Intel Announces Q3 FY 2018 Earnings: Record Quarter

by Brett Howse on October 25, 2018 6:50 PM EST- Posted in

- CPUs

- Intel

- Financial Results

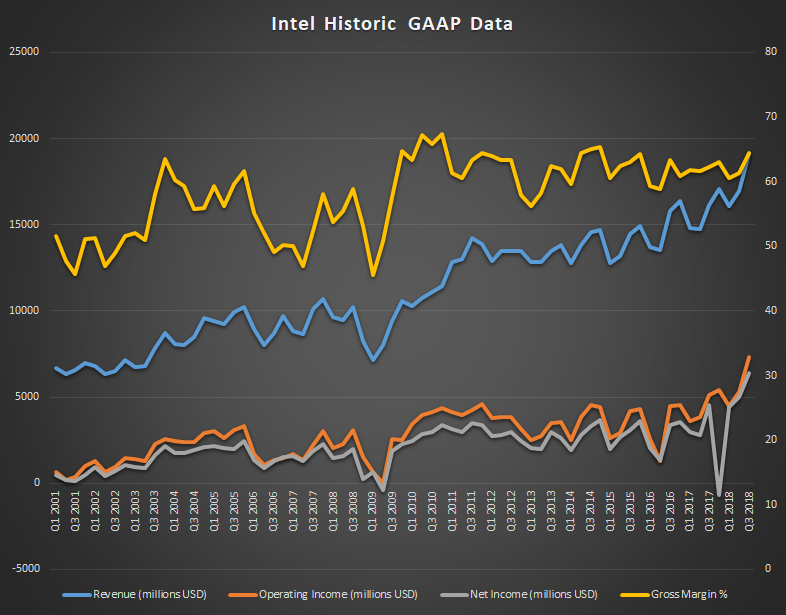

This afternoon, Intel announced their earnings for the third quarter of their 2018 fiscal year. Revenue was at a record level compared to any previous quarter, coming in at $19.2 billion, which is a gain of 19% compared to Q3 2017. Gross margin was up 2.2% to 64.5%. Operating income was up 43% to $7.3 billion, and thanks to a tax rate of just 10.4%, net income was up 42% to $6.4 billion. This resulted in earnings per share of $1.38, a gain of 47% from a year ago.

| Intel Q3 2018 Financial Results (GAAP) | |||||

| Q3'2018 | Q2'2018 | Q3'2017 | |||

| Revenue | $19.2B | $17.0B | $16.1B | ||

| Operating Income | $7.3B | $5.3B | $4.9B | ||

| Net Income | $6.4B | $5.0B | $4.5B | ||

| Gross Margin | 64.5% | 61.4% | 62.3% | ||

| Client Computing Group Revenue | $10.2B | +17.2% | +16% | ||

| Data Center Group Revenue | $6.1B | +11% | +26% | ||

| Internet of Things Revenue | $919M | +4% | +8% | ||

| Non-Volatile Memory Solutions Group | $1.1B | flat | +21% | ||

| Programmable Solutions Group | $517M | -4% | +6% | ||

Intel saw gains across its lineup, despite setbacks on the manufacturing side which have stalled the company at their 14 nm process for several years. The Client Computing Group had revenues of $10.2 billion for the quarter, which is up 16% from a year ago, and operating income was up 26% to $4.5 billion. Intel attributes this growth to continued strong growth in the gaming sector, as well as commercial demand. Intel now puts their modem business into the Client Computing Group, and almost certainly thanks to a design win in a certain smartphone from Cupertino, Intel had growth of over 66% in their modem business, which had revenues of $1.2 billion this quarter. Revenue from notebook processor sales increased 13%, and desktop revenue was up 9%, with Intel overall growing PC volumes by 6% year-over-year. Considering the strong competition right now, that is quite impressive.

The Data Center Group continues its upward trajectory as well, with revenues up 26% to $6.1 billion for the quarter. Operating income grew 37% to $3.1 billion Looking at segments, Intel’s Cloud SP segment grew revenue by 50% year-over-year, and Comms SP was up 30% as datacenters evolve to software defined networks. Intel sold 15% more units in their Data Center Group, at 10% higher average selling prices.

The IOT Group had revenues of $919 million, which is up 8% from a year ago, while operating income grew 120% to $321 million. Non-Volatile Storage was up 21% year-over-year to $1.1 billion, thanks to growth in datacenter and Optane sales, and Intel is transitioning to 64-layer NAND for SSDs, with over 50% of sales now being this type. Operating income was up 408% as Intel earned $160 million from this group this quarter, compared with a $52 million loss last year. Programmable Solutions was up 6% year-over-year to $496 million, although operating income was down slightly at $106 million.

