Intel Xeon Update: Ice Lake and Cooper Lake Sampling, Faster Future Updates

by Anton Shilov on May 9, 2019 11:00 AM EST

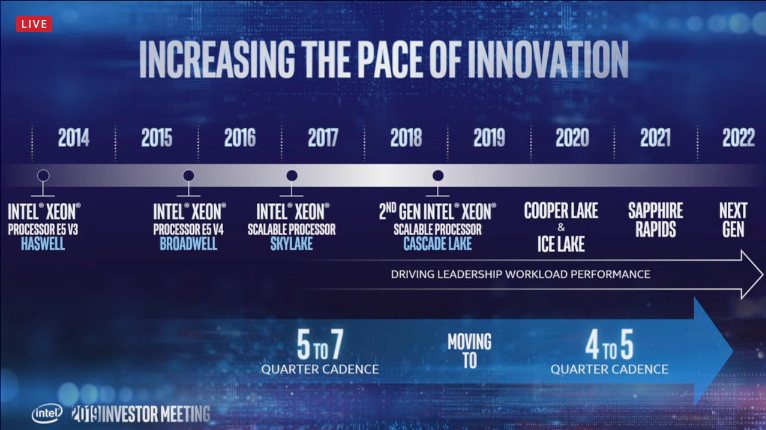

Emerging workloads will require considerably higher performance, and in order to solve upcoming challenges Intel has adjusted its product roadmaps quite significantly. One of the key things that Intel confirmed during its Investor Meeting event this week is shortening its Xeon introduction cadence from 18-24 months down to 12-15 months, thus accelerating its server CPU roadmap.

In the coming months Intel will launch two Xeon processors that will belong to the same platform: Cooper Lake CPUs made using Intel’s 14 nm manufacturing technology, and Ice Lake chips produced using Intel’s 10 nm node. Cooper Lake will offer high core counts and will exclusively support AVX512_BF16 (bfloat16) instructions that will benefit machine learning and near-sensor computing applications, whereas Ice Lake is set to become Intel’s first Xeon made using 10 nm process technology and based on a new microarchitecture offering higher per-core performance. At present, Intel is already sampling Cooper Lake and Ice Lake processors with customers, and claims that it is on track to ship these CPUs in volumes in the first half of next year.

Intel will launch its Ice Lake Xeon processors around four quarters after its Cascade Lake Xeon processors, a shorter than usual timeframe between Xeon releases. According to the chip giant, this will become its new introduction cadence and going forward it will release new generations of Xeon platforms every four to five quarters, down from five to seven quarters today.

Following the Ice Lake Xeon in 2020, Intel plans to release 'Sapphire Rapids' processors for servers in 2021. These chips will likely be made using Intel’s 10++ nm process technology and will rely on a new microarchitecture along with various enhancements to optimize performance in various workloads. We expect the platform to support new connectivity standards given the introduction timeframe. Meanwhile, it is too early to discuss CPU core count, platform capabilities, and other peculiarities. Following the Sapphire Rapids will come Intel’s ‘Next-Gen’ server CPU in 2022 that may be made using a variation of Intel’s 7 nm process technology, depending on how production goes.

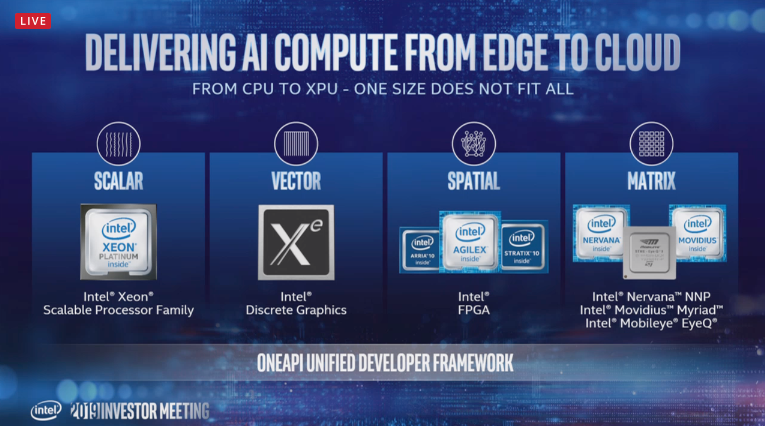

Intel’s Xeon processors will continue to be the company’s key components for datacenters, but there will be a host of other products for other datacenter workloads, including Xe GPUs, a variety of FPGAs and others. Having acquired or developed loads of different IP in the recent years, Intel pins a lot of hopes on its diversified product portfolio that will complement next-gen Xeons.

