Intel Q3 FY 2014 Quarterly Earnings Analysis

by Brett Howse on October 14, 2014 7:15 PM EST

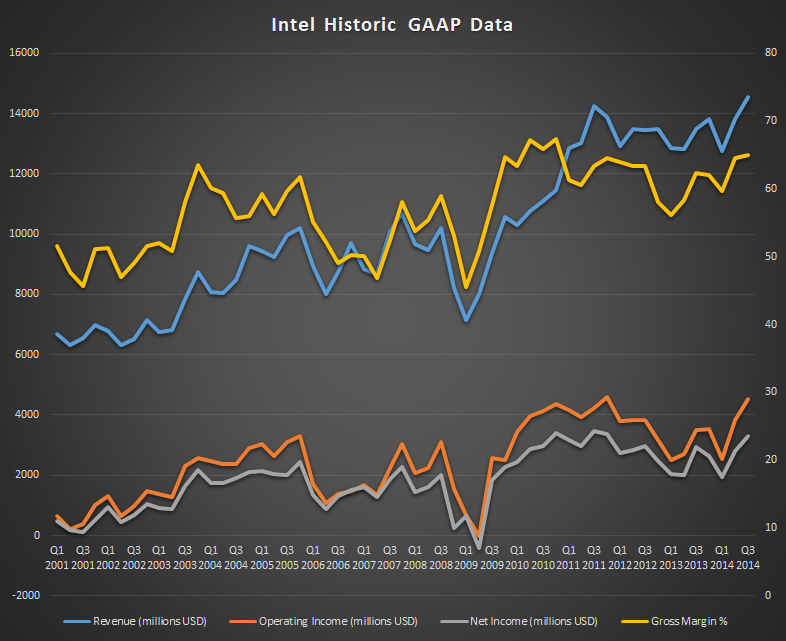

Today Intel released their financial results for the third quarter of their 2014 fiscal year, which ended September 27, 2014. Q3 was a record quarter for Intel, with the highest revenue in the company’s history. Their major markets of the PC Client Group was up 9% year-over-year and the Data Center Group was up 16% year-over-year.

Earnings per share was up 14% compared to Q3 2013 at $0.66, beating analysts’ expectations of $0.65. Year-over-year, revenue was up 8% at $14.6 billion, Gross Margin was up 2.6% at 65.0%, Operating Income was up 30% at $4.5 billion, and net income was up 12% at $3.3 billion.

The PC Client Group, which includes all business related to desktops, notebooks, two-in-one systems, wired and wireless Ethernet (for the PC), home gateway, and set-top-box components, continues to be the largest division for Intel with $9.190 billion in revenue this quarter. For the first three quarters, the PC Client group has contributed $25.789 billion in revenue, up $1.1 billion over the same period a year ago. This group had an operating income for Q3 2014 of $4.120 billion, up from $3.243 billion last year. Q2 seemed to indicate that the PC market has bounced back, and these revenues and income from the PC division for Q3 indicate that the trend will continue. The volume of sales for the quarter were up 7% over last quarter, and up 15% year-over-year. At the same time, the Average Selling Price (ASP) was down 2% from last quarter and down 5% year-over-year. Notebook volumes were up 21% year-over-year with the ASP down 10%, and desktop volumes were up 6% with the ASP down 2%. Intel is forecasting Q4 revenue at $14.7 billion, plus or minus $500 million, so their expectations are that the PC industry will continue its rebound. For Q3, Intel continued to sell the 22 nm range of processors, but has started production of 14 nm Broadwell parts, with a modest increase in inventory which they will likely utilize to keep up with demand for the new parts. Clearly the 14 nm node was a challenge, with the 22 nm node now being the primary process for the last ten quarters, with the average length of time between nodes being 8.5 quarters, starting with the 130 nm process. Q4 looks to be exciting with a whole new type of device able to be created from the Broadwell processors. We should start to see actual devices for sale within the next couple of weeks.

The Data Center Group, which is platforms for server, workstation, networking, and storage computing segments, was also up for Q3, with revenue up to $3.7 billion from $3.178 billion a year ago. Operating Income rose $395 million over Q3 last year to $1.915 billion. Unit volumes were up 6% year-over-year and sequentially, and the ASP was down 1% sequentially and up 9% over Q3 2013.

The Internet of Things group, which is a relatively new division focused on embedded platforms for retail, automotive, home, and transportation, had revenues for the quarter of $530 million, up 12% year-over-year. Revenues were only up $1 million over last year, with $153 million in revenue for this quarter.

