Cryptomining Demand Drives Exceptionally High Graphics Card Shipments in Q2 2017

by Nate Oh on August 25, 2017 2:00 PM EST

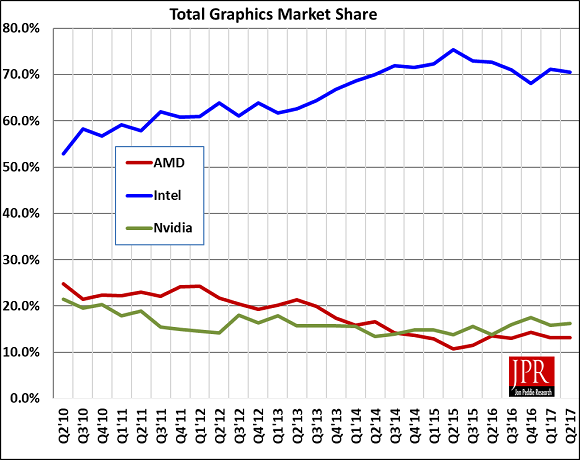

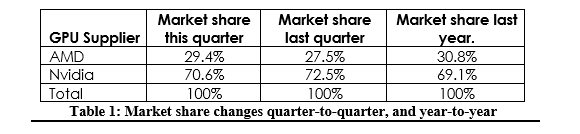

This week, Jon Peddie Research (JPR) reported significantly higher discrete GPU shipments for Q2 2017, attributing the historically unprecedented increase to cryptocurrency mining, specifically to Ethereum mining. As opposed to the cryptocurrency mining demand of a few years ago, JPR notes that the ASIC-resistant nature of Ethereum mining has especially encouraged GPU mining. In terms of discrete desktop graphics market share, AMD gained a few percentage points from NVIDIA, bringing the current balance to AMD’s 29.4% versus NVIDIA’s 70.6%.

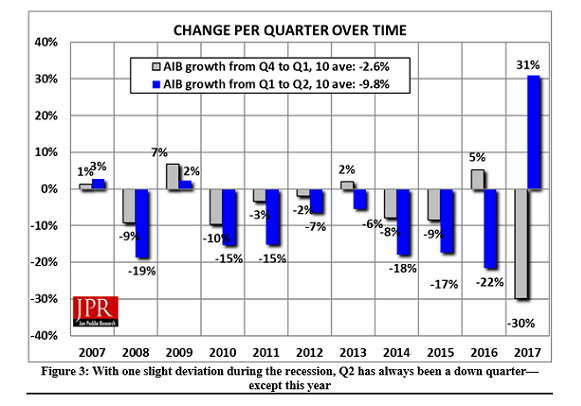

In context, the GPU and PC markets fluctuate in a relatively consistent seasonal pattern: shipments trend flat to down in Q1, notably down in Q2, notably up in Q3, and up to flat in Q4. According to JPR, Q2 2017 has seen an unprecedented 31% increase in discrete GPU shipments from Q1, the first time in over eight years that Q1-to-Q2 shipments have seen an increase at all. Discounting the minor increases during the recession, Q2 has always been the seasonally weak quarter for graphics card shipments.

Drawing a contrast to the limited Bitcoin and Litecoin mining impact on 2013 shipments, JPR identifies the memory-intensive Ethash, Ethereum’s hashing algorithm, as deterring ASIC development for Ethereum mining, and in turn any sudden GPU-displacing bust. That is, during the Bitcoin boom, low cost ASICs displaced GPUs. Consequently, JPR does not see a repeat of market cannibalization by used mining cards. While the diminishing return-on-investment (ROI) will eventually flatten out Ethermining-fueled GPU demand, this quarter saw a direct and significant Ethermining/cryptomining impact on discrete graphics demand.

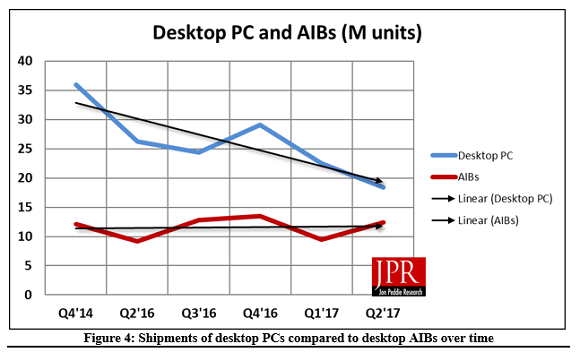

On the back of that cryptomining demand, discrete GPUs have regained market share over integrated GPUs (iGPUs). Weak iGPU and desktop PC shipment numbers continue to reflect the overall declining PC market, while the high-end gaming PC sector continues to be the bright spot for the market. Overall, GPU shipments increased by 7.2% from last quarter.

