Intel Announces Q3 FY 2018 Earnings: Record Quarter

by Brett Howse on October 25, 2018 6:50 PM EST- Posted in

- CPUs

- Intel

- Financial Results

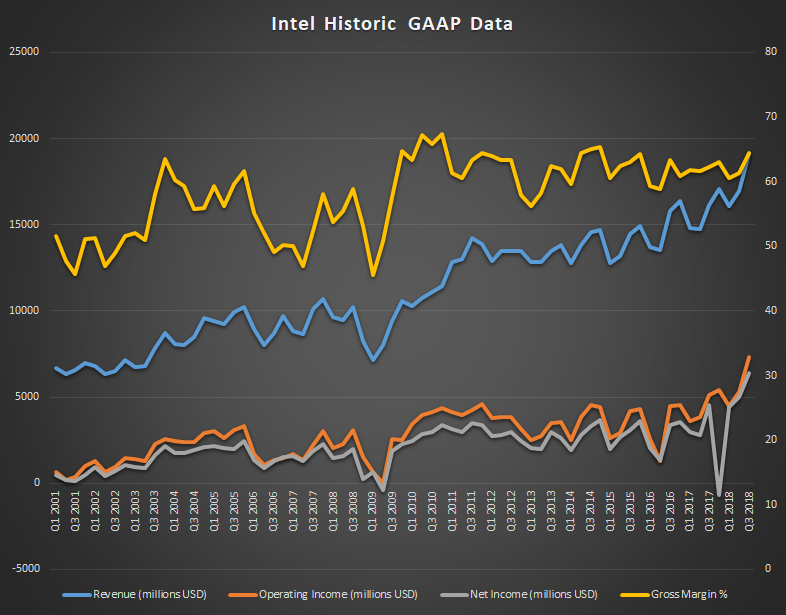

This afternoon, Intel announced their earnings for the third quarter of their 2018 fiscal year. Revenue was at a record level compared to any previous quarter, coming in at $19.2 billion, which is a gain of 19% compared to Q3 2017. Gross margin was up 2.2% to 64.5%. Operating income was up 43% to $7.3 billion, and thanks to a tax rate of just 10.4%, net income was up 42% to $6.4 billion. This resulted in earnings per share of $1.38, a gain of 47% from a year ago.

| Intel Q3 2018 Financial Results (GAAP) | |||||

| Q3'2018 | Q2'2018 | Q3'2017 | |||

| Revenue | $19.2B | $17.0B | $16.1B | ||

| Operating Income | $7.3B | $5.3B | $4.9B | ||

| Net Income | $6.4B | $5.0B | $4.5B | ||

| Gross Margin | 64.5% | 61.4% | 62.3% | ||

| Client Computing Group Revenue | $10.2B | +17.2% | +16% | ||

| Data Center Group Revenue | $6.1B | +11% | +26% | ||

| Internet of Things Revenue | $919M | +4% | +8% | ||

| Non-Volatile Memory Solutions Group | $1.1B | flat | +21% | ||

| Programmable Solutions Group | $517M | -4% | +6% | ||

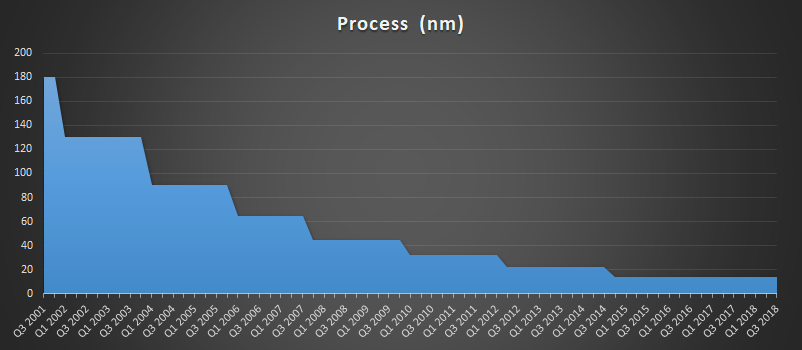

Intel saw gains across its lineup, despite setbacks on the manufacturing side which have stalled the company at their 14 nm process for several years. The Client Computing Group had revenues of $10.2 billion for the quarter, which is up 16% from a year ago, and operating income was up 26% to $4.5 billion. Intel attributes this growth to continued strong growth in the gaming sector, as well as commercial demand. Intel now puts their modem business into the Client Computing Group, and almost certainly thanks to a design win in a certain smartphone from Cupertino, Intel had growth of over 66% in their modem business, which had revenues of $1.2 billion this quarter. Revenue from notebook processor sales increased 13%, and desktop revenue was up 9%, with Intel overall growing PC volumes by 6% year-over-year. Considering the strong competition right now, that is quite impressive.

