Intel Announces Q2 2018 Results: Setting More Records

by Ryan Smith on July 27, 2018 9:00 AM EST- Posted in

- CPUs

- Intel

- Xeon

- Financial Results

All across the hardware industry 2018 is shaping up to be a banner year for earnings, and the 800lb gorilla that is Intel is no exception. Reporting their Q2’2018 earnings yesterday afternoon, Intel booked $17.0B in revenue for the quarter, setting another new Q2 revenue record for the company. Meanwhile net income, while not being noted as a record for the company, was still very high at $5.0B. This puts Intel well ahead of itself both on a year-over-year and sequential basis, topping Q1’2018 and Q2’2017, both of which were also record quarters. All told, Intel’s both Intel’s revenue and net income for the quarter increased by $2.2B year-over-year, while against Q1 they’re up $0.9B and $0.5 respectively.

Meanwhile Intel’s all-important gross margin has held relatively steady at 61.4%, which is down two-tenths from Q2’2017, but up from the previous quarter.

| Intel Q2 2018 Financial Results (GAAP) | |||||

| Q2'2018 | Q1'2018 | Q1'2017 | |||

| Revenue | $17.0B | $16.1B | $14.8B | ||

| Operating Income | $5.3B | $4.5B | $3.8B | ||

| Net Income | $5.0B | $4.5B | $2.8B | ||

| Gross Margin | 61.4% | 60.6% | 61.6% | ||

| Client Computing Group Revenue | $8.7B | -3% | +6% | ||

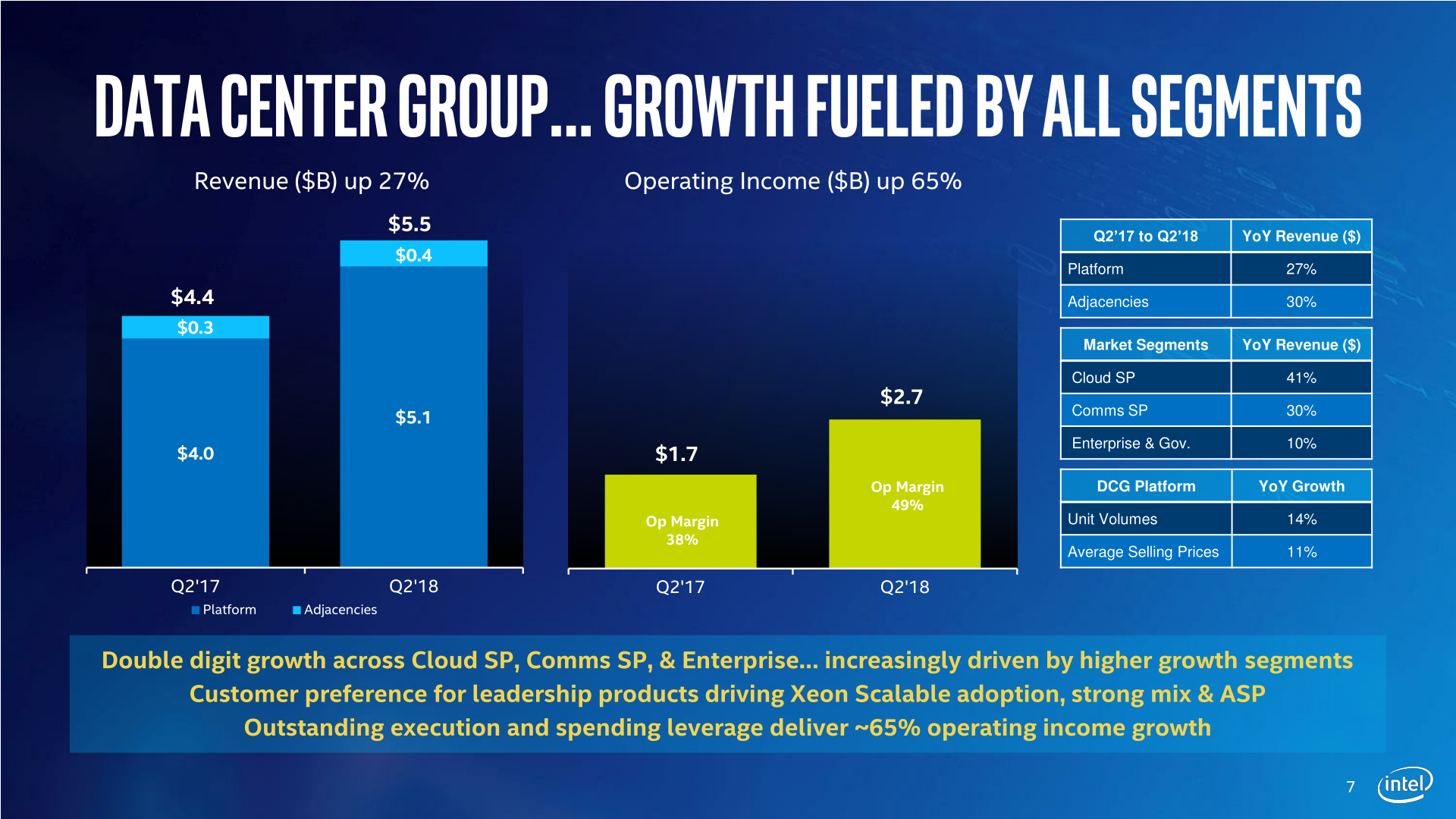

| Data Center Group Revenue | $5.5B | +6% | +27% | ||

| Internet of Things Revenue | $880M | +5% | +22% | ||

| Non-Volatile Memory Solutions Group | $1.1B | +10% | +23% | ||

| Programmable Solutions Group | $517M | +4% | +18% | ||

Breaking down the numbers by Intel’s various business groups, all of Intel’s groups saw revenue growth for the year. This ranges from 6% for the client computing group, up to 27% for the data center group. And even on a less-comparable quarterly basis, every group except CCG has seen some growth.

Overall Intel has been making a concentrated effort to pivot towards (or at least play up) what the company sees as the segments primed for growth – which Intel is calling its “data-centric” business – and isolate it from the “PC-centric” client computing group. Looking at revenue growth it’s easy to understand why; client computing revenue has been slow to move for years now, while Intel’s other businesses have grown much faster, and as an added kicker are generally more profitable too. None the less, Intel can’t ignore the fact that the client computing group alone makes up more than half of the company’s revenue. However at the rate things are going, this might be one of the last quarters where that is true.

