Intel Reports Q1 2020 Earnings: Another Strong Quarter For Both Client and Datacenter

by Ryan Smith on April 24, 2020 9:30 AM EST- Posted in

- CPUs

- Intel

- Financial Results

Kicking off earnings season for the tech industry, Intel yesterday evening reported their financial results for the first quarter of the year. And, like pretty much every Intel quarter for the last couple of years, it was a doozy, with Intel once again recording growing revenues and a very healthy profit margin.

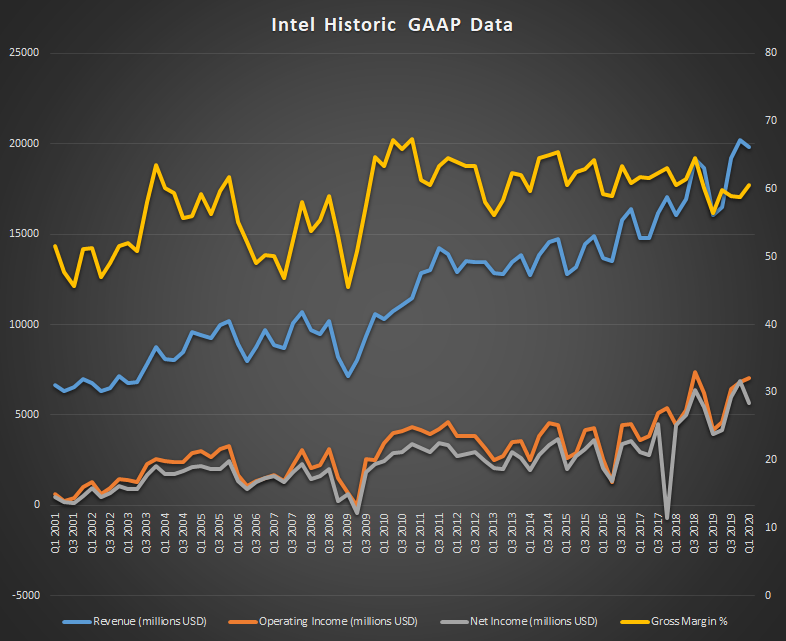

For the first quarter of 2020, Intel reported $19.8B in revenue, a significant improvement over the year-ago quarter, and only slightly behind Intel’s record-breaking Q4. As a result of this strong revenue, income was also very healthy for the company, with Intel recording $5.7B in net income, a 43% jump over Q1’19. Meanwhile gross margins were up 4 percentage points to 60.6%, pushing Intel back above their much revered 60% gross margin threshold.

| Intel Q1 2020 Financial Results (GAAP) | |||||

| Q1'2020 | Q4'2019 | Q1'2019 | |||

| Revenue | $19.8B | $20.2B | $16.1B | ||

| Operating Income | $7.0B | $6.8B | $4.2B | ||

| Net Income | $5.7B | $6.9B | $4.0B | ||

| Gross Margin | 60.6% | 58.8% | 56.6% | ||

| Client Computing Group Revenue | $9.8B | -2% | +14% | ||

| Data Center Group Revenue | $7.0B | -3% | +43% | ||

| Internet of Things Revenue | $1137M | -2% | +8% | ||

| Non-Volatile Memory Solutions Group | $1.3B | +8% | +46% | ||

| Programmable Solutions Group | $519M | +3% | +7% | ||

Breaking things down on a group basis, many of Intel’s internal reporting groups saw double-digit growth over the year-ago quarter. Client computing revenue was up 14% to $9.8B, and data center revenue was an even bigger winner with $7.0B in revenue, a 43% jump over the previous year. The significant growth in the data center segment comes as Intel saw both higher average selling prices and higher volumes overall, with ASPs and volumes growing by 13% and 27% respectively. Overall Intel attributes the data center gains to the company’s “broad strength” in the market, though they did note that they’ve seen a 53% year-over-year increase in revenue from cloud service providers.

As for client computing revenue, the biggest gains there came from notebook ASPs, which were up 22% over the year-ago quarter. Other client metrics were relatively tame; notebook volumes actually slipped 3%, while on the desktop, ASPs were up 4% while volumes were down 4%. For Intel’s client group, the company is coming off of the second quarter of selling Ice Lake laptops, with improving supply and improving helping to drive those numbers. As well, Intel’s new Comet Lake-H CPUs were recently launched, which means those would have been shipping to OEMs in Q1 as well.

Rounding out Intel’s product portfolio, the company recorded smaller gains for their Programable Solutions Group, as well as their Internet of Things business. Overall IoT was a mixed bag: Mobileye revenue, which the company offers a separate breakout, was up 22% over the previous year, but the rest of Intel’s IoT business saw a 3% drop in revenue. Finally, Intel’s storage group was a surprising winner, with record revenue pushing them to year-over-year growth of 46%, thanks to higher NAND ASPs and lower unit costs.