Vendor-wise, JPR reports that AMD’s overall unit shipments increased 7.8% quarter-to-quarter, Intel’s shipments increased 6.3%, and NVIDIA’s shipments increased 10.4%. As mentioned earlier, AMD did gain market share in discrete desktop graphics, but still remains below last year’s market share level.

For AMD, their market share is back to Q2 2016 levels of around ~30%. The past year has seen launches of NVIDIA’s Pascal-based consumer cards, as well as of AMD’s Polaris-based RX 400 and 500 series cards; of the latter, the Polaris-based cards were explicitly a volume-play, and did not target the high-end market. To that end, the GTX 1070 and above did not have competition until this month, with AMD’s launch of RX Vega cards, and on the face of it, while Polaris has improved AMD's market share against NVIDIA, it has not made a dramatic difference. As the next few months roll on, the RX Vega cards, as well as Vega 11-based cards, will play a large role in AMD’s aspiring return to its historical 35% – 40% discrete desktop GPU market share.

For cryptomining demand, the remarkable impact on discrete graphics shipments does match up with general reports of mainstream graphics card shortages. When we looked at the discrete graphics market in Q2 and Q3 of 2016, the cryptocurrency mining demand then was nothing like this quarter. Now that the Ethereum mining mania has been quantified into numbers, it has revealed some of the context and reasoning behind cryptomining cards, cryptomining motherboards, and Radeon Pack bundles. And what the numbers reveal is that Ethereum GPU mining has been ridiculous in every sense of the word.

While Ethereum itself will die down eventually, it is anybody’s guess if GPU cryptomining booms will be firmly part of graphics card economics.

Source: Jon Peddie Research

46 Comments

View All Comments

Yojimbo - Friday, August 25, 2017 - link

I want to clarify something I said. The percentage of people looking to buy SOME newly released game who only have an iGPU may be greater than 12%. But the percentage of total games sales by people with only an iGPU is probably less than 12%. Those with dGPUs are buying more games (and probably paying more for their games: buying higher priced games and buying them as soon as they come out instead of waiting for the price to fall).In any case, a demand for graphically-demanding games does exist. If companies started making their games to cater to less demanding hardware it would open up the market for other companies to swoop in and cater to the users willing to pay more money for better-looking games. This is supported by the fact that gamers have actually been increasingly willing to spend more money for GPUs as time goes on, not less.

someonesomewherelse - Saturday, October 14, 2017 - link

Or hope that the Ryzen apus wont be to shitty since AMD actually has relatively decent iGPUs and now with Ryzen decent cpus to. As long as neither part is cut down too much they should make okish gaming chips for undemanding gamers.jjj - Friday, August 25, 2017 - link

Was looking today at prices, Nvidia seems to have caught up with demand but AMD is not even close.This means that AMD will be losing massive share in gaming and they need to push prices down even if that means that everything is OOS.

StrangerGuy - Monday, August 28, 2017 - link

AMD's only saving grace here is there are still clueless mining bandwagoners still clearing out their GPU supply even at prices that make zero sense because they still believe that "AMD + mining = gud" and "NV + mining = bad" meme.blppt - Tuesday, August 29, 2017 - link

Thats all well and good for now, but AMD spends money on endorsing game developers with their "Gaming Evolved" program, which is kind of pointless if nobody can buy your cards to game on.Plus, eventually this mining crazy will fall off, and if you piss off gamers into buying in-stock Nvidia cards, you hurt yourself that way as well. My guess is that AMD is having trouble manufacturing enough supply for the cards, not that they are intentionally doing anything to limit output right now.

