Intel Q2 FY 2019 Earnings Report: Datacenter Drop

by Brett Howse on July 26, 2019 12:15 AM EST- Posted in

- CPUs

- Intel

- Financial Results

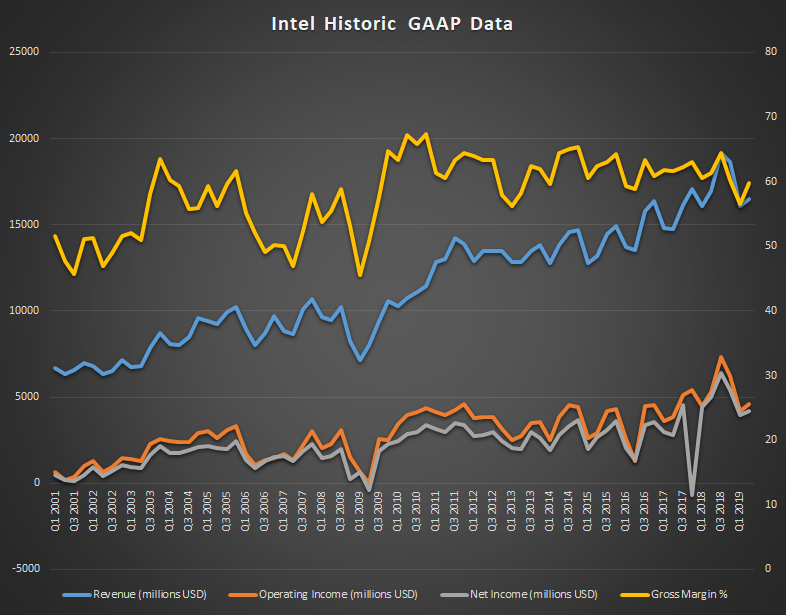

Intel announced their earnings for the second quarter of their 2019 fiscal year. Overall, revenue dropped 3% year-over-year to $16.5 billion, with gross margins still below the 60% that Intel likes to maintain, but at 59.8%, the are improved significantly over last quarter’s 56.6%. Operating income for the quarter was down 12% to $4.6 billion, and net income down 17% to $4.2 billion. This resulted in earnings-per-share of $0.92, down 12% from a year ago.

| Intel Q2 2019 Financial Results (GAAP) | |||||

| Q2'2019 | Q1'2019 | Q2'2018 | |||

| Revenue | $16.5B | $16.1B | $17.0B | ||

| Operating Income | $4.6B | $4.2B | $5.3B | ||

| Net Income | $4.2B | $4.0B | $5.0B | ||

| Gross Margin | 59.8% | 56.6% | 60.6% | ||

| Client Computing Group Revenue | $8.8B | +2% | +1% | ||

| Data Center Group Revenue | $5.0B | +2% | -10% | ||

| Internet of Things Revenue | $986M | +8% | +12% | ||

| Mobileye Revenue | $201M | -4% | +16% | ||

| Non-Volatile Memory Solutions Group | $940M | +3% | -13% | ||

| Programmable Solutions Group | $489M | +1% | -5% | ||

Over the last couple of years, it’s been the datacenter group that has been the sharp end of Intel’s growth, and it’s now the datacenter group that took the brunt of the slowdown. In fact, the PC-centric group at Intel managed to keep revenue more or less flat compared to last year, up 1% from Q2 2018, with $8.8 billion in revenue. Intel has seen high sales in their higher performance, and therefore higher margin, products, as well as customers purchasing ahead of possible tariffs. Intel also has finally started shipping 10 nm products in volume with expectations of holiday 2019 sales. The Client Computing Group had operating income of $3.7 billion this quarter, up from $3.2 billion a year ago, so despite Intel not executing on 10 nm as expected, they are still quite strong in the PC space even as competition has ramped up.

Intel’s Datacenter group experienced a revenue drop of 10%, with $5.0 billion in revenue for Q2. The biggest single drop was enterprise and government revenue, which was down 31%, but cloud also declined, although only 1% compared to last year, and the communications service provider segment was up 3%, offsetting some of the drops. Operating income for the Datacenter group was down more significantly though. Operating income was $1.8 billion, down 34% from a year ago.

Intel’s Internet of Things continues its rise, almost hitting the $1 billion/quarter threshold, and achieved a record quarterly revenue for Q2 with $986 million in revenue. This was up 12% from a year ago, with increased demand for higher performance processors driving the revenue gain. Operating income was up $51 million to $294 million as well. Mobileye revenue was up 16% to $201 million with an operating income of $53 million, up 20.4%.