The Mobile and Communications Group, which is the division responsible for platforms for tablet and smartphones, as well as mobile communications with baseband processors, RF transceivers, GPS, Wi-Fi, Bluetooth, and power management chips continued its slide for Q3. Revenues were down around 100% year-over-year, at a meager $1 million. This division is also responsible for the majority of Intel’s losses, with a Q3 operating loss of $1.043 billion. For the nine months ended September 27th, this unit has lost $3.096 billion. Intel is pushing hard to drive adoption of its mobile processors, and they seem to be OK with losing money on them in the short term to gain the foothold for the future. We have seen a slew of low priced tablets packing Intel Bay Trail processors, including the HP Stream tablets and just recently a $65 tablet from Emdoor out of Hong Kong. It seems hard to believe that you can buy a Windows tablet for less than the cost to fill your tank with gas, but with both Intel and Microsoft dropping fees, you have to wonder how low things will go before they stop. Luckily for Intel, their strong performances in other segments allows them to be a loss leader in this category, and they must see the long term gain here by not just allowing ARM SoCs to rule the space.

The final division for Intel is the Software and Services segment, which includes McAfee which they acquired a few years ago, and the Software and Services Group which delivers products and services that promote Intel architecture as a platform for development. This unit had a slight bump in revenues, up $13 million over last quarter to $558 million, and operating income was up 97% at $29 million.

| Intel Q3 2014 Financial Results (GAAP) | |||||

| Q3'2014 | Q2'2014 | Q3'2013 | |||

| Revenue | $14.554B | $13.831B | $13.483B | ||

| Operating Income | $4.918B | $3.844B | $4.910B | ||

| Net Income | $3.317B | $2.796B | $2.950B | ||

| Gross Margin | 65.0% | 64.5% | 58.3% | ||

| PC Group Revenue | $9.2B | +6% | +9% | ||

| Data Center Group Revenue | $3.7B | +5% | +16% | ||

| Internet of Things Revenue | $530M | -2% | +14% | ||

| Mobile Group Revenue | $1M | -98% | -99.7% | ||

| Software and Services Revenue | $558M | +2% | +2% | ||

| All Other Revenue | $558M | +2% | +2% | ||

Q4 expectations are for revenue to increase slightly to $14.7 billion, plus or minus $500 million and Gross Margin will be 64%, plus or minus a couple of points. With Broadwell soon to be shipping to consumers, Intel is clearly expecting another record quarter. It is great to see the PC market recovering, and one has to wonder to what level it will continue. The expectations of the tablet replacing the PC seem to have subsided for the moment, due to a slump in overall tablet sales. With Broadwell now shipping, we will of course anxiously await Skylake, which will be the new Core architecture available on 14 nm, and the Cherry Trail Atom chips which will also use the new node.

This was a pretty bullish quarter for Intel, which is generally a good indicator of the overall PC market. They still have their work cut out for them in the mobile segment, but with the other divisions pulling in great revenue and margins, they seem to be content to play the long game on what is certainly a very important segment for the future.

Source: Intel Investor Relations

37 Comments

View All Comments

TheJian - Wednesday, October 15, 2014 - link

Yet the K1 smoked T100 in everything. See the review of the shield tablet here at anandtech ;)Kjella - Wednesday, October 15, 2014 - link

It's not that crappy but if Intel wasn't buying their way to market share through contra revenue you'd probably not see many x86 tablets at all. So you can pick your poison, either it won't sell because of Intel or it won't sell because of ARM, either way Mullins is pretty much dead on arrival. It's no secret what Intel is doing:http://www.pcworld.com/article/2089421/how-intel-i...

AMD is rather screwed, but then this was rather predictable. Everyone knew Intel and ARM (Samsung, Qualcomm, nVidia, Apple+++) was going to clash and when giants fight the little guys are likely to get stomped. I understand the two-way race with Intel was going badly for AMD, but they jumped out of the frying pan and into the fire by going into ARM territory themselves.

yannigr2 - Wednesday, October 15, 2014 - link

There would have been Mullins in the market. Not many, only a few, but there would have been products with Mullins enough to justify the R&D cost, or part of it.Many people are happy with an Android tablet or a chromebook, many are with an iPhone/iPad, many others want a cheap portable device with x86 Windows on it. If Intel wasn't giving away free chips, yes, x86 devices would have been a little more expensive and not a threat for the ultra cheap ARM tablets. But people who wanted x86 Windows would be buying those. Not in great numbers, but they would be buying them. And AMD would have a small part of that x86 market, even a very small one.

What Intel is doing now is not just trying to create a market share that will have to keep spending money forever to maintain, but it is also killing anything AMD can create and not give away for free of course. So, this poison is much worst for AMD than the other one.

