s revenue by business, soft APU sales pulled down the Computing and Graphics business overall, and led to Enterprise, Embedded, and Semi-Custom carrying a larger share of the company. Computing and Graphics revenue was down 29% over Q1’15 and a staggering 54% over Q2’14, primarily due to weak sales of notebook APUs, while graphics revenue was also down. Despite this the ASPs for both CPUs/APUs and GPUs were up on both a sequential and year-over-year basis, as while overall sales are lower, the prices of what AMD has sold has increased thanks to a richer product mix and the launch of the R9 300/Fury series at the tail end of the quarter.

| AMD Q2 2015 Enterprise, Embedded and Semi-Custom | |||||

| Q2'2015 | Q1'2015 | Q2'2014 | |||

| Revenue | $563M | $498M | $613M | ||

| Operating Income | $27M | $45M | $97M | ||

Enterprise, Embedded, and Semi-Custom on the other hand had a much stronger quarter, with revenue there increasing 13% sequentially, though year-over-year revenue was still down by 8%. As part of AMD’s long-term plans they are attempting shift more of their resources and revenue over to this business, so any kind of growth is welcome growth for the company. However for this quarter in particular AMD was not prepared for such a high ratio of revenue from this business group, with the lower margin of AMD’s semi-custom products dragging down the overall gross margin.

Finally, compounding AMD’s difficulties this quarter was the impact of their previously announced plan to move the rest of their in-development 20nm products to a newer FinFET node. This project resulted in a further $33 million hit to AMD’s books, driving up losses and decreasing gross margins. The good news for AMD is that this is a one-time charge, so they won’t have to pay for it again.

Looking forward, AMD’s projections for Q3 are that sales will pick up in both the Computing and Graphics business and the Enterprise, Embedded, and Semi-Custom business. AMD is expecting improved PC sales as a result of Windows 10 and Carrizo reaching the market – in particular shoring up the company’s poor notebook sales – while orders for semi-custom processors for the game consoles will pick up in order to build up inventory for Christmas. AMD expects overall revenue to be up 6% (+/- 3%) sequentially, though the non-GAAP gross margin is expected to come in at just 29%, which is below where AMD would like to be and means there’s a good chance AMD will be in the red again for Q3.

Longer term, the company is still working on bringing their expenses under control and better aligning them with revenue, a task that becomes harder after quarters like these, with AMD admitting that the profitability timeline for the company has been pushed out. As it stands AMD still has over $800 million in cash and equivalents on-hand, however the company has also mentioned that restructuring to further cut expenses is not off the table, and that the company is assessing the option.

Source: AMD Investor Relations

125 Comments

View All Comments

Michael Bay - Friday, July 17, 2015 - link

Looking at the current state of things, people were right to root for South.Owls - Saturday, July 18, 2015 - link

The current state of what? Are you that monumentally stupid to think slavery is something that should have stayed?Please go to stormfront and stay there

Michael Bay - Sunday, July 19, 2015 - link

Enjoy your gulags, coming soon.V900 - Friday, July 17, 2015 - link

They truly are the flat-earthers of the computing world...lyeoh - Sunday, July 19, 2015 - link

Think properly. You should be encouraging more AMD fanboys to buy more AMD products to keep AMD alive for longer. Someone has to buy AMD products so that Intel won't screw us as much, if it's not going to be you or me guess who else?3ogdy - Friday, July 17, 2015 - link

You're an utter joke. Fury X has almost the performance of 980Ti, beating it in VERY FEW exceptions. It is also priced as if it was an nVidia card - it also requires water cooling, it is hotter and less overclockable, it is marketed towards 4K, yet it only has 4GB of VRAM (vs 6GB on the 980Ti) - ALL of these while consuming 20% more power. Did I mention pump noise? Pump issues? All this to do what? TRY to match an nVidia card with blower-based cooling? What a fracking joke! What a fracking joke! For Fruck's sake!Anyone seeing ANY reason at all to buy any Fury card is a blind man. The R9 300 series? Well, they're the same R9 200 series cards with a bit of overclock that can easily be achieved on the R200 series. The point in buying anything other than APUs from AMD?

None. After the HUGE disappointment the Fury X is, let them go down if they can't get one damn thing right - this will mean higher prices on nVidia and Intel hardware, but hey...what can we do? Buy shit products when there are infinitely better alternatives?

beck2050 - Monday, July 20, 2015 - link

http://hexus.net/tech/reviews/graphics/84722-zotac...980 ti beating a Fury X by 15 to 30% BEFORE overclocking. It really crushes it. Even faster than a 295 with a single GPU and NO WATER required. With overclocking it's ridiculous. Fury X is very limited there anyway.

CiccioB - Friday, July 17, 2015 - link

Let me light some of obscure points that lead you to this limited and approximate view of the world:1. 290X didn't really beat anything. Do you really think that Titan and 290X played in the same league? In fact after a couple of weeks the 780Ti, which has been kept in a drawer for months, appeared. And the vertical price drop of 290X cards explained which victory that was. Titan's price didn't move of a single dollar... guess why.

2. Fury beats 980? Really? That's a miracle, my dear! A real miracle! Let's see... it consumes more and costs more, but most of all Fiji is 150% the die size of GM204 and even HBM can't manage the card to come to Maxwell efficiency. That (Fiji, not GM204) is the kind of product that is killing AMD. It should have been the Titan X killer, sold at premium price, giving a new vision to the company, free advertising, all sites speaking of this new product more modern and faster than competition, well distant from being able to use the same technology, making nvidia drop its prices and roll up their sleeves, but in the end was the usual disappointment that has to be sold with no gain margin just to have any appeal. With nvidia retaking their quiet sleep after a few seconds of noise.

Come on, be realistic. AMD's products line is under par with competitions, be it Intel or nvidia. They struggle to present something new every once in a while. And even when using the most of their resources, they fail (see Fiji, but also console APUs that are sold at no margins at all, WHY??).

Sorry, but this company is lead to fail in few months. All the markets it relies on are shrinking. High profitability ones they are no more. Lots of debts. And no valid products on horizon for still a few months.

I really hope they can survive until Zen is released, hoping it is such a good architecture that may convince me to return to AMD CPUs. But my hopes are thin. Really.

For GPUs, if they have not already created GCN v2 completely from scratch, they are already doomed.

Nagorak - Friday, July 17, 2015 - link

Their GPUs are still basically competitive. Even if slightly slower/more power use in some cases. They are in the same ballpark. New drivers could very well post Fury X above the 980Ti (at stock). The difference is small enough that it could happen. Will it? It remains to be seen. The same cannot be said about CPUs, which just aren't competitive at all.D. Lister - Friday, July 17, 2015 - link

"So, next time you look for the reasons to buy them over competition product, don't look up you arse, just check the numbers."Easy there champ. No need to get so emotional over whose toy is better. lol