Intel’s NAND group had revenue of $940 million in the quarter, down 13% due to “challenging pricing” and Intel continues to lose money on their NAND group, with an operating loss of $284 million this quarter, compared to a $65 million loss last year.

Finally, Programable solutions had revenue of $489 million, down 5% from last year with no explanation given. This group saw its operating income slashed almost in half compared to last year, coming in at $52 million for the quarter compared to $101 million a year ago.

Collectively, Intel’s PC group was up 1% and its Datacenter products were down 7%. Intel saw a 2% drop in notebook processor volumes, but average selling price was up 3%. Desktop processor volumes were down 11% compared to Q2 2018, but average selling price was up 5%. On the datacenter side, unit volumes were down 12% compared to Q2 2018, and average selling price was only up 2%.

Looking ahead to Q3, Intel is expecting revenues of around $18.0 billion, with earnings-per-share of about $1.16.

Source: Intel Investor Relations

16 Comments

View All Comments

Gondalf - Friday, July 26, 2019 - link

Thanks Mr Trump; tariff tariff tariff.......at the end IT companies suffer. A growing market is now a disaster, too bad because increasing the global volume there is space for all companies without loss in revenue. Well done (sarcasm), Intel AMD ARM IBM Nvidia and many others love you sooo much.Kevin G - Friday, July 26, 2019 - link

This is the impact of 10 nm delays.Data center decline is likely due to the arrival of Cascade Lake and its minor improvements over Sky Lake-SP. The big feature is Intel returning some performance from the security fixes being in hardware, a small clock speed bump and Optane memory support on select models. Oh and a price increase. There is no incentive to migrate, especially since Cooper Lake and Ice Lake are both due next year on a new socket with some real improvements. I'd expect the YoY declines to be present in the approaching quarters based on this alone.

The NAND group may actually start to improve as one of the few reasons to migrate to Cascade Lake is Optane DIMM support, a feature that Intel was hoping to launch alongside Sky Lake-SP. Intel also loosened the requirements for their Optane caching as it went no where as a high end premium feature. The biggest factor in their decline and potential grow moving forward is the competitive nature of the DRAM and other manufacturer's NAND pricing. Right now DDR4 spot pricing is low which makes the capacity/cost benefits of Optane DIMMs not that great (especially with performance being factored in). NAND pricing is actually volatile and with one of their competitors suffering a power outage setting back production, spot prices for the market may start to move upward which works into Intel's favor. Overall outlook isn't too good for this group but it isn't as bad as it was previously.

Programmable solutions, aka what was known as Altera, had its decline as they are suffering from the same 10 nm delays. Even before Intel acquired them, their high end line was to be manufactured on Intel's 10 nm process as Altera was a custom foundry client for them. A bit tin foil hat, but I wonder how much of that Altera acquisition was based upon Intel's own projection for missing Altera's time tables and how big the penalties would be in breaking the contract they had. It wouldn't be the only reason to acquire Altera (see the planned Xeon + FPGA announcement prior to the merger) but it could have been the tipping point. Intel is also facing very strong competition from Xilinx right now.

HStewart - Friday, July 26, 2019 - link

Keep in mind there total revenue basically close to same, costs are down. But client side (mostly laptops) are up.I think the biggest issue is simply that company's are keeping with existing equipment and not buying new equipment.

Qasar - Friday, July 26, 2019 - link

OR... maybe they are buying AMD based instead of inteljospoortvliet - Friday, July 26, 2019 - link

Could it be data centers are holding off purchases as the upcoming amd generation seems to move the goalposts so much? We will know in a few weeks... of course testing validation etc takes much more time but i assume the biggest players already have access to the amd epic 2 CPUs...Kevin G - Saturday, July 27, 2019 - link

There really is little reason to hold off if you need a new build except for budgeting purposes. While AMD may capture the performance crown in server once again if the Zen 2 desktops are anything to go by. However, in the middle and lowend I would expect some serious pricing competition from Intel to keep AMD's market share minimal. Even without Intel, they have taken a beating from their customers due to the recent wave of security flaws which have significantly impacted some server workloads. End users want to upgrade but not at the prices Intel is charging. Intel also has several new server chips in the wings for later this year (Cooper Lake) and next year (Ice Lake-SP). I'd expect lots of previews of these chips to act as a 'we can wait one more quarter' deterrent for immediate purchases as well as hinting at lower prices for them.