TSMC: 7nm Now Biggest Share of Revenue

by Ian Cutress on January 17, 2019 9:00 AM EST- Posted in

- Semiconductors

- TSMC

- 7nm

- CLN7FF

- Revenue

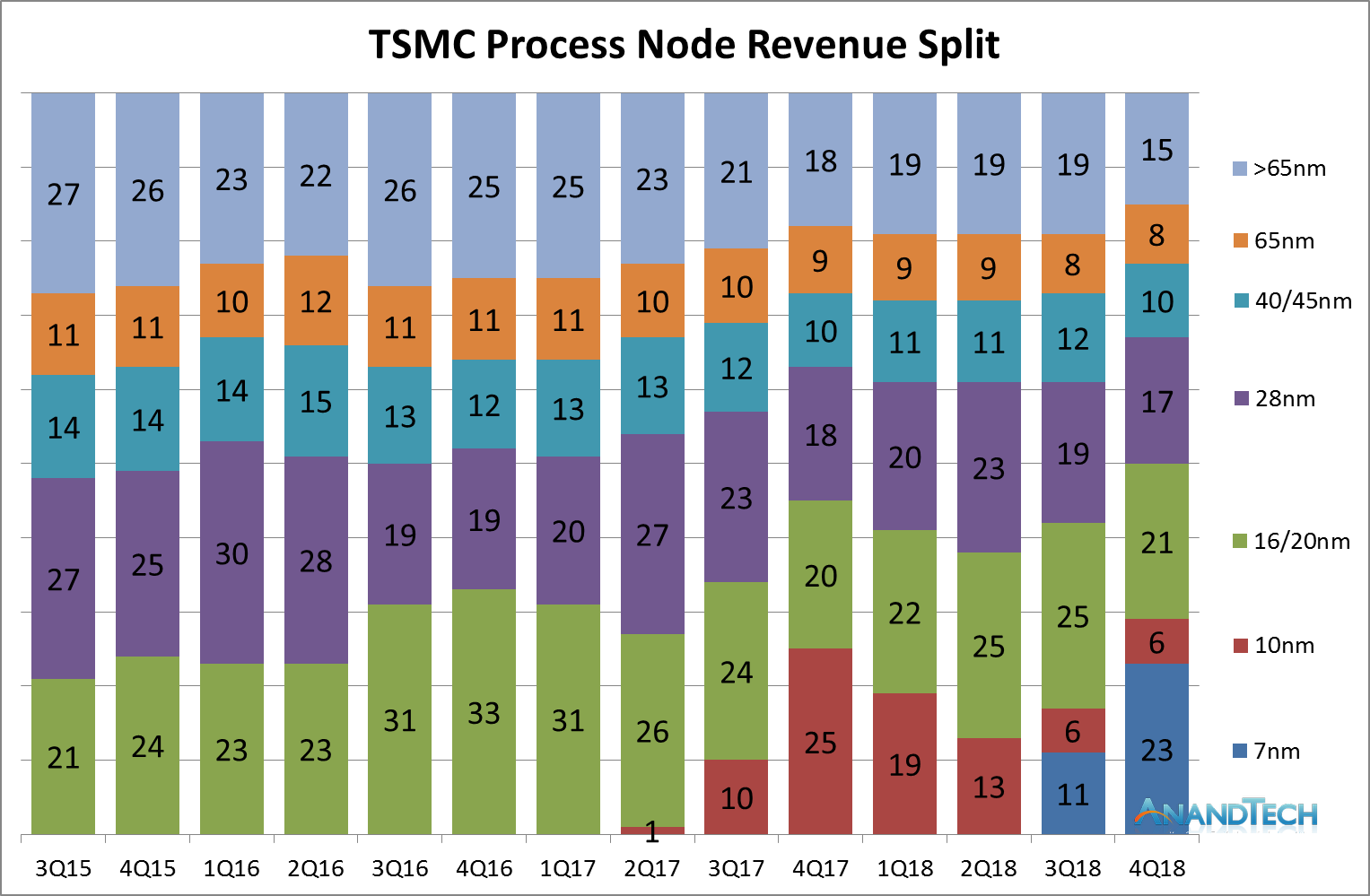

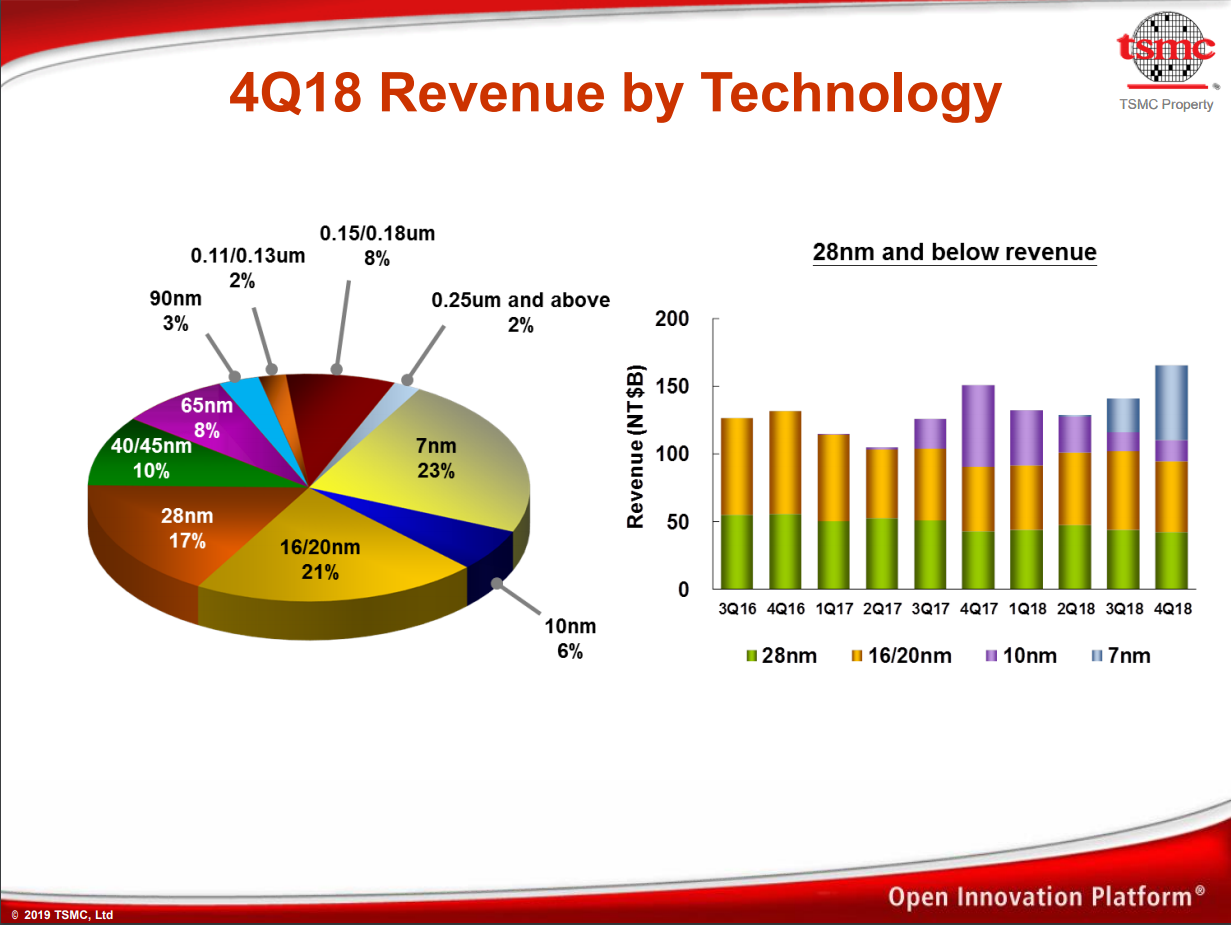

As process node technology gets ever more complex, it costs big dollars to develop and then building chips on the process is also a very costly process. The big foundries often have many process nodes running in parallel across a wide range of price brackets in order to both diversify the revenue streams but also offer multiple competitive options for the market. The latest numbers out of TSMC are stating that in Q4, the revenue generated from their leading edge 7nm node family now takes the biggest percentage of revenue for the company.

As posted by David Schor of WikiChip over Twitter, taking data from TSMC’s earning calls over the years and adding its latest Q4 results to the mix, it shows that 7nm has had a significant ramp, becoming 23% of the revenue of the company since it starting offering it as a process. Over the course of 2018, TSMC has stated that 7nm has accounted for close to 10% of total revenue, and the company expects the process node to be worth ‘greater than 20%’ of its 2019 revenue.

