Market Views: HDD Shipments Down 20% in Q1 2016, Hit Multi-Year Low

by Anton Shilov on May 12, 2016 8:00 AM ESTUnit Sales of Enterprise HDDs Decline, But There Is a Catch

Enterprise hard disk drives are arguably the most important and lucrative part of HDD makers’ business these days. Firstly, such drives have to use many leading-edge technologies in order to demonstrate very high performance, or offer very high capacities. Secondly, they are not shipped in huge volumes, but they are sold with huge premium because of the technologies as well as extended reliability. Finally, since many client devices no longer have HDDs, but still have to store files elsewhere, their data ends up in the cloud and stored on various datacenter-class HDDs. Basically, even if an HDD maker fails to sell a $50 drive for a low-end laptop, the data from that laptop will eventually be stored on a $300 - $600 nearline drive in a data center, compensating missed revenue to the HDD producer.

There are two types of enterprise-class hard drives:

- High-performance HDDs for mission-critical storage that feature 10K or 15K spindle speeds as well as SAS interface. Such drives compete against SSDs these days and their volumes are slowly declining. This trend has been ongoing for years now and hard drive makers perfectly understand it. Seagate, Toshiba and Western Digital also offer high-end mission critical SSDs with SAS interface to their customers and eventually the portfolio of such solid-state storage devices will only expand.

- Another type of enterprise HDDs are nearline (near online) drives that are used to store various data in data centers. Some of such drives are for cold archives, which are rarely accessed and are hardly ever modified. Such HDDs have 5400 RPM-class spindle speed and their main purpose is to store as much data as possible and at the lowest cost. Other drives are used to store frequently accessed and modified data, which is why they feature 7200 RPM spindle speed and various methods to improve their performance. These drives can be filled with helium to maximize storage space (allowing a reduced platter gap) and keep power consumption down to minimize TCO. Usage of nearline HDDs has been increasing in the recent years. More importantly, their capacities have been growing very rapidly.

It is very important to distinguish between the two types of enterprise-class hard drives not only because they are completely different from a technology point of view, but also because their market dynamics are poles apart. Unfortunately, until this quarter neither of HDD makers disclosed sales of mission critical and nearline drives separately, but only reported the number of enterprise-class HDDs sold. This quarter, Seagate published more or less precise details about its enterprise drives and their dynamics, which we will analyze below. In the meantime, let’s have a look at the shipments of both leading enterprise HDD suppliers.