JanW1 - Friday, August 25, 2017 - link

I'm surprised no one mentions the fact that GPU demand was _down_ 30% in Q1 2017 wrt Q4 2016, whereas shipments tend to trend flat between Q4 and Q1. So this really looks like mostly shipments were delayed from Q1 to Q2 2017.Yojimbo - Friday, August 25, 2017 - link

Shipments do not tend to be flat between Q4 and Q1. They send to be down close to 20%. They were down a bit more than what is seasonal. There was a glut of graphics cards in the channel during Q1, so supply was fine. Shipments weren't delayed. Therefore any "delay" would have to be on the side of demand. What would be your explanation for such an unusual "delay" to have taken place this particular Q1? It flies in the face of the notion of seasonal normality.JanW1 - Friday, August 25, 2017 - link

Where did you get the -20% from? Q4 to Q1 never was below -10 over the past 10 years prior to 2017.I'm just looking at the data in the article. First image:

"AIB growth from Q4 to Q1, 10 ave: -2.6%" (which is nowhere near the -20% you claim)

"AIB growth from Q1 to Q2, 10 ave: -9.8%"

That is the 10-year average baseline. Note that this is a cumulative -12.4% from Q4 to Q2.

Now the article discusses the +31% from Q2 2017, comparing it to the -9.8% average - a huge outlier. We're talking about a sudden +40% in graphics card production and sales wrt what was expected. Thing is, the -30% from Q4 to Q1 in 2017 is also a huge outlier in the opposite direction. Q4 2106 to Q2 2017, we get a cumulative +1%. Now all of a sudden, we are just talking about a +13% over what was expected. Not the same thing.

The article seems to argue that there was an unexplained huge drop in sales in Q1 and a completely unrelated insane cryptomining boom in Q2 for a single cryptocurrency (to support this, at least some parallel chart of ether supply or similar info would be needed).

I'm just saying that without more info, it would seem more plausible to assume that the Q1 and Q2 outliers are related. That could be either a simple technical reason of some sales being attributed to Q2 rather than Q1 in the data, delayed purchase decisions, whatnot.

Yojimbo - Friday, August 25, 2017 - link

I got it from something I remembered from something an analyst said in a conference call, I believe 18% was the number. But it was talking about revenue, and specifically about NVIDIA's Q1 revenue. NVIDIA's Q1 is February, March, and April. JPR might be using calendar year Q1 which is January, February, and March (not sure). OK, forget about that. I shouldn't have said it, my mistake. Assume a 3% decline from Q4 to Q1 on average as in the chart.There was a 30% decline this past Q4 to Q1. But it wasn't from a lack of supply. It was from a lack of demand. It's not reasonable to just assume that the Q1 and Q2 outliers are related. You need a reason. For what reason would large numbers of people be putting off purchases from Q1 to Q2? Why should it be different from seasonal norms? Anxiety about the economy? I don't think there was much. Expectation of a new product coming into market? The only product thought to be coming was Vega. In Q1 people thought Vega might come in Q2. Then in Q2 people knew Vega would be coming Q2 and Q3. Why would people who are waiting for new products purchase old products once they were sure a new product really was coming very soon? That doesn't make sense. Note that Vega Frontier Edition reviews didn't come out until Q2 was over.

Then consider that we do know why Q2 demand was strong. AMD and NVIDIA both said that cryptocurrency mining had a big impact in Q2. NVIDIA showed about $200 M of revenue sold to large crypto mining operations that they listed in their "OEM & IP" segment. That's independent of seasonal norms, it's direct market information. Q1 was not weak because of lack of cryptocurrency demand, since strong crypto currency demand is not normal. So there is good reason to believe Q1's weakness and Q2's strength are unrelated.

It's a good guess there would have still been weakness in discrete desktop graphics cards sales in Q2 without cryptocurrency sales, but we'll never know for sure. But the idea that Q2 demand was strongly affected by cryptocurrency mining is known from other sources. It's not just inferred from total unit shipments.

Nate Oh - Friday, August 25, 2017 - link

JPR argues for the insane cryptomining boom in Q2, which is what the article cites. For both Q1 (https://jonpeddie.com/press-releases/details/add-i... and Q2 2017 AIB reports, JPR does not go beyond saying that the -30% is "seasonally understandable," amidst a generally declining PC market. In the general graphics Q2 report (https://jonpeddie.com/press-releases/details/moder... JPR describes the trend as a return to seasonality, rather than a drastic outlier. What JPR does imply is that the post-recession cycle and the tablet incursion may be factors in why seasonality has not been normal.We do not have access to the full paid JPR market reports, but it is highly unlikely that there is a hidden reason that JPR would not mention in the press releases and public reports. On the face of it, JPR has previously signaled the Q4 to Q1 drop is for mundane and/or seasonal reasons. And JPR in the Q2 2017 AIB report does not connect the Q1 to Q2 rise and Q4 to Q1 drop together at all. Because they have not stated or implied that the two outliers are related, this makes it difficult for the article to assume so without data, especially in light of a report that is explicitly data-driven.