The Data Center Group continues its upward trajectory as well, with revenues up 26% to $6.1 billion for the quarter. Operating income grew 37% to $3.1 billion Looking at segments, Intel’s Cloud SP segment grew revenue by 50% year-over-year, and Comms SP was up 30% as datacenters evolve to software defined networks. Intel sold 15% more units in their Data Center Group, at 10% higher average selling prices.

The IOT Group had revenues of $919 million, which is up 8% from a year ago, while operating income grew 120% to $321 million. Non-Volatile Storage was up 21% year-over-year to $1.1 billion, thanks to growth in datacenter and Optane sales, and Intel is transitioning to 64-layer NAND for SSDs, with over 50% of sales now being this type. Operating income was up 408% as Intel earned $160 million from this group this quarter, compared with a $52 million loss last year. Programmable Solutions was up 6% year-over-year to $496 million, although operating income was down slightly at $106 million.

Intel is still promising 10 nm by holiday 2019, but as to what that ends up being is hard to say now. There’s little doubt the company has struggled to move past their 14 nm node, despite increasing R&D spending by 11% since 2015. Originally, they were targeting 100 million transistors per square millimeter, but it’s possible they’ve reset their expectations.

Looking ahead to Q4 2018, Intel is expecting revenue of $19 billion, and they have raised their full-year outlook to expect $71.2 billion for FY 2018.

Source: Intel Investor Relations

36 Comments

View All Comments

HStewart - Saturday, October 27, 2018 - link

Note also Intel has shown they can enhance 14nm mode recently with more performance, core and even power savings with changing node.I think rise in stock prices is because they have shown that they can overcome this and even over come security issues

HStewart - Saturday, October 27, 2018 - link

Without changing mode for above - it would nice to edit - sorry I think faster that I type. It better that way then other way aroundsa666666 - Friday, October 26, 2018 - link

And again, you prove yourself a fool if you find it 'hard' to purchase a product because of the comments of some people using it. If you base your purchasing decisions on what some fanboy says instead of what the hardware will actually deliver, then you're not a very intelligent person.Just admit it; in your mind Intel can do no wrong, and you will buy it no matter what the circumstance. This "some of comments from Anti-AMD make it very hard to EVER consider AMD" is just an idiotic smoke-screen around your obvious heavy bias for Intel products. I have _never_ in all my years met some so devoid of logic and devoted to a company as you are.

Black Obsidian - Monday, November 5, 2018 - link

I'm a bit late on this comment, but in case others are even further behind on their reading...The 13% and 9% numbers are REVENUE growth, while 6% is VOLUME growth. So Intel is selling more units *and* charging more for each unit compared to last quarter.

Supercell99 - Friday, October 26, 2018 - link

I don't know if they are "stuck" at 14nm or just milking the sh!t out of it, look at their profits. Why build new 10nm fabs when you can make billions with the old 14nm ones.Eliadbu - Friday, October 26, 2018 - link

You are right you do not know, especially about situation. They invested ten of billions of dollars on fabs that still do not produce any chip for the mass market right now. what is the point of investing so much money on a technology if you don't sell it? Unless they can't mass produce right now...sseemaku - Friday, October 26, 2018 - link

It thought AMD's good product launches will impact Intel just like every one keep saying it again and again. What did I miss? Did customers forget AMD totally?lemans24 - Friday, October 26, 2018 - link

Yes...Intel is in NO way affected by AMD prices on ANY of their products as the last year of revenues clearly indicates!!Targon - Friday, October 26, 2018 - link

You have places like Staples that went all in on intel when it comes to what machines to display(even if they have AMD machines hidden away in back). I suspect payoffs to be "Intel only" for what is on display, or the old, "We don't want you selling more than 10 percent of your computers with an AMD processor" approach that they have done before.If you don't see a computer out on display, and don't know enough to look online for what they actually offer(and know to look for a Ryzen 5 2500U based laptop for example), then you won't be buying an AMD based machine from many of these stores. It's pretty sad that those who decide what machines should be out on display have no computer knowledge.

darkich - Friday, October 26, 2018 - link

Sickening..