On the client computing front, Intel is citing the commercial and enthusiast segments as being the driving factors for the growth, which is unsurprising as the two have been consistent performers with higher-than-average spending. Beyond that, Intel hasn’t broken down client computing revenue by form factor or such this quarter, so unfortunately we don’t get any insight into how the recently launched Coffee Lake mobile parts have done.

Besides being a more stagnant space, the biggest challenge Intel faces with the client computing group right now is in fact the company’s biggest challenge, which is the stalled development of their 10nm process. As part of today’s earnings call the company has announced that they are still on-track for 10nm mass production in 2019, however they aren’t expecting complete systems to reach store shelves until the holiday shopping season. Which means Intel will be relying on their 14nm technology and resulting products for the next 12 to 15 months, which is going to make it harder to entice already fickle consumers into upgrading.

The news is of course happier with Intel’s other business, all of which have grown at a much greater rate. Intel continues to sell Xeon processors to server vendors and cloud server providers at a good clip, with revenues there improving by 27% year-over-year. And yet even with that growth, Intel actually missed analyst expectations by 2%, indicating just how hot this business segment really is: there’s clearly still very high demand for server processors. Going forward however, Intel is going to be facing off with AMD and EPYC, which is finally finding its footing. So it will take a lot of work to sustain this growth, especially as according to Intel’s own accidentally published roadmaps, the company won’t have 10nm-class Xeons read until 2020, which means Intel will likely be playing defense against AMD starting in 2019.

The rest of the “data-centric” business is a similar upbeat story. FPGA sales are up, non-volatile memory sales are up, and even IoT sales are up. The reasons are varied, but overall NAND prices have been good and the drive for neural networking hardware is helping sales on both the FPGA (cloud) and IoT (edge) sides.

Overall then, based what has now been two strong quarters of growth for Intel, the company is expecting the rest of the year to go similarly. And indeed at this point they’re expecting 2018 as a whole to be their third consecutive record year. Which is especially impressive at a time where Intel’s core manufacturing advantage has increasingly slipped away. Conversely however, there remains the lingering question of whether Intel can sustain this kind of growth for the next year without their next-generation fabrication technology.

