Intel Reports Q1 2020 Earnings: Another Strong Quarter For Both Client and Datacenter

by Ryan Smith on April 24, 2020 9:30 AM EST- Posted in

- CPUs

- Intel

- Financial Results

Kicking off earnings season for the tech industry, Intel yesterday evening reported their financial results for the first quarter of the year. And, like pretty much every Intel quarter for the last couple of years, it was a doozy, with Intel once again recording growing revenues and a very healthy profit margin.

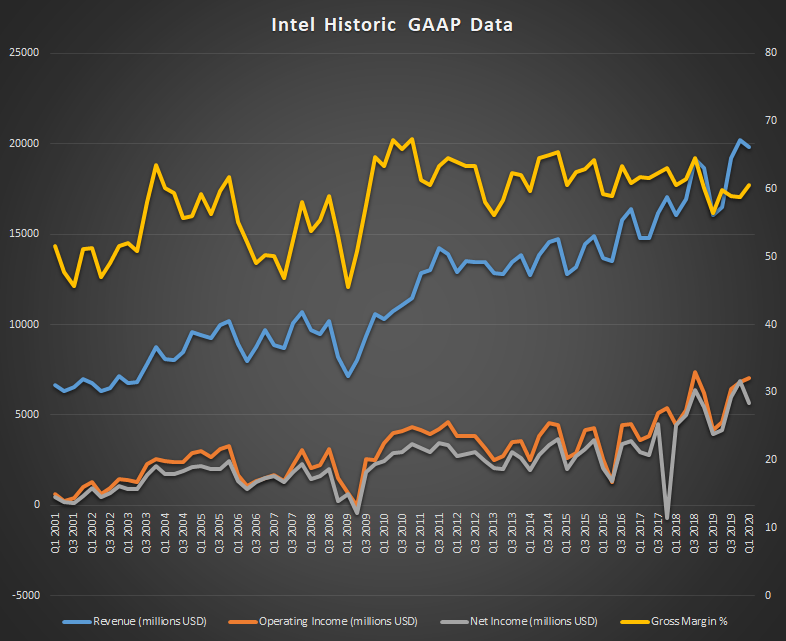

For the first quarter of 2020, Intel reported $19.8B in revenue, a significant improvement over the year-ago quarter, and only slightly behind Intel’s record-breaking Q4. As a result of this strong revenue, income was also very healthy for the company, with Intel recording $5.7B in net income, a 43% jump over Q1’19. Meanwhile gross margins were up 4 percentage points to 60.6%, pushing Intel back above their much revered 60% gross margin threshold.

| Intel Q1 2020 Financial Results (GAAP) | |||||

| Q1'2020 | Q4'2019 | Q1'2019 | |||

| Revenue | $19.8B | $20.2B | $16.1B | ||

| Operating Income | $7.0B | $6.8B | $4.2B | ||

| Net Income | $5.7B | $6.9B | $4.0B | ||

| Gross Margin | 60.6% | 58.8% | 56.6% | ||

| Client Computing Group Revenue | $9.8B | -2% | +14% | ||

| Data Center Group Revenue | $7.0B | -3% | +43% | ||

| Internet of Things Revenue | $1137M | -2% | +8% | ||

| Non-Volatile Memory Solutions Group | $1.3B | +8% | +46% | ||

| Programmable Solutions Group | $519M | +3% | +7% | ||

Breaking things down on a group basis, many of Intel’s internal reporting groups saw double-digit growth over the year-ago quarter. Client computing revenue was up 14% to $9.8B, and data center revenue was an even bigger winner with $7.0B in revenue, a 43% jump over the previous year. The significant growth in the data center segment comes as Intel saw both higher average selling prices and higher volumes overall, with ASPs and volumes growing by 13% and 27% respectively. Overall Intel attributes the data center gains to the company’s “broad strength” in the market, though they did note that they’ve seen a 53% year-over-year increase in revenue from cloud service providers.

As for client computing revenue, the biggest gains there came from notebook ASPs, which were up 22% over the year-ago quarter. Other client metrics were relatively tame; notebook volumes actually slipped 3%, while on the desktop, ASPs were up 4% while volumes were down 4%. For Intel’s client group, the company is coming off of the second quarter of selling Ice Lake laptops, with improving supply and improving helping to drive those numbers. As well, Intel’s new Comet Lake-H CPUs were recently launched, which means those would have been shipping to OEMs in Q1 as well.

Rounding out Intel’s product portfolio, the company recorded smaller gains for their Programable Solutions Group, as well as their Internet of Things business. Overall IoT was a mixed bag: Mobileye revenue, which the company offers a separate breakout, was up 22% over the previous year, but the rest of Intel’s IoT business saw a 3% drop in revenue. Finally, Intel’s storage group was a surprising winner, with record revenue pushing them to year-over-year growth of 46%, thanks to higher NAND ASPs and lower unit costs.

