Intel Announces Q3 FY 2019 Earnings: Record Results

by Brett Howse on October 24, 2019 11:10 PM EST- Posted in

- CPUs

- Intel

- Financial Results

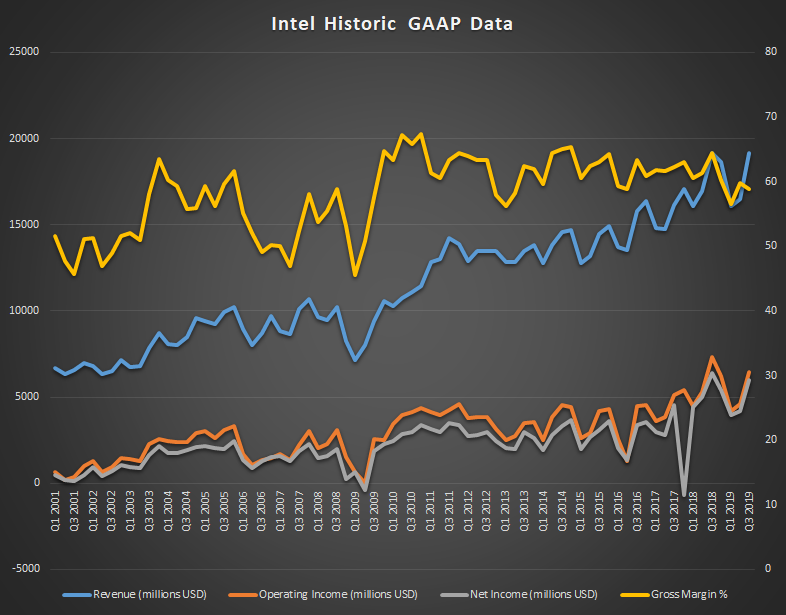

Today Intel announced their earnings for the third quarter of the 2019 fiscal year, which ended September 29, and the company has set a record for revenue thanks to increased growth of their datacenter business. Revenue for the quarter came in at $19.2 billion, beating Q3 2018 by $27 million, which results in a mere 0.14% growth over last year, but enough to make this the highest revenue ever for the company. Gross margin was 58.8%, down from 64.5% a year ago. Operating income was down 12% to $6.4 billion, and net income was down 6% to $6.0 billion. This resulted in earnings-per-share of $1.35, down 2% from a year ago.

| Intel Q3 2019 Financial Results (GAAP) | |||||

| Q3'2019 | Q2'2019 | Q3'2018 | |||

| Revenue | $19.2B | $16.5B | $19.2B | ||

| Operating Income | $6.4B | $4.6B | $7.3B | ||

| Net Income | $6.0B | $4.2B | $6.4B | ||

| Gross Margin | 58.9% | 59.8% | 64.5% | ||

| Client Computing Group Revenue | $9.7B | +10% | -5% | ||

| Data Center Group Revenue | $6.4B | +28% | +4% | ||

| Internet of Things Revenue | $1.0B | +1% | +9% | ||

| Mobileye Revenue | $229M | +14% | +20% | ||

| Non-Volatile Memory Solutions Group | $1.3B | +38% | +19% | ||

| Programmable Solutions Group | $507M | +3.7% | +2% | ||

Intel splits their business into two main areas. The Client Computing Group is the PC-Centric products, and the Data Center Group consists of everything else. Despite the contraction of the PC market over the last several years, it has continued to be the main source of revenue for Intel, and that continues this quarter as well, but only by a small margin. The Client Computing Group revenue was down 5% year-over-year to revenue of $9.7 billion. Intel attributes this drop to lower year-on-year platform volume, although loss was partially offset by some of the higher-cost products especially in the commercial segment.

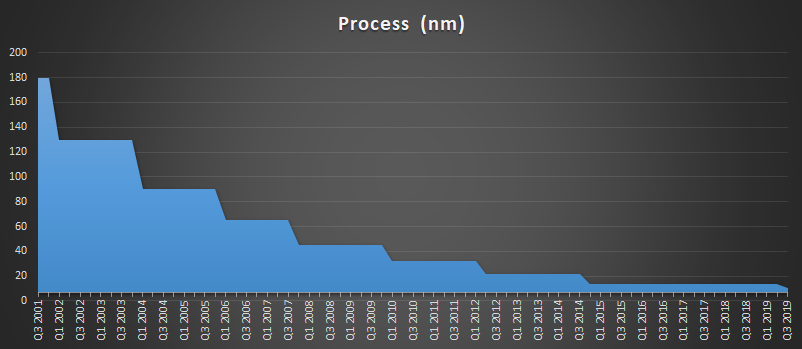

Although the overall PC side from Intel was down, Intel has only just launched their latest 10th generation Core products which won’t make up much of Q3’s numbers due to the cut-off date of the end of September. Intel now has over 30 devices launched based on the 10 nm Ice Lake platform, signalling the end of 14 nm which has been iterated on many times over the last several years as Intel struggled to get their 10 nm process off the ground. The good news for Intel is that despite the initial setbacks for 10 nm, they have stated that 10 nm yields are actually ahead of their internal expectations for this point in its lifecycle, which should help alleviate some of the backlog the company has been facing with production assuming the can use the improved yields to transition more of their lineup over to 10 nm a bit quicker. Intel has also stated that despite the years lost on 10 nm, they are moving back to a 2 to 2.5 year process cadence, with 7 nm on track for their GPU lineup in 2021.