Related Reading:

- Intel Architecture Manual Updates: bfloat16 for Cooper Lake Xeon Scalable Only?

- Intel Server Roadmap: 14nm Cooper Lake in 2019, 10nm Ice Lake in 2020

- An Interview with Lisa Spelman, VP of Intel’s DCG: Discussing Cooper Lake and Smeltdown

- Intel Documents Point to AVX-512 Support for Cannon Lake Consumer CPUs

- Cisco Documents Shed Light on Cascade Lake, Cooper Lake, and Ice Lake for Servers

- Intel’s Xeon Scalable Roadmap Leaks: Cooper Lake-SP, Ice Lake-SP Due in 2020

Source: Intel

29 Comments

View All Comments

PeachNCream - Thursday, May 9, 2019 - link

It's very much a paper assault and a positive spin on the latest ugly situation that is lowering the share value. Apparently there's no reason to be bullish about the company's financial outlook until around 2023 when 7nm chips finally start looking more competitive...assuming the competition remains reasonably stagnant until then which may not be the case at all.https://www.marketwatch.com/story/intel-stock-fall...

HStewart - Thursday, May 9, 2019 - link

Stock looks level to me as of 1pm - and others are down, AMD to a sharp turn down today - but went back up - so above quote are probably don't like Intel. This is no official statement when 7nm is competitive. Just that Xe will get it first and in 2021 not 2023.PeachNCream - Thursday, May 9, 2019 - link

I hold Intel shares. They're down nearly 5% right now (an hour after your comment). That's not level by any stretch of the imagination. While I'm not worried about the day to day performance since I'm in this for dividends and my portfolio is diverse, indications are pointing to weakened performance for the next four years. In Intel terms, weakened performance is still just fine since the gross margin ought to hang around an obnoxious +50%, but that is down considerably from their usual performance.As for this BS - "This is no official statement when 7nm is competitive."

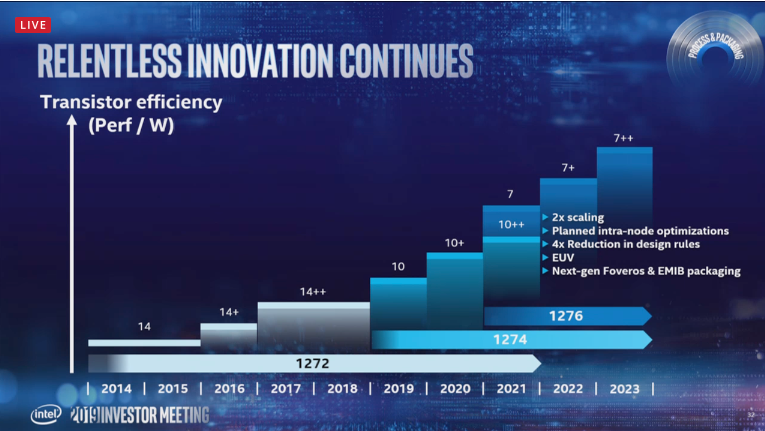

We have - "While Intel's first 7 nm product will be launched in 2021, Intel stresses that high-volume manufacturing (HVM) using the technology will begin in 2022 when the technology will be used not only for a server GPU, but also a server CPU."

Which is from this article that you seemingly read and commented on starting yesterday - https://www.anandtech.com/show/14311/intel-process...

So you can see with production ramp-up happening in 2022 for 7nm on server chips, volumes for purchase will likely hit the markets sometime in 2022 and consumer chips on the same process node are likely going to arrive in 2023.

Honestly, I'm not sure why I just wasted all that time typing at you. You're intentionally ignorant and blindly brand loyal. Heck, I have investments in Intel and even I'm not standing around with pom-poms waiting to shake my money makers when Intel encounters the least bit of trouble. You have some unresolved issues.

