Intel Announces Record Quarterly Revenue And Full-Year Revenue For Q4'2016

by Brett Howse on January 26, 2017 10:00 PM EST- Posted in

- CPUs

- Intel

- Financial Results

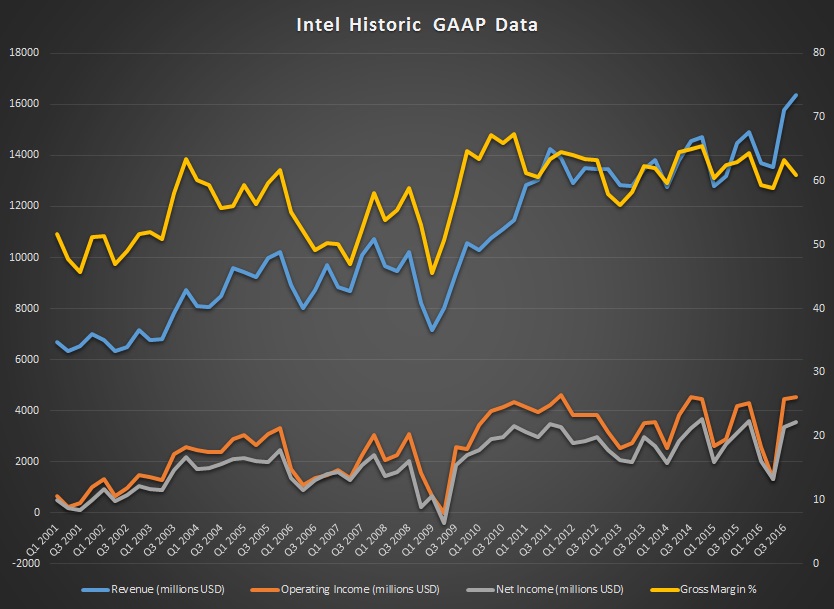

This afternoon, Intel announced their quarterly earnings for the fourth quarter of their 2016 fiscal year. Intel set a new record for revenue for this quarter, coming in at $16.4 billion. This is up 10% from a year ago. For the year, Intel brought in $59.4 billion, up 7% from their 2015 results. Intel’s gross margin fell 1.7 points to 60.9%, and they had an operating income of $12.9 billion, which is down 8% from a year ago. Net income was down 10% to $10.3 billion, and earnings per share fell 9% to $2.12.

Intel also reports Non-GAAP results, which exclude several expenditures, such as acquisition-related adjustments, write-downs, and the like. On a Non-GAAP basis, Intel had a gross margin of 63.1%, down 1.7 points, an operating income up 11% to $4.9 billion, and a net income up 4% to $3.9 billion. Non-GAAP earnings per share were up 4% to $0.79.

| Intel Q4 2016 Financial Results (GAAP) | |||||

| Q4'2016 | Q3'2016 | Q4'2015 | |||

| Revenue | $16.4B | $15.8B | $14.9B | ||

| Operating Income | $4.5B | $4.5B | $4.3B | ||

| Net Income | $3.6B | $3.4B | $3.6B | ||

| Gross Margin | 60.9% | 63.3% | 62.6% | ||

| Client Computing Group Revenue | $9.1B | +2.2% | +3% | ||

| Data Center Group Revenue | $4.7B | +4.4% | +3% | ||

| Internet of Things Revenue | $726M | +5.3% | +5% | ||

| Non-Volatile Memory Solutions Group | $816M | +26% | +26% | ||

| Intel Security Group | $550M | +2.4% | +2% | ||

| Programmable Solutions Group | $420M | -9.7% | -1% | ||

| All Other Revenue | $65M | +47.7% | +10% | ||

The gross margin impact is being attributed to a few things. Warranty and IP charges increased, as did spending on factory start-ups, due to the move to 10 nm coming this year, Client Computer Group non-platform costs, and the Non-Volatile Memory Solutions Group margins. Intel very much likes to keep their margins up above 60%, and for the moment they are still there even with these extra costs.

Intel breaks the company down into several groups. The main group is the Client Computing Group, which as the name implies, provides CPUs, SoCs, and wireless and wired connectivity products destined for PCs. Although the PC market is still down, this group had revenue for the year of $32.9 billion, which is up 2%, but platform volume is down 10%. Platform selling prices were up 11%, which makes up the difference. For just the last quarter, Client Computing Group had revenues of $9.1 billion, up 4% from a year ago. Platform volumes were down 7%, offset by selling prices up 7%. Desktop platform volume was down 9%, while notebook volumes were flat. Desktop average selling price (ASP) was up 2%, and notebook ASP was up 3%. Considering the down market, Intel continues to drive revenue here. While good for them, it means prices are high, and some competition in this space might help out the consumer.

