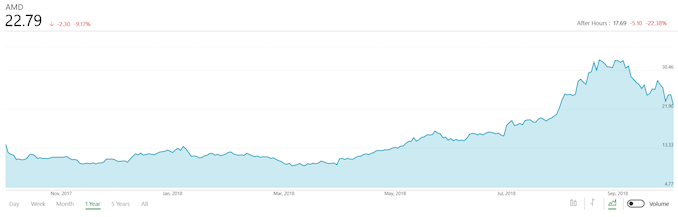

AMD Announces Q3 FY 2018 Earnings: Improving Margins, But Dogged By Crypto Decline

by Brett Howse on October 24, 2018 8:50 PM EST- Posted in

- CPUs

- AMD

- Financial Results

This afternoon, AMD announced their third quarter earnings for the 2018 fiscal year, and while there are a couple of issues they’ll have to work through, this quarter was another strong one from the company. Revenue was up 4% year-over-year to $1.65 billion, and possibly more importantly, AMD achieved a gross margin of 40%, which is up 4% from a year ago. That’s a big win for the company which struggled with margins over the last several years, dipping to as low as 29% in Q4 2014. Operating income was up 26% to $150 million, and net income was up 67% to $102 million. This resulted in earnings per share of $0.09, up 50% from a year ago.

| AMD Q3 2018 Financial Results (GAAP) | |||||

| Q3'2018 | Q2'2018 | Q3'2017 | |||

| Revenue | $1653M | $1756M | $1584M | ||

| Gross Margin | 40% | 37% | 36% | ||

| Operating Income | $150M | $153M | $119M | ||

| Net Income | $102M | $116M | $61M | ||

| Earnings Per Share | $0.09 | $0.11 | $0.06 | ||

AMD attributes the growth in gross margin to the launches of new products like Ryzen and EPYC, but also due to IP related revenue, which accounted for half of the gross margin increase. While that revenue stream may not last, even without it, 38% puts them in a much better position than they have been previously.

Looking at their segments, Computing and Graphics saw revenues climb 12% year-over-year to $938 million, and the segment had operating income of $100 million, up 37% from a year ago. Strong Ryzen desktop and mobile sales were actually offset though by lower GPU revenues with the fall of the cryptocurrency market. AMD says that blockchain revenue for this quarter was negligible, and it’s unlikely to grow with the current state of cryptocurrency. What this does lead to though is AMD having a glut of products in the channel where crypto sales haven’t happened, which is likely to impact upcoming quarters.

| AMD Q3 2018 Computing and Graphics | |||||

| Q3'2018 | Q2'2018 | Q3'2017 | |||

| Revenue | $938M | $1086M | $835M | ||

| Operating Income | $100M | $117M | $73M | ||

AMD’s other major segment is Enterprise, Embedded, and Semi-Custom, which helped them with the lean years thanks to AMD wins in both the Xbox and PlayStation. Revenue for this segment was $715 million, down 4.5% from a year ago. Operating income was $86 million, up 16.2%. The lower revenue is due to lower semi-custom product and IP related revenue, which isn’t surprising given how long the consoles have been on the market. This was offset though by increase server sales with EPYC, and the additional EPYC sales also helped with the margins, thanks to enterprise offering much better returns than consumer plays. AMD has also said their Radeon Instinct line of datacenter graphics products also were a key factor to their income growth this year.

| AMD Q3 2018 Enterprise, Embedded, and Semi-Custom | |||||

| Q3'2018 | Q2'2018 | Q3'2017 | |||

| Revenue | $715M | $670M | $749M | ||

| Operating Income | $86M | $69M | $74M | ||

Looking ahead to next quarter, AMD expects revenue to be $1.45 billion, plus or minus $50 million, and non-GAAP gross margin to be 41%.

Source: AMD Investor Relations

49 Comments

View All Comments

Yojimbo - Thursday, October 25, 2018 - link

Oooh, AMD stuffed the channel.Now the Q2 discrete GPU market share from Jon Peddie Research makes sense. How come NVIDIA knew 3 months ago that cryptocurrency demand had dried up and AMD only discovered it now? AMD gave themselves a stellar Q2 by pushing forward revenue from Q3 and Q4. Wonder what sort of insider trading has gone on at AMD over the past 3 months.