In the Q3 earnings call, CC Wei from TSMC stated that:

This is the first time in the semiconductor industry the most advanced logic technology is available for all product innovations at the same time. We continue to work with many customers on N7, N7+ product design and expect to see more than 100 customer product tape-outs by end of 2019 expect 7-nanometer to be a multiple waves of customer adoptions.

Trendforce has reported that TSMC held 56.1% of the worldwide market share for semiconductor foundry business in the first half of 2018, prior to 7nm being offered. Compared to other foundries, the same report has that GlobalFoundries holds 9.0% of the market, UMC at 8.9%, Samsung at 7.4%, and SMIC at 5.9%; all other players are sub 2.5%. It will be interesting to see if 7nm changes this balance.

On the future of 7nm offerings, back in August 2018, GlobalFoundries announced that it has stopped all 7nm development, that it no longer has plans to develop a 7nm process, and will focus on its current profit-generating technologies such as 14LPP, 12LP, 22FDX, and 12FDX. Also, Samsung’s 7nm offerings are starting to come online and the company has been particularly aggressive about discussing future process node technologies. We have also reported on TSMC's future plans, such as offering 5nm volume production by early 2020.

44 Comments

View All Comments

woggs - Thursday, January 17, 2019 - link

Interesting observation. The 16/20 dropped at the same time 10 peaked. Gives the appearance that some folks jumped to 10nm... then struggled... and jumped back to 16/20. Maybe their 10nm was really hard and difficult to ramp. Intel is existence proof of that possibility. The 16/20 is dropping again as 7 ramps.name99 - Thursday, January 17, 2019 - link

Not at all. Two DIFFERENT things are constantly happening.The leading edge crowd (Apple, Huawei, QC) used 10nm for a year, then moved to 7nm as soon as they could. That's the huge changes you see as each leading node comes on line.

Meanwhile everyone else, on a much less aggressive schedule, moves from one node to another in a way that's much slower and more gradual. They were likely on 28nm for 5 yrs or so, and when they finally needed better specs for their part, 16nm (ie finFETs) was the easiest next node that did the job.

woggs - Thursday, January 17, 2019 - link

That makes sense. If the plot went further back in time, might see it the 28 to 16/20 transition, too.woggs - Thursday, January 17, 2019 - link

Still... 10nm peaked and dropped long before 7 was ready. That's weird.Dvgeniy - Thursday, January 17, 2019 - link

Probably this is not the first year when Apple suddenly cuts their orders. Looks like they did the same in q1 2018.name99 - Thursday, January 17, 2019 - link

Again the timing is different from what you might think.- Manufacturing (especially for Apple) peaks a quarter or two before devices ship.

- Payment does not have to exactly match manufacturing or delivery. Either Apple or TSMC may have particular reasons (tax, revenue smoothing, whatever) for trying to shift payment forward or backward by a quarter.

- The other large 10nm players (like Mediatek and Huawei) are on their own particular schedules that might lead or trail Apple by a quarter.

All the numbers show is how the PAYMENTS flowed for 10nm vs 7nm. That's different from (not completely detached from, but different from) how the manufacturing flowed.

Dvgeniy - Friday, January 18, 2019 - link

>Either Apple or TSMC may have particular reasons (tax, revenue smoothing, whatever) for trying to shift payment forward or backward by a quarter.If Apple were prepaying, TSMC would not be complaining now about high inventory levels. Mos likely they pay on delivery.

drexnx - Thursday, January 17, 2019 - link

amazing that 10nm was such a dog of a process that it only grew in share for TWO quarters! and then even when it was still the "top" node, it proceeded to lose share two quarters before its replacement even came out. Wow.DanNeely - Thursday, January 17, 2019 - link

10nm was basically a phone only process, and q4/q1 are probably peak sales time periods for the SoCs with Q2 the nadir. Q3/4 are new iphones (late q3 is production for the release day stock), Q4 Christmas, and Q1 production for all the new Android phone releases and the end of the quarter.If it was broken out separately, I suspect you'd see something similar for 20nm; IIRC that was the last short lived phones only process.

iwod - Thursday, January 17, 2019 - link

Are there any SoC using 10nm other Apple A11? Qualcomm and Samsung SoC are all using Samsung Foundry for 10nm.The 6% revenue suggest iPhone 8 / X are still selling pretty well so far.