Source: Intel Investor Relations

27 Comments

View All Comments

grahad - Friday, July 27, 2018 - link

You live in an adamantium bubble of your own making, you deluded fool.HStewart - Friday, July 27, 2018 - link

"You live in an adamantium bubble of your own making, you deluded fool."Comments like sound like it comes from WCCFTech.

Just for information, I found an Erratum in IBM 486SLC - in my first job. I have down Operating System development

sa666666 - Friday, July 27, 2018 - link

You really are delusional. And I seriously doubt your technical abilities and what jobs you've actually done in the past. And you can't spell correctly in English, it seems. You really do belong at WCCFTech.HStewart - Friday, July 27, 2018 - link

I didn't say my English was all that correct - in fact I was in with Football players at Ga Tech.One problem with this website is does not allow edits of messages so they can be corrected.

And to be honest, it really does not matter if you believe my jobs from past - but in this erratum, the IBM 486SLC processor had the cache on processor inverted but only jumping between 286 and 386 protected mode. Back in those days we did not ICE ( in circuit emulators ) and the way it was resolved was spreading out instructions to parallel port and when last led came on, I knew where the program crash.

eva02langley - Friday, July 27, 2018 - link

Intel stock drop because Intel is having trouble with their 10 nm process. However what really burned investor is the fact that Intel will not release a 10 nm Xeon until 2020. Stop deluding yourself, AMD stock gained 20% in two days. At this point I doubled my investment.HStewart - Friday, July 27, 2018 - link

I believe Intel drop was from loosing it CEO and not from 10 nm - I would say it part of it, but amount AMD Gain is insignificant compare to income that Intel pulls in.Demigod79 - Friday, July 27, 2018 - link

No, it was not because of Intel "loosing" its CEO - that happened weeks ago and investors are always forward looking (if you knew anything about the stock market then you would know this). There's no reason to expect an event that happened weeks ago to suddenly affect stock prices now.The drop was because they underperformed in the data center business and because of the delay with the 10nm tech (which further puts the data center business in jeopardy). The various downgrades of Intel stock my Wall Street firms was also about concerns about their future products and growth due to their troubles with 10nm.

eva02langley - Friday, July 27, 2018 - link

It is not the money they made, it is the money they are going to make in the future. AMD is about to get into an A64 era all over again, and Intel drop the ball for countering them.https://www.cnbc.com/2018/07/27/intel-plunges-on-c...

"The setup is for Advanced Micro Devices to control both the architectural and process node aspects of the x86 [processor] market for years to come; a dynamic we have never seen before and structurally destructive for Intel's business model. We reiterate our Sell rating," Rosenblatt Securities wrote in a note on Friday. The analysts noted that Intel could lose its "near monopolistic position in CPUs that allowed for increased ASPs."

Maxiking - Saturday, July 28, 2018 - link

AMD future is highly uncertain. The Athlon 64 era took 3 years, then they got destroyed by Core2. Now, it is a second good year for AMD. So ironically, if Intel fix their 10nm, it will be those 3 years again.Watch out what you wish for. The situation is different now. A64 was better, P4 was a disaster. Ryzen isn't even able to match Intel, be it mainstream or HEDT. They are slower and are able to compete by setting be being cheaper and adding more cores.

There is very big if. While AMD is on a good way and the future looks more or less bright but IF Intel fix their 10 nm, AMD is done. Intel will introduce the new architecture and will start "glueing" their cpus together as much as AMD do now. And at that moment, any AMD advantage will be gone.

FreckledTrout - Sunday, July 29, 2018 - link

I am way more optimistic on AMD. AMD were always at a manufacturing disadvantage even Athlon 64 days Intel moved to 90nm months after Athlon 65 came out on 130nm. Now AMD are on "12" nm it is still GloFlo's lpp process that does not scale up to high frequencies. That disadvantage ends this year when EPYC's start rolling out on TSMC's 7nm and next year when Ryzen is made on GloFlos 7nm. This feels totally different than in the Athlon 64 days where AMD is and where they are heaing. AMD partners are competitive at the manufacturing process maybe even a a little ahead of Intel, chip design of Zen is damn good and AMD is going mobile, desktop and server. I understand why you are cautious I just think you are wrong.