Intel lumps the rest of their business into the “Data-Centric” role, and this side of the company has been making strong gains over the last several years, and now almost matches the Client Computing Group in total revenue at $9.5 billion, versus $9.7 billion for the CCG. But Data-Centric includes not only the Data Center Group, but also Internet of Things, Mobileye, Non-Volatile Storage, and Programable Solutions. Altogether these segments achieved record revenue, up 6% from 2018. Individually, Data Center Group was up 4% to $6.4 billion with a strong mix of Xeon sales and growth in all segments. Internet of Things also had record revenue, up 9% to $1.0 billion. Mobileye is also on the record train, with a 20% year-over-year gain to $229 million, as did Non-Volatile Storage which was up 19% to $1.3 billion. Programable Solutions was the only segment in the Data-Centric listings to not hit a record in revenue, but it was still up 2% to $507 million for the quarter, and they shipped their first 10 nm Agilex FPGA this quarter as well.

Looking ahead to Q4, Intel is expecting revenue around $19.2 billion with earnings-per-share of $1.28.

Source: Intel Investor Relations

39 Comments

View All Comments

FreckledTrout - Friday, October 25, 2019 - link

It is different this time. All the big cloud providers want, no need, a second cpu provider. They will buy AMD just to make that happen. Hell Amazon was making their own CPU just to have another option. No intel cant buy there way out this time but frankly I don't think they will need to result to anything like that other than price cuts, if they execute properly going forward.yannigr2 - Friday, October 25, 2019 - link

All will depend on 7nm. If 7nm come out in 2021, Intel can recover pretty quickly. We see it with the first Core CPU. If 7nm gets delayed, Itel will start having real problems.Targon - Friday, October 25, 2019 - link

7nm won't come in 2021 from Intel, except maybe initial laptop sales. There is a big question about any design improvements from Intel, because if they claim a 15 percent IPC boost due to fixing the security problems, then they may be at the same performance levels as they were in 2017 before the security mitigations first started showing up. If clock speeds are down by 20+ percent due to new process node, that's a net loss in performance between the new chips and the old 14nm++++ chips.imaheadcase - Friday, October 25, 2019 - link

People often forget Intel and others have hands in MANY business ventures other than pure CPU. The jump from 14nm to 7nm is not as important as you think it is in the grand picture of a business.sgeocla - Friday, October 25, 2019 - link

First Intel 10nm process node with "aggressive" scaling was expected to yield around 100M tr/mm2, which is about 2.3x original 14nm and about 2.7x 14nm++ which has decreased density vs 14nm.OEMs have reported Intel shortages for more than 1 year now, so if you think making more than 3.5x the number or chips on a new 7nm node wafer vs 14nm is not a big deal you don't really understand how the semiconductor industry works.

Keep this in mind as AMD pushed more cores each year and every 14nm Intel wafer makes less and less CPUs that need more cores to compete.

Keep this in mind as AMD pushed more cores each year and every 14nm Intel wafer makes less and less CPUs that need more cores (and die space) to compete.

FreckledTrout - Friday, October 25, 2019 - link

I gree. Intel planned fab capacity based off the fact they would be on 10nm well before now and they missed that mark hard. So now they simply cant make enough chips since they are not getting more chips per wafer with 10nm.tiwi1391 - Friday, October 25, 2019 - link

There are still issues though, like Intel promising FPGAs for 2017 to industry partners and then getting released last month...ilt24 - Friday, October 25, 2019 - link

@tiwi1391 ... "promising FPGAs for 2017 to industry partners"they fixed that problem by buying that industry partner.

deil - Friday, October 25, 2019 - link

its not issues with 10 nm itself just overaggressive target. if they will build that 10 nm node on 7 nm process, its already will be enough to keep them afloat propably up to 65W, and at least competitive. AMD will be the king of top performers for next few years, or decade intel lost momentum in there.Drumsticks - Friday, October 25, 2019 - link

It will certainly be impressive if they can keep it, though. TSMC Launched their first 7nm mobile processor in Q32018. HVM for 7nm was in Q2 2018. Their first 5nm HVM is coming in Q2 2020. So maybe we'll see a 5nm iPhone in 2020. Intel is launching a 7nm GPU in 2021. Sure, it's a year late, but they'll be launching with a much bigger die. I wouldn't be surprised if Intel's 7nm tech comes out at the same time as TSMC 5nm tech of a comparable size. That would be a hell of a quick turnaround for such a big ship - even parity with TSMC would be a big win for Intel, I think.