Market Views: HDD Shipments Down 20% in Q1 2016, Hit Multi-Year Low

by Anton Shilov on May 12, 2016 8:00 AM ESTFinal Words

The storage market in the first quarter of 2016 performed in accordance with the PC market trends in general. Shipments of HDDs went down, but sales of high-capacity nearline hard drives remained a bright spot in the reports of leading hard drive suppliers. Western Digital remains optimistic in the short term for HDDs, but Seagate detailed plans to severely cut its production capacities and to reduce its presence the market of low-end mobile HDDs.

As ultra-thin notebooks, as well as 2-in-1 hybrid PCs, are gaining market share, the potential for 2.5” client HDDs suffers. Theoretically, sales of 2.5” drives for AIO and small form-factor desktops could offset declines in the mobile (at the expense of 3.5” HDDs declines), but this did not happen in Q1: sales of Seagate’s 2.5” client HDDs dropped to 10.6 million units (down 37% YoY), whereas shipments of Western Digital’s 2.5” client drives declined to 13.577 million units (down 28% YoY).

This quarter Seagate announced plans to discontinue some of its 2.5” low-capacity (500 GB and lower) client drives and concentrate on promoting 1 TB and 2 TB 2.5” models based on its latest technologies. Basically, Seagate no longer wants to compete against entry-level TLC NAND-based SSDs in low-end and mainstream notebooks. Reducing participation in this market segment will allow Seagate to simplify the portfolio of components it purchases from other makers and cut down its costs as high-capacity platters for advanced drives are made mostly in-house. It will be very interesting to see how other HDD makers respond to this action. They face similar problems and eventually it will only get harder to compete against cheap SSDs.

Shipments of 3.5” client hard drives hit a new low in the first three months of this year, which was not completely surprising, given slow shipments of PCs. So far neither Seagate nor Western Digital has announced plans to optimize their 3.5” lineups (WD actually folded its Green drives into its Blue lineup last year), but this is something that will likely happen in the future.

Enterprise HDD business is a mixed bag these days. On the one hand, sales of 10K and 15K HDDs are declining because of SSDs and that decline has yet to bottom out. Yet, those hard disks remain expensive and the business overall is profitable. On the other hand, sales of nearline drives are on the rise. More importantly, the growth of average capacities of such HDDs even outpaces the growth in their unit sales. Interestingly, Seagate indicated that demand for high-end 8 TB nearline HDDs was so strong in Q1 2015 that it could not even fulfill the orders placed. Seagate’s rather unexpected start of 10 TB HDD revenue shipments in April proves that operators of data center are rapidly building up capacities.

Seeing the fact that HDD sales volumes have been falling for many quarters now, Seagate not only decided to exit the market of low-end notebook drives but also detailed its plans to steeply cut-down its manufacturing capacities to 35 – 40 million units per quarter from 55 – 60 million units per quarter. From now on, the company will focus on high-capacity HDDs that are sold at higher prices rather than on affordable drives for bulk storage, which will naturally help it to avoid direct competition against SSDs in the entry-level segment where capacity may not be that important. It remains to be seen what Seagate will do with the manufacturing equipment that it will not need after its optimizations, but that is a different conversation entirely.