CiccioB - Thursday, May 9, 2019 - link

Well, this view is not entirely true.Intel stock is loosing value not because of this talking about 10 or 7nm, but for two other main reasons:

1. Trump sentences about China's trade deals which put clouds on the entire economy progress

2. Linked to the above, the fact that Intel business depends heavily on big data center orders, and seen Intel already has given an outlook of flat market for the entire 2019, reason n.1 is putting more doubts on its flatness rather than being downwards.

You can see nvidia following the same path, being hit more hardly han others in the market.

AMD, which just has crumbles in data center market is not going to suffer this economic negative momentum as everyone knows that if they manage to increase their presence in the DC market of just one point they are going to make a lot of money more than the none they are doing now (while 1% less in Intel is almost unnoticeable, but the problem are not the 1 less, its the 20% less they write in Q1 financial report).

As soon as the China deal will resolve Intel (and nvidia incidentally) will probably be the ones to gain most of the advantages and their stock will recover as fast as they have lost.

You see, AMD stocks were gaining nothing (returning on par after an initial boom) after Lisa Su said that Zen will start doing some real competition not before 1.5 year from now, which means that Intel has all the time to create it new architecture at 10nm and be there to fight at that critical moment, when Zen will be mature enough to be chosen for new installations.

Loosing some % in DC market in favor of a good Zen (and its better PP) is not a problem if the market grows. The real treat to Intel is not their technical offer now or in 18 months, but the flat or worse shrinking market, if Trump does not stop all that economic threats against the ones that have the capitals, pay USA debts and provide raw resources for USA own tech industries.

PeachNCream - Thursday, May 9, 2019 - link

I specifically pointed out that the short term stock valuation is not the central point.peevee - Thursday, May 9, 2019 - link

In terms of share price and business overall, Intel has a lot of risks ahead of it, some shared with competition and some not. It is very likely than MORE THAN ONE of those risks will actualize, so it is pretty insane to invest in Intel now.Some of the big ones (risks, none are certainties but possibilities):

- Corporate transition to Win10 with new desktops and laptops is almost over and will be over before the end of the year with Win7 going EOL, meaning that corporate sales will plummet.

- Corporate server transition to cloud servers at AWS and Azure will be over the next couple of years, after which shared resource model will not require previous rate of purchases.

- Strong competition from upcoming Ryzen 3000 on desktop, in only a month or two.

- Very strong competition from next EPYC in servers.

- Very probably failure of the first discrete GPU in many years in the face of Nvidia and AMD competition on TSMC and/or Samsung processes.

- Inability of Intel's "10 nm" to reach competitive frequencies

- Inability of Intel's "10 nm" to reach cost savings compared to their own "14 nm", let alone TSMC's "7 nm" or "6 nm", so upcoming 10nm volume production would hurt their bottom line.

- Possible delays of Intel's "7nm".

- Apple switching their MacOS products to their own ARM-based CPUs.

- adoption of ARM for cheap Windows laptops and Chromebooks.

- cloud gaming killing the demand for new CPUs and GPUs (including the new Intel's GPU)

- next recession.

What is the probability of none of them materializing?

smilingcrow - Thursday, May 9, 2019 - link

You missed out plagues of locusts and the great flood.mode_13h - Friday, May 10, 2019 - link

Good point. Perhaps a bomb cyclone floods out one of Intel's fabs.On the flip side, perhaps Samsung or TSMC are even more susceptible to climate change-related outages.

HStewart - Thursday, May 9, 2019 - link

Well June will tell if it is a paper assault or not - Ice Lake laptops are suppose to be revealed at 2019 Comdex and ready for shipping in June.Paper assaults comments belong on WCCFtech.

sa666666 - Thursday, May 9, 2019 - link

No, you and your idiotic shilling belong on WCCFTech. When are you going to get the point that everyone here sees right through your blatant attempts at propping up Intel no matter what the announcement actually says.To be clear, I don't think most people care about Intel _or_ AMD that passionately; they just can't stand your drivel. IOW, _you_ are the one that's unwelcome and don't belong here.