The Data Center Group also had a strong quarter, and year. For the year, they had revenue of $17.2 billion, up from $16.0 billion a year ago. For the year, Intel saw volumes up 3% and ASP up 4%. For the most recent quarter, the Data Center Group had revenues of $4.7 billion, which was up 3%. Platform volumes were down 3%, with ASP up 6%.

Intel is slowly building it’s Internet of Things group, which had revenues for the year at $2.6 billion, up from $2.3 a year ago. Revenue for this quarter was up 5% to $726 million. The Non-Volatile Memory Solutions group had revenues for the quarter of $816 million, up 26% from a year ago, and a full-year revenue of $2.58 billion, down slightly from the $2.6 billion a year ago. Programmable Solutions is new for Intel this year, with the purchase of Altera, and this segment had revenue of $420 million for this quarter, and $1.7 billion for the year. All other revenue was $65 million for the quarter, up from $59 million a year ago.

2016 was a strong year for Intel, although it was not without its challenges. Earlier this year, Intel decided to get out of the mobile SoC space completely, abandoning it’s Atom architecture for this segment. Atom does live on for low power PCs, but any of the tablets that used the Cherry Trail Atom have found themselves without a new CPU to move to. The death of Tick-Tock also had its first new entrant in Kaby Lake, although you could easily argue Devil’s Canyon was a similar situation. But they have several new exciting technologies coming to market as well, such as 3D X-Point, and of course the expected launch of their 10 nm CPUs later this year.

Looking forward to Q1 2017, Intel is forecasting a midpoint revenue range of $14.8 billion, with margin estimates at 62%.

Source: Intel Investor Relations

20 Comments

View All Comments

Nagorak - Saturday, January 28, 2017 - link

Yeah... most people involved in the stock market really don't know what they're doing. Some make some big bets and do well for a while but they end up flaming out. Most just end up following the herd and buying when things are expensive and selling when they are cheap. I'm certainly not impressed with the majority involved in the financial markets--including the "pros".duploxxx - Friday, January 27, 2017 - link

The monopoly they have is on the edge of being dangerous. Yet many IT organisations will always and only buy from the djingle company in every segment even if there are other choices that are as good as.In the end the cost is just higher for everybody since there is no competition.... poor human mind. Praise HPinc and HPe for not being a sheep.

Gothmoth - Friday, January 27, 2017 - link

the intekl monopoly has to be broken.i wish AMD all the best.

i will probably not buy an ryzen this year but i hope many people do.

since 2004 i use intel but this monopoly has to stop.

only ~30% more performance from sandy bride to kaby lake.. that alone is enough to wish for competition.

Michael Bay - Friday, January 27, 2017 - link

Monopoly of electron physics is a terrible thing, indeed.patrickjp93 - Friday, January 27, 2017 - link

There's more than 100% performance improvement from Sandy Bridge to Kaby Lake if you have software that properly takes advantage of AVX2. For all those extensions which AVX1 didn't cover, the throughput over SSE1/2/3/4 is double.The problem with performance gains is not Intel. It's software. Even games make very little use of SSE1/2/3/4 which are already 4x as powerful as standard scalar code.

JKflipflop98 - Friday, January 27, 2017 - link

You should go look up the definition of the word "monopoly". You're using it wrong.Alexey291 - Saturday, January 28, 2017 - link

Depending on the situation monopoly can mean anything from 'single company in the market' through 'controls over 50% of the market's sales'.Obviously people tend to pick the definition that suits them best.

TristanSDX - Friday, January 27, 2017 - link

"Looking forward to Q1 2017, Intel is forecasting a midpoint revenue range of $14.8 billion, with margin estimates at 62%."Look like they know that Ryzen is crap, or their management is super arogant

Haawser - Friday, January 27, 2017 - link

After years of pleading from customers it seems that Intel have finally decided to release Pentiums with HT and unlocked i3's... Now you *could* (if you were mentally unstable) put this down to the goodness of their hearts and desire to 'do right' by their loyal customers.Or you could just see things how they really are, and see that Ryzen has them rattled. ;)

coolhead - Friday, January 27, 2017 - link

AMD is no longer a good buy, AMD is now an extremely risky buy as the wave is over it's the wait and see period. The thing is yeah Zen will probably eat some of Intels money and make AMD some cash, but you have to remember AMD being competitive is keeping companies like ARM at bay from entering the market and what is good for x86 is good for intel