Meanwhile, like most other tech companies, the 800lb gorilla of the chipmaking world finds itself in an interesting position as the novel coronavirus pandemic has shuttered large parts of the world’s economies. For Q1, Intel believes they actually benefitted somewhat from the outbreak, as companies and consumers needed to make previously-unplanned purchased of laptops and other equipment for working from home and remote learning. However as the pandemic continues, it’s likely to start impacting Intel’s sales in other ways, as idled business won’t be making their usual purchases and expansions. As a result, Intel isn’t even providing full-year financial guidance due to the economic uncertainty that the pandemic has caused.

On the flip side of the coin, as a business and employer themselves, the coronavirus outbreak has also threatened Intel’s manufacturing operations. Despite that, according to Intel the company was able to keep all of its essential manufacturing operations going, with an on-time delivery rate that’s still better than 90%. So thus far Intel seems to have weathered the first part of the pandemic fairly well.

All eyes then will be on the second quarter, both for continuing developments with the coronavirus pandemic, as well as Intel’s own internal manufacturing efforts. With Intel set to start shipping its 10nm Tiger Lake CPUs to OEMs by mid-year, the company is going to be pushing its 10nm manufacturing lines harder than ever as they ramp up for a new generation of CPUs. While slowly improving, 10nm’s rocky bring-up remains a bit of a proverbial albatross around Intel’s neck, so further improving capacity and yields will go a long way towards helping Intel maintain its success, especially in light of heavy competition from AMD.

Source: Intel

49 Comments

View All Comments

AshlayW - Sunday, April 26, 2020 - link

Not a great thing for the consumer, given Intel's history. AMD has superior products in almost all areas now, and people are learning that.Spunjji - Tuesday, April 28, 2020 - link

"I'm clever because I mock people with disabilities"Yeah, go you, big man here.

Massive, cash-rich company maintains dominant market position despite inferior products in most relevant categories. News at 10.

alufan - Monday, May 4, 2020 - link

LOLits a slow road to beat a "competitor" that hands out billions in rebates and incentives to keep the competition out, however in non commercial settings AMD is beating intel hands down and once the 4000 CPUs are on open availability we will see a big shift in the market, unfortunately for AMD the Covid19 outbreak and the resultant massive uplift in Laptpops for home working will mean the market will be slower for a while as there will be a glut within most companies after all this, but it will still shift.

Data centre is starting to shift intels own results show that and the results correlate with AMDs, competition is good for us all and frankly intel needs to put its house in order.

BTW AMD was in this position many years ago then intel launched core2duo that was intels "Ryzen" blow to AMD and I believe Intel will be behind for some time to come

AshlayW - Sunday, April 26, 2020 - link

Anti-competitive practises paying off as usual for Intel.Also, I don't have words to describe my contempt for some of the users on here; their flagrant bias (whether by delusion or financial investment) is telling, and sickening.

BenSkywalker - Tuesday, April 28, 2020 - link

You complain about flagrant bias directly after claiming Intel is being anticompetitive?Offering special kickbacks to large scale buyers is considered 'competitive', not 'anticompetitive'. AMD should maybe consider going the same route and dropping their toxic vial marketing campaign.

AMD is doing well on the CPU side being a great offering for all builds outside of pure gaming(and they aren't *terrible* there either), but their GPU side is regurgitated fecal matter being as kind as possible(full node advantage and struggling with fourth tier parts.......).

Tilmitt - Monday, April 27, 2020 - link

How do these guys rerelease Skylake for 5 years in a row and keep growing revenue? That's actually an achievement in itself when you think about it.Spunjji - Tuesday, April 28, 2020 - link

Tech markets are more about marketing agreements and supply capability than tech. As long as the market itself grows, Intel's share grows, because as far as most customers are concerned Intel *is* the market.Teaming up with Nvidia to lock out the high-end gaming laptop market and continually raise ASPs has obviously helped a bunch, too. It pisses me off how that has been treated as completely acceptable by consumers and the tech press.

ingwe - Monday, April 27, 2020 - link

Can we get the process graph in semilog? It feels unhelpful with a linear scale.Lakados - Monday, May 4, 2020 - link

This isn't overly surprising, even with AMD having the current lead in performance over Intel for their parts lineup AMD is not capable of producing those parts in a sufficient quantity to pose a real threat to Intel at this time. TSMC doesn't have as many fab plants as Intel does, and AMD shares that fab time with over a dozen other companies, Intel included. They simply can't get their stuff built in a large enough quantity for any OEM to seriously launch a mainstream laptop/desktop with. Until AMD can increase their delivery capabilities by at least 10x of what they currently are Intel will continue to crush markets.