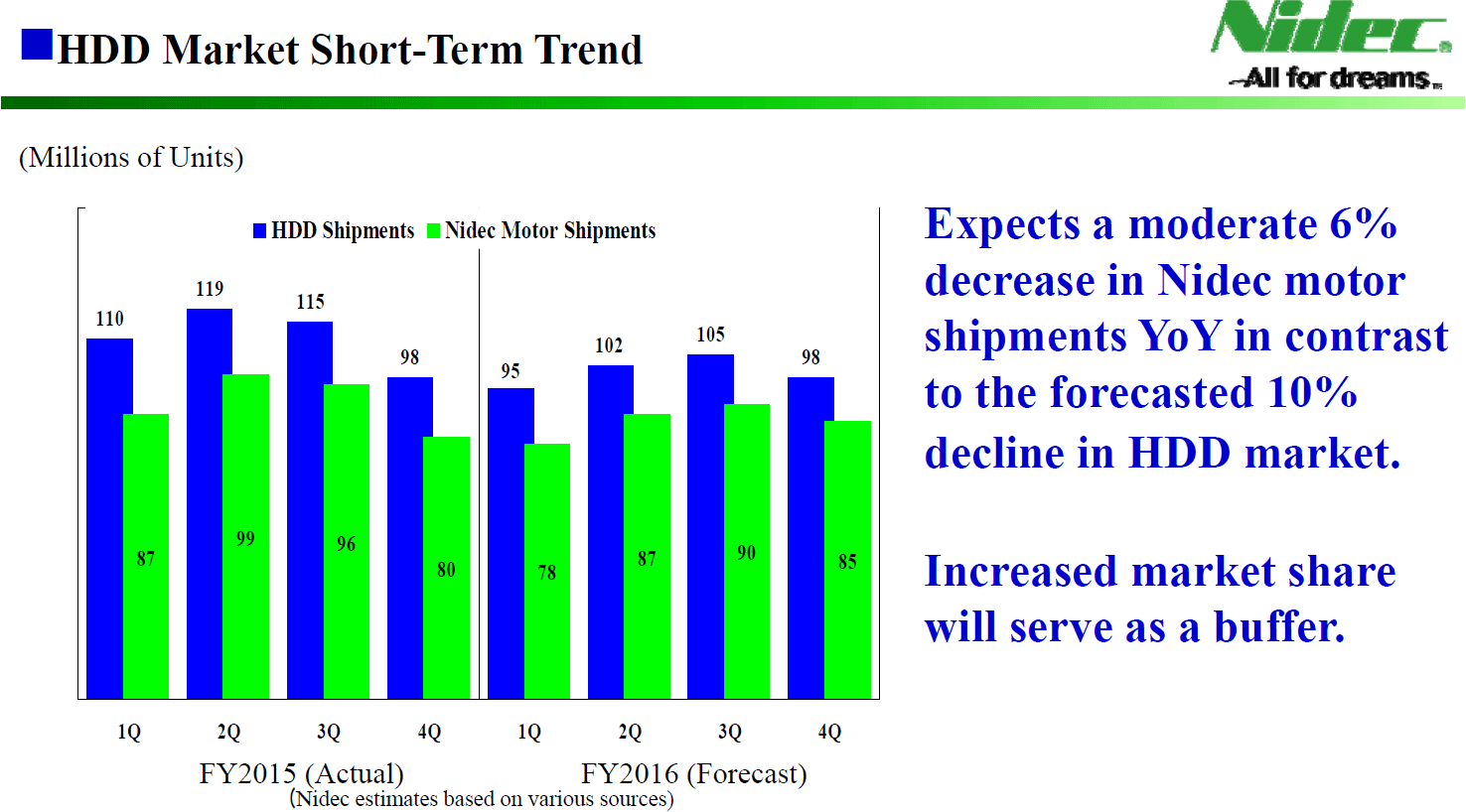

Looking ahead, Western Digital believes that the HDD TAM will remain above a psychologically important 400 million units per year mark (shipments of HDDs last year were around 453.6 million units), but will drop in the long term. Meanwhile, Nidec conservatively predicts that HDD TAM will fall to 400 million units in 2016 with shipments of PC and external HDDs declining the most. The upcoming quarters will show whether optimistic or conservative predictions are applicable to today’s HDD market.

Methodology and Important Notices

There are three major manufacturers of hard drives today: Seagate, Toshiba and Western Digital. Other suppliers are reselling hard drives made by these three companies.

Seagate and Western Digital reveal their HDD unit shipments as well as TAM (total available market) estimates every fiscal quarter. While such numbers are considered preliminary, they are usually rather accurate and re-affirmed by third-party analysts. Our TAM is the midpoint between Seagate’s and Western Digital’s TAM estimates. If only one hard drive maker reveals its TAM, we consider the number from only one vendor.

Meanwhile Toshiba does not officially disclose its HDD shipments. We subtract quarterly shipments of Seagate and Western Digital from our TAM estimate to get the number of drives sold by Toshiba. The approach is is the reason why we do not report historical shipments of Toshiba prior to Q3 2012. Based on estimates of hard drive makers and industry observers, Toshiba cannot produce more than 22 – 23 million of HDDs per quarter.

Seagate’s and Western Digital’s fiscal quarters end on the last business day of the last week of a calendar quarter (e.g., the Friday next to December 31). While fiscal quarters of HDD makers may not correspond exactly to calendar quarters, they are very close. Fiscal years of Seagate and Western Digital do not correspond to calendar years as they begin in July.

Historical TAM data comes from financial reports of Seagate and Western Digital.

Note 1: Seagate completed the acquisition of Samsung’s HDD business in December, 2011. The company started to include sales of Samsung-branded HDDs in its quarterly shipments in Q1 2012 (Q3 FY2012).

Note 2: Western Digital closed the acquisition of Hitachi Global Storage Technologies in March, 2012. Western Digital began to include HGST shipments in its financial reports in Q2 2012 (Q4 FY2012).

Note 3: Toshiba acquired some of Western Digital’s 3.5-inch HDD manufacturing equipment and intellectual property in May, 2012. It was expected that the manufacturing transfer could be complete within 6 to 12 months. Western Digital made HDDs for Toshiba on a contract basis until late Q4 2012. Due to the contract manufacturing agreement between Western Digital and Toshiba in 2012, there may be some inaccuracies in the historical data in that period (i.e., since the drives were made by Western Digital and then sold to Toshiba, they are attributed to the former, not the latter).

Note 4: Seagate defines client HDDs as 2.5” and 3.5” hard drives for desktops, notebooks and hybrid PCs as well as game consoles. Seagate considers HDDs for external storage and network-attached storage (NAS) as “branded” drives. Hard disks for DVRs and surveillance systems belong to Seagate’s family of HDDs for consumer electronics. Enterprise lineup includes 2.5” and 3.5” drives for mission critical (SAS, SCSI, Fibre Channel), enterprise storage, nearline and other datacenter applications.