Lord of the Bored - Thursday, October 25, 2018 - link

nVidia didn't see as big a boom from the buttcoin diggers as AMD in the first place, because AMD cards are actually better at buttdigging. During the peak of the buttdigger craze, I could still find green video cards at inflated prices, but every red card of even remotely decent specs was just empty shelf space.Yojimbo - Thursday, October 25, 2018 - link

NVIDIA had roughly 50% of the revenue from crypto. The reason NVIDIA cards had greater availability is because NVIDIA had more liquidity because they owned 80% of the gaming market. They could be more certain they'd sell through the cards if crypto evaporared so they didn't have to be so conservative with their production.Regardless, it's not that important. The ethereum global hashrate shows when crypto demand dried up. And when it dried up it dried up for both NVIDIA and AMD.

Yojimbo - Thursday, October 25, 2018 - link

Oh, and another thing that shows pretty clearly that AMD is trying to he sneaky here. Even if AMD actually still saw strong crypto demand in Q2, the fact that NVIDIA's demand completely dried up in Q2 should make it impossible for them to be surprised by crypto drying up for them in Q3.neblogai - Thursday, October 25, 2018 - link

Where are you getting 'AMD is trying to be sneaky'? Their Q3 results are as expected, only with better gross margin:'For the third quarter of 2018, AMD expects revenue to be approximately $1.7 billion, plus or minus $50 million (/it is 1653M), ... GAAP gross margin to increase to approximately 38 percent (/increased to 40%), driven by the sales growth of Ryzen and EPYC products, partially offset by lower sales of GPU products in the blockchain market'.

And- it they produced more Polaris chips than needed- then that will not go to waste, as they are not releasing a replacement for them for another ~9months at least. And, a lot of their SKUs are still very much overpriced in many markets of the world, meaning- there is not enough of them being delivered.

silverblue - Thursday, October 25, 2018 - link

And yet, despite meeting or exceeding expectations, AMD's share price has tanked by a quarter within less than 24 hours, with what Business Insider describes as "AMD is getting smoked after revenue misses, guidance falls short". They must've been reading something different to the rest of us.silverblue - Thursday, October 25, 2018 - link

To clarify, I'm referring to the revenue "miss" and not the guidance.FullmetalTitan - Thursday, October 25, 2018 - link

Exact same thing happened after Q2 earnings report, for missing guidance by a few $M due to crypto demand drying up. They acknowledged that loss of market back in July, so I don't know what Yojimbo is going on about them deceiving investors with predictions of crypto profits in Q3Yojimbo - Thursday, October 25, 2018 - link

"Exact same thing happened after Q2 earnings report, for missing guidance by a few $M due to crypto demand drying up. They acknowledged that loss of market back in July, so I don't know what Yojimbo is going on about them deceiving investors with predictions of crypto profits in Q3"If they acknowledged it in Q2 then it's even worse, isn't it? Because then they should have told investors that their channel was full and the weak GPU demand should not have been a surprise.

From the Q3 conference call, Lisa Su said: "Third quarter revenue was $1.65 billion, an increase of 4% from a year ago. Looking at our Computing and Graphics segment, third quarter CG segment revenue increased 12% year-on-year, driven by significant growth in both client processor and OEM GPU sales that offset a larger-than-expected decline in channel GPU sales."

So why were the GPU sales declined larger than expected if they knew about it in Q2?

Later she reiterates: "Channel GPU sales came in lower than expected, based on excess channel inventory levels, caused by the decline in blockchain-related demand that was so strong earlier in the year."

Later, when answering a question: "We are expecting that it might take a couple quarters to completely get back to, let's call it, a normal channel. However, it is factored into our Q4 guidance."

If they knew "blockchain" was drying up then why did they fill the channel? They thought their 2 year old cards that only managed to capture 20% of the gaming market before crypto would suddenly be in high demand with gamers? And if the channel was filled because of an expectation for more sales in Q2 and they knew those Q2 sales never came then they already knew it would become filled when they made their Q2 conference call. Why didn't they tell people their channel would be filled then?

FullmetalTitan - Thursday, October 25, 2018 - link

I will give you the benefit of the doubt re: guidance on blockchain. I swear I read in their Q2 report that they had pegged crypto-related GPU sales as a "negligible component" of revenue going forward, but I can't seem to find it now.As for speculation on increased GPU production leading to an excess of inventory, I think there were multiple factors involved in that decision based on the market demands early in the quarter. I concede that they may have been bullish on blockchain demand for GPUs, but I suspect the story is more complicated, especially given that supply lead times for a GPU are ~3-4 months from wafer fab in to packaging/shipment. Unless they had actually adjustment production well ahead of the Q2 report then we would only expect the bump in volume to hit shelves around September, a time frame that sets them up for failure because of NVIDIA announcements of Turing.