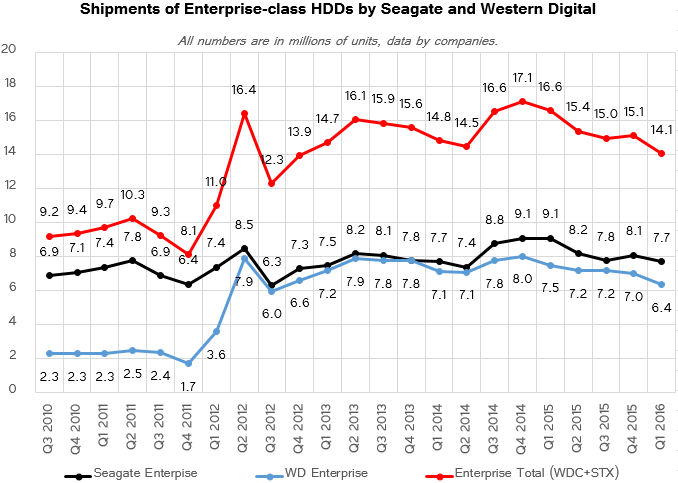

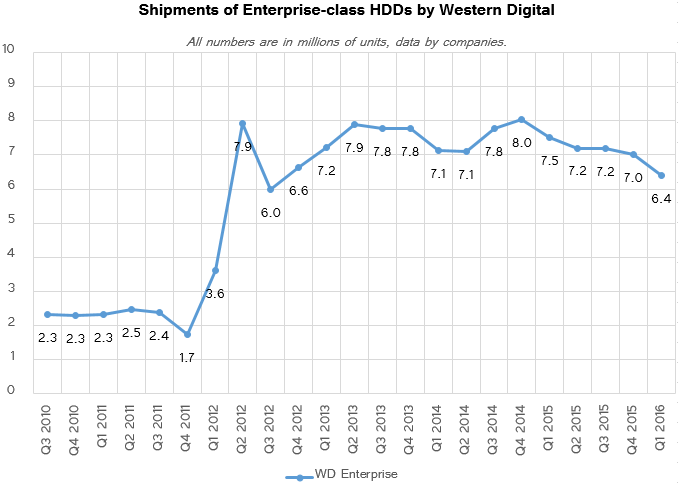

Based on the numbers from Seagate and Western Digital, sales of enterprise-class hard drives from these two manufacturers declined to 14.09 million units in Q1 2016, which is 15% lower compared to the first quarter last year. Seagate remained the largest supplier of enterprise drives with 7.7 million units sold (down 15.4% YoY), whereas Western Digital supplied 6.39 million of enterprise hard disks (down 15% YoY). Toshiba also has a portfolio of high-end drives for servers, but while it has many products with a SAS interface, it does not participate in the high-end of the nearline market due to lack of 8 TB and 10 TB HDDs in its lineup.

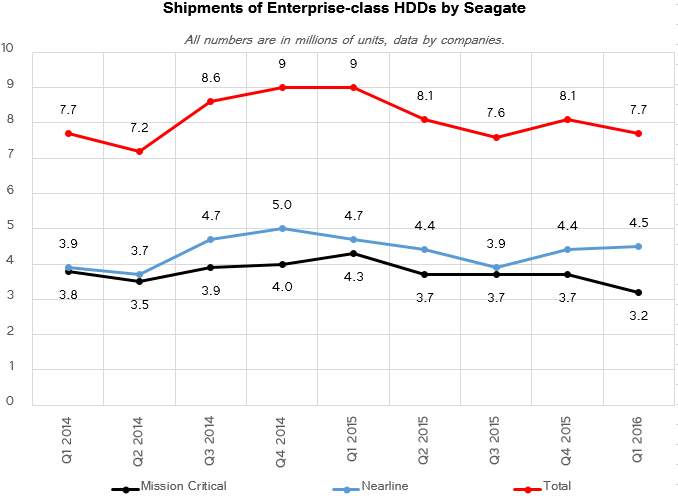

Out of 7.7 million enterprise drives that Seagate shipped in the first quarter, 4.5 million HDDs were for nearline storage applications, whereas 3.2 million HDDs were designed for mission-critical apps.

Shipments of Seagate’s nearline HDDs were down 4.3% compared to the first quarter of 2015, but were slightly up sequentially. The company claims that it expected demand for such drives to be significantly weaker, which is why it could not even satisfy all the demand. During the quarter, Seagate ramped up production of its 8 TB HDD lineup and significantly increased shipments of such drives compared to the previous quarter, however, it could not meet all the demand. The company also supplied a large volume of qualification units of its 10 TB helium-filled hard drives aimed at the highest-end of the cloud market. Due to the 7200 RPM spindle speed and advanced caching sub-system, Seagate’s Enterprise Capacity 3.5 (Helium) 10 TB hard drive is among the fastest in the company’s lineup, challenging even 15K mission-critical drives when it comes to sustained transfer rates (of course, those small drives still have a lot of other advantages, including considerably higher IOPS, significantly lower latency, very high instantaneous transfer rates and so on). In April, the company started revenue shipments of its SATA 10 TB HDDs, which further indicates growing demand for such drives.

By contrast, shipments of mission-critical HDDs dropped 13.6% sequentially and 25.6% year-over-year. The company says that approximately 25% out of 3.2 million mission-critical HDDs are 15K drives, which are gradually replaced by SSDs in the data centers. Solid-state storage devices also challenge 10K HDDs, but the manufacturer expects this segment of the market to have a much longer transition horizon. Because of the economic situation and the market shift to SSDs, sales of mission-critical drives were 700K below Seagate’s original forecast in Q1 2016, the company said.

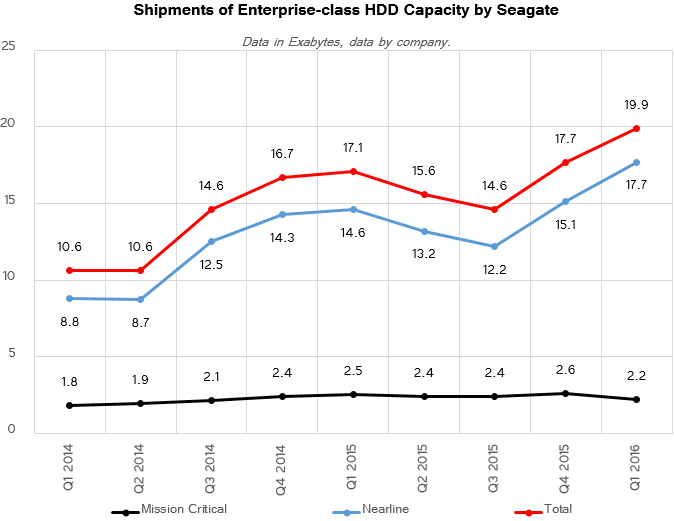

Given the fact that nearline drives have significantly higher capacities than mission critical drives, it is not surprising that they are driving enterprise storage capacities in terms of EB shipments.