Note 5: Western Digital attributes desktop and mobile 2.5” and 3.5” hard drives to client HDDs. External hard drives and NAS are referred to as “branded products”. Western Digital’s consumer electronics HDDs are used in DVRs, game consoles, video streaming applications and security video recording systems.

116 Comments

View All Comments

nils_ - Monday, May 30, 2016 - link

Is anyone still buying those 15k or even 10k drives?glad2meetu - Friday, May 13, 2016 - link

I think people are waiting to see what comes out of the merger between WD and Sandisk. I am surprised that Seagate did not make a bid late last year for Micron.I think much of the blame for the decline in the PC market in general is due to Intel failing to innovate. The drop in HDD shipments effectively just mirrors the lower number of new computers being shipped. But that may be a bit harsh on Intel and the rest of the PC industry. It has become much more difficult to make a game changing product given the level of excellence found in existing technology. The same can be said for smartphones.

Hard drives may turn around in another couple of years if designers can get hybrid drives to work as intended. Or perhaps 3D XPoint lives up to the hype and changes the market in another few years.

There also is a risk that the cost reduction on SSDs comes back to haunt them. General consumers will just lump all SSDs together or may view them based on brand names. So SSD makers could get hurt if the cheapest SSDs run into more issues for consumers.

avbohemen - Friday, May 13, 2016 - link

With these numbers, I am wondering: does this include disks delivered to the cloud providers (AWS, Azure, Google), Facebook and other big consumers? They are always expanding their datacenters and use a lot of storage, while no one seems to really know how big their "market share" is. Can anyone share some insight in this?Pix2Go - Friday, May 13, 2016 - link

The numbers in the article do include those customers. They typically are the ones using "Enterprise" drives, with some exceptions.As an idea of how many drives they need, consider this random nugget from "the internet":

"The volumes of storage Google needs are insane: as the post notes, YouTube alone requires a petabyte of new storage every single day."

Yep, at least 1000TB a day in new storage requirements. And I'd bet that's a low estimate.

This link doesn't give a solid answer, but gives some ideas about how much data is really out there. https://www.backblaze.com/blog/200-petabytes-of-cu...

revanchrist - Friday, May 13, 2016 - link

Couldn't agreed more with what some already said. The per GB price of HDD will not go further down, it will just stay stagnant. Right now the lowest per GB price is on 3TB and 4TB drives, once you go further up eyeing for 5TB and more, the prices simply rocket sky high. I think in the future, all those 1TB and 2TB drives will go extinct while 5TB and higher prices will drop down to the level of 3TB and 4TB. 1TB and lower storage space belongs to the SSD, and it will happen very soon.StrangerGuy - Friday, May 13, 2016 - link

My educated guess is that costs of HDDs doesn't scale well at the low end since HDD manufacturers still have to build the entire drive assembly minus platters for a 1TB or less HDD while NAND is far more flexible in physical packaging.zodiacfml - Friday, May 13, 2016 - link

LOL. I feel bad for these ageing kings of storage.They have to throw out their cash and apply for some loans to be build a NAND fab. It is the only way to stay relevant for the next 10 to 20 years. SSDs are already eating from the top and bottom of the food chain. The last remaining stronghold of HDDs is cost per GB; but SSDs doesn't have to go there as HDDs didn't replaced Tape drives for cost per GB.

zodiacfml - Friday, May 13, 2016 - link

Edit: Got carried away and forgot WDs acquisition of Sandisk which puts them on track. Seagate, just do it.vivekvs1992 - Saturday, May 14, 2016 - link

Most of the reasons for declining sales are because of steafy decline in the pricing of small to medium capacity ssd, hdd are used for long term storage nowadays and those drives are never below 1tb, personally i have 2 2tb usb hdd, 1 1tb usb hdd and a 2 tb in my build, and 2 more 2 tb beauties are on their way... The thing is many of my friends don't consider that they can add another hard disk without removing the old one in a desktop, another lot of them don't need so m7ch storage and the last lot are unaware of this data expansion methodFriendlyUser - Saturday, May 14, 2016 - link

For a lot of stuff we have gone from "owning" digital libraries to "subscribing". If people had to locally store their netflix content or their Amazon books and their MP3s, the need for space would have grown considerably. With a fast network you can always rely on re-downloading content you want, instead of storing.Also, in my opinion, the industry has stagnated. Price per GB is today similar to what I paid the last time I upgraded my HDs, in 2009. This is unacceptable. I know I would have bought a ton of 2.5" 2TB HDs for backups and the like, but they are still priced at ~$100. Too expensive... Plus, there has been little progress with hybrid HD/SSDs, which would be a great solution for people who don't want to mess with multiple drives. In fact, all I see is rebranding the same drive with slightly modified firmware and selling it as "NAS" or "workstation" or "IP camera" or "NAS pro" or "Storage" etc.

They have been milking us for too long. Time to start innovating.