As for AMD jumping on the fire. Nope. You said it yourself. Mullins end up DOA because of Intel's tachtics. So, what do you do then? You go to the ARM platform and do what Nvidia is doing. Use your graphics advantage to try to take a part of the market. At least there you could sell something for money, without Intel sabotaging you in any way possible.

Nvidia abandoned smartphones, in the future Tegra will move from tablets and chromebooks to Steam machines. AMD will follow with both low power x86 and ARM cores. Both companies have an advantage there over Intel and when ARM cores become powerful enough, and Windows less important, they could turn the tables against Intel. Intel of course has billions and billions for R&D and it can close the gap in graphics to defend it's huge market share thanks to integrated graphics that it has today. The future is not x86 only, so no, AMD isn't jumping on the fire.

AnakinG - Wednesday, October 15, 2014 - link

You believe the only reason why AMD Mullins NOT selling is due to Intel's contra revenue? To me, that's very hard to believe. Unless you are saying there's no / not much difference between Bay Trail and Mullins. Performance / feature differentiation I THINK will always over-power cost difference if there's a market need for it. I think it's that there's really no real Tablet market need for Mullins (or Bay Trail) when it is already saturated by ARM counterparts.I argue exactly opposite actually. All of the money Intel pours into tablet market to enable x86 share will benefit AMD in the future versions of Mullins (don't know their code names.) If anything AMD should thank Intel for helping to establish x86 Tablet market. So this should be a good news for fanboy like you. :)

yannigr2 - Wednesday, October 15, 2014 - link

AMD usually let Intel create a market and then comes in, I agree. They do it constantly with RAM for example. But this time because of ARM a market is created and sustained in a way that AMD, at least today, can not enter in any meaningful way.A free chip and an Intel logo on a tablet that it's cost is already low, is way too much marketing value for an AMD product to become an option, even if it performs better in some areas like for example graphics.

AnakinG - Wednesday, October 15, 2014 - link

Don't worry - Intel won't be able and will not keep up the contra revenue for too long. Next generation of x86 based products need to be free of contra revenue (NOT free of charge of course.) That's when AMD needs to target market entry for Tablet - better make sure whatever lined up to match Intel performance is below Intel's chip cost so value proposition is better than Intel. Cross your fingers. :)ppi - Thursday, October 16, 2014 - link

Well, if I was Intel shareholder, I would have been certainly asking, what is their long-term proposition of that business, that they needed to sink half their profits into it ...TheJian - Wednesday, October 15, 2014 - link

NV abandoned commodity phones ($300 and down), not the high end. We will see what Denver gets in this area soon, as it's in house cpu should be even better at power than K1 32bit, which should easily enable their own modem or even qcom's to be included and do a nice job vs the competition especially since S808/810 LOSE this advantage as they are off the shelf IP.We know maxwell's power kicks the crap out of kepler, so next june we should see an M1@20nm which will surely garner some high end phones if not Denver itself shortly. Nexus 9 and shield tablet have LTE so you can already do it, just need to see how Denver's battery is, and if it's capable of running with decent life in a high end phone. Qcom loses perf and battery advantages of IN HOUSE next year so we'll see how that affects their phone sales. I'd bet NV wins at least a few with denver, or at worst the maxwell version. I don't think NV will put out a 20nm K1, but that would surely do it too (I'm guessing 20nm will be M1 and beyond), but who knows.

testbug00 - Friday, October 17, 2014 - link

how phones was Tegra 4 (not 4i, 4i is a completely different beast and is aimed at lower cost phones) again?I think it was one, and, that one was part of 2 models, one with Qualcomm... I believe the Tegra one was projected to ship less due to which carriers got it in China and some junk like that.

Only potential reason to but Tegra K1 in a phone is the GPU power, but, in a phone TPD/heat limit, you would have to downclock the GPU so much that it wouldn't end up much faster than its competitors.

I don't buy Tegra getting back into phones anytime soon, at least, not unless they have a Tegra 4i successor, which, I would love to see... Maybe the Maxwell Tegra parts will have high end part with 2 SMM and low end part with 1? I think it would be awsome in a mid-high end phone than.

name99 - Wednesday, October 15, 2014 - link

"The Internet of Things group, which is a relatively new division focused on embedded platforms for retail, automotive, home, and transportation, had revenues for the quarter of $530 million, up 12% year-over-year. Revenues were only up $1 million over last year, with $153 million in revenue for this quarter."One wonders whether the IoT numbers are as fake as the previous Mobile numbers were.

It's pretty obvious that the previous Mobile quarters were playing some sort of games, booking revenue as early as possible and delaying accounting for the bribes until they could be delayed no longer (ie this quarter).

After all Atom is actually not a completely crappy chip, unlike Quark, so if they have to bribe the hell out of anyone to use Atom, god only knows how large the bribes are to use Quark.