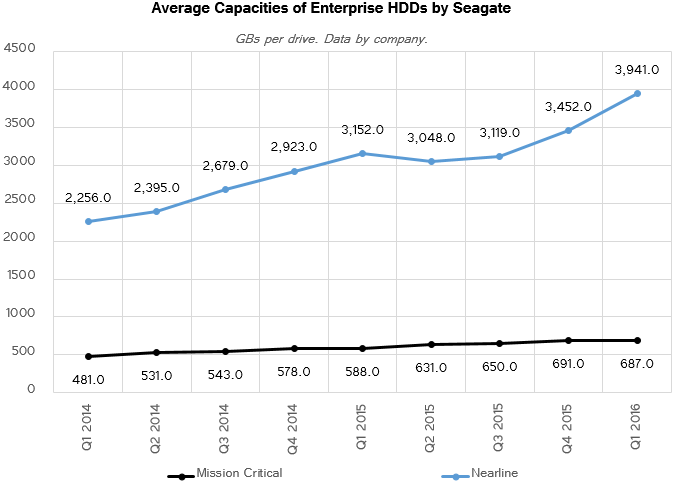

Average enterprise HDD sold by Seagate in Q1 2016 could store 3.941 GB of data, up 25% from the first quarter of last year, which is a direct result of growing demand for capacities from various data center customers.

Western Digital does not break down sales of its enterprise HDDs into nearline and mission critical categories, but while the split may be slightly different, market trends affect both companies in the same way. In its conference call with financial analysts, the management of Western Digital confirmed that shipments of the company’s 15K HDDs are declining because many customers replace such HDDs with SSDs and also observed that many 10K HDD deployments begin to adopt SSDs. In addition, the company noted that in Q1 2016 it saw steeper than expected price declines in performance enterprise and capacity enterprise markets. In particular, the company blamed decreased prices of 4 TB and 8 TB nearline HDDs for its lowering gross margins.

116 Comments

View All Comments

Michael Bay - Monday, May 16, 2016 - link

Hybrids have almost died by now for the reason of cost. Little logic in buying a hybrid if you can just get a proper SSD for comparable money.Arbie - Saturday, May 14, 2016 - link

What a great article! It reads like an MBA project. Even more impressive - by, um, a lot - if English is not Anton's first language. Efforts like this keep the shine on Anandtech (and remind us of what we lost in X-Bit Labs). Thanks.poohbear - Sunday, May 15, 2016 - link

so guess that would explain why Western Digital's stock is at its lowest ever @ $36 a share!piasabird - Thursday, May 19, 2016 - link

Part of this is that the current computers have CPU's that are so fast and dependable that it may be taking longer before someone wants to purchase a desktop with a hard drive in it. The computer market is very diverse with many options like video game consoles, Roku, Tablets, Phones Phablets, so there is just less demand for a desktop computer.Summersnow - Saturday, May 21, 2016 - link

This is classic disruption. SSD started from the bottom in terms of capacity. HDD guys thought that was a toy and that HDD will forever be much cheaper $/GB.Problem is once SSDs hit a good enough capacity for $30 per drive oem price, that's the end of HDD. I believe the good enough capacity for 2.5" is 256GB. $30 is around the corner.

HDD has a floor cost. HDD cannot be produced for lower than floor cost by cutting capacity but flash can continuously shrink and deliver lower cost per GB in forseeable future. 2.5" HDD floor cost is probably $25. By the time ssd hits sub $20 for 256Gb, HDDs will have no choice but to give up. All entry level notebook PC models will go for ssd 256GB. HDD TAM will see a sudden huge drop when that happens.

Wolfpup - Thursday, July 14, 2016 - link

That stinks they're getting rid of people.One thing I never understood is why Seagate and Western Digital did pounce all over the SSD (emerging) market 10 years ago. Obviously some of the skill-set involved would overlap, it was obvious they'd become more popular. I guess Seagate's maybe done some enterprise drives? I'm not even sure... but I don't get why they're not one of the biggest names in SSDs...