Meanwhile, like most other tech companies, the 800lb gorilla of the chipmaking world finds itself in an interesting position as the novel coronavirus pandemic has shuttered large parts of the world’s economies. For Q1, Intel believes they actually benefitted somewhat from the outbreak, as companies and consumers needed to make previously-unplanned purchased of laptops and other equipment for working from home and remote learning. However as the pandemic continues, it’s likely to start impacting Intel’s sales in other ways, as idled business won’t be making their usual purchases and expansions. As a result, Intel isn’t even providing full-year financial guidance due to the economic uncertainty that the pandemic has caused.

On the flip side of the coin, as a business and employer themselves, the coronavirus outbreak has also threatened Intel’s manufacturing operations. Despite that, according to Intel the company was able to keep all of its essential manufacturing operations going, with an on-time delivery rate that’s still better than 90%. So thus far Intel seems to have weathered the first part of the pandemic fairly well.

All eyes then will be on the second quarter, both for continuing developments with the coronavirus pandemic, as well as Intel’s own internal manufacturing efforts. With Intel set to start shipping its 10nm Tiger Lake CPUs to OEMs by mid-year, the company is going to be pushing its 10nm manufacturing lines harder than ever as they ramp up for a new generation of CPUs. While slowly improving, 10nm’s rocky bring-up remains a bit of a proverbial albatross around Intel’s neck, so further improving capacity and yields will go a long way towards helping Intel maintain its success, especially in light of heavy competition from AMD.

Source: Intel

49 Comments

View All Comments

Spunjji - Tuesday, April 28, 2020 - link

"Comment section is overrun by hypocritical projecting dweebs who whine about AMD fanboys while relentlessly shilling for Intel"FTFY

TristanSDX - Friday, April 24, 2020 - link

no 10nm desktop CPU this year, confirmedTiger Lake, Ice Lake for servers and SoC 5G - that's all stuff

yeeeeman - Friday, April 24, 2020 - link

This year only rocket lake for desktop which is tigerlake on a 14nm node.Deicidium369 - Saturday, April 25, 2020 - link

14nm Rocket Lake with architecture from Tiger Lake - Ice Lake (Sunny Cove) saw a 20-30% increase in IPC and Tiger Lake (Willow Cove) is likely to increase IPC by a similar amount - and with the superior frequency of Intel 14nm - those cores at 4-4.5Ghz are beasts. This will be the final 14nm Desktop flagship.There are no Tiger Lake servers - Ice Lake, yes.

Lord of the Bored - Monday, May 4, 2020 - link

" This will be the final 14nm Desktop flagship."I'll believe it when I see it. Intel's been promising 10nm any day now for quite a while.

trivik12 - Saturday, April 25, 2020 - link

AMD fans are retarded. This is a phenomenal result considering its Q1 with no blockbuster product launch. Plus Intel is very conservative with its projections. I am expecting another big beat for Q2 when Tigerlake will start to ship for revenue. Q3 should have ice lake servers for revenue.Biggest point is Intel is sitting on huge cash pile and can weather this crisis.

Deicidium369 - Saturday, April 25, 2020 - link

They have a decent warchest for sure - but they are paying out an almost $5 per share dividend.I would push those back a bit - Q4 to show revenue from Tiger Lake and Q1 to show revenue for Ice Lake servers. TGL ships mid year for mid Q3 OEM sales - so Q4 will show the strength of Tiger Lake. Ice Lake start shipping around the same time - so might be Q4 or Q1 before we see the full impact. Certainly will see some impact in Q2 and Q3 from those launches.

I would expect Q2 to be strong - really depends on Covid - I am sure Intel has orders to see them through Q2 ... But not expecting to see it as strong as Q1.

Either way, will be a busy year for Intel. Desktop, Laptop, Server and GPU. Then the updated Optane SSDs and DIMMs, In the meantime their latest 10nm FPGA Agilex has been shipping.

Korguz - Saturday, April 25, 2020 - link

what ever anti amd Deicidium369. you bash amd here, and bashed amd on toms, but NOT once did you every that i could see, post any sort of proof to you BS, FUD, or personal opinions.jjjag - Sunday, April 26, 2020 - link

Intel does not pay out $5 per share as a dividend. Earnings are about $5/sh and dividends are $1.32 per share. That is a nice safe ratio. Please learn how to use the internet before you post.Nobody cares how YOU project Intel's next Q earnings, because you have no idea what you are talking about. Intel themselves provided Q2 projection in their quarterly release. That is what we look at, not the musings of some internet crackpot

AshlayW - Sunday, April 26, 2020 - link

Begone, shill.