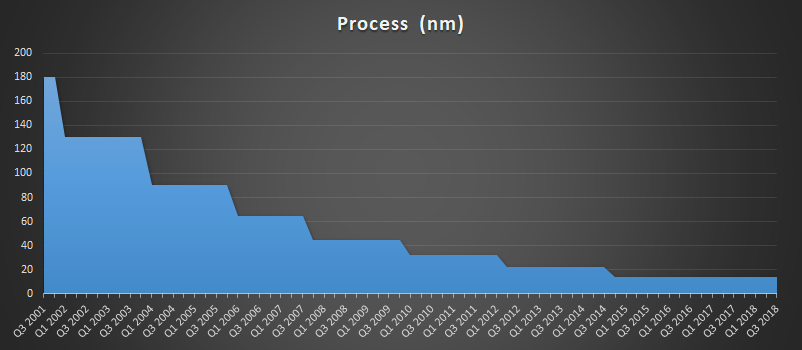

Intel is still promising 10 nm by holiday 2019, but as to what that ends up being is hard to say now. There’s little doubt the company has struggled to move past their 14 nm node, despite increasing R&D spending by 11% since 2015. Originally, they were targeting 100 million transistors per square millimeter, but it’s possible they’ve reset their expectations.

Looking ahead to Q4 2018, Intel is expecting revenue of $19 billion, and they have raised their full-year outlook to expect $71.2 billion for FY 2018.

Source: Intel Investor Relations

36 Comments

View All Comments

Dragonstongue - Thursday, October 25, 2018 - link

64% margins...LMFAO, that just shows IMHO they are cheaping out HUGE to make such a massive margin (compared to most companies) it must be all that saving of PCB layers and using toothpaste for TIM ^.^.kind of "crappy" that no matter how "bad they do" they still walk away with champagne in both hands eating caviar (something along those lines) I wonder what Ngreedia margins are (even though they always seem to claim one year ahead of everyone else??) 150% :P

Lord of the Bored - Friday, October 26, 2018 - link

Less that they're cheaping out and more that they are price-gouging with the most rapacious markups they can get away with. You don't bloat your margins massively with nickel-and-dime cost-cutting.PeachNCream - Friday, October 26, 2018 - link

While I agree there might be price gouging, I do like where the EPS is going. Enterprise customers are on life cycle upgrades so they represent a stable income source. In the home computer market, we've had more than enough CPU power to handle the average home computing tasks. If someone wants to throw down money for a 9900k that gives them the same performance in a game as a 8400, go for it.Kvaern1 - Friday, October 26, 2018 - link

It's not price gouging. It's milking an owned luxury item market.One is illegal, the other isn't.

PeachNCream - Friday, October 26, 2018 - link

That's a good point and an important distinction. I was being a bit too casual about referring to it as price gouging.wiz329 - Friday, October 26, 2018 - link

Gross margin doesn't include any depreciation. In a capital-intensive industries, having high gross margins doesn't mean a lot.iwod - Thursday, October 25, 2018 - link

--Intel had growth of over 66% in their modem business, which had revenues of $1.2 billion this quarter. Revenue from notebook processor sales increased 13%, and desktop revenue was up 9%, with Intel overall growing PC volumes by 6% year-over-year.this doesn't make sense, subtracting modem revenue from clients computing, the rest of it don't make up.

HStewart - Friday, October 26, 2018 - link

I think it very simple to explained - Intel competition has been push node side a lot and Intel has shown that it can make significant improvements without changing the node. Of course the competition wants to state that current generation is same as original 14 nm version which is not true. Intel has proven that it can do it and more than just adding cores. I have 4th Generation Lenovo Y50 and 8th Generation Dell XPS 2in1 - except for possibly the video on the XPS, the Dell is significantly faster than the Y50 and half the width and same number of cores. Also AMD concentrated on game desktop machine and that is not Intel primary focus - which is actually mobile laptops. AMD does have some in that market - but they got into late and by that time with the push of Ryzen on their hill, Intel was able to improved Mobile performance and size and make a difference.Gamers may differ with this but industry see that even with not having 10nm ready, that Intel can delivered newer products with more performance. Also make firmware and even hardware changes for Spectre/Melthown stuff

Another factor is trust - the average people see Intel has more trustworthily, for me personally, I have used Intel for decades and that means a lot to me. The average user does not care about what is stated on forums. But some of comments from Anti-AMD make it very hard to EVER consider AMD. My purchase of Dell XPS 15 2in1 was hard because of AMD GPU - but the technology in it override the video. EMiB is awesome technology and CPU performance is amazing. But also in the Dell XPS 2in1 designed. I did think it might have been a better decision to get a new Dell XPS 15 with Coffee Lake and NVidia GPU - but I find having power in 2in1 is nice.

peevee - Friday, October 26, 2018 - link

"Of course the competition wants to state that current generation is same as original 14 nm version which is not true"Yes, the current generation is actually BIGGER. More like 16 if the numbers would mean anything.

Drumsticks - Friday, October 26, 2018 - link

Who cares though? Would you really rather have a denser, lower frequency product on a desktop CPU? For the vast majority of the desktop products, 14nm is actually a great node. Sure, Enterprise and mobile need to move to 10nm because of power savings, but I'd rather use more power (within 100W or so) on a standard desktop and have higher clocks.