Intel Announces Q1 2017 Financial Results: Record Quarter

by Brett Howse on April 27, 2017 10:00 PM EST- Posted in

- CPUs

- Intel

- Financial Results

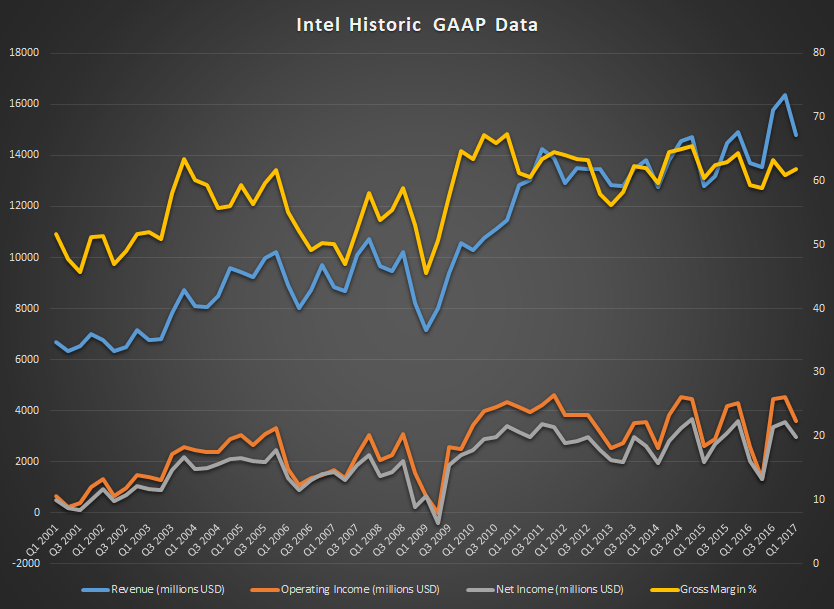

Today Intel announced their earnings for Q1 of their 2017 fiscal year, and the results were good. Intel delivered record revenue for the quarter, of $14.8 billion, up from $13.7 billion a year ago. Intel is a company that loves their margins, and they were once again over 60% for the quarter, coming in at 61.8%, which is 2.5 percentage points higher year-over-year. Operating income was up 40% to $3.6 billion, and net income was up 45% to $3.0 billion, which resulted in earnings-per-share of $0.61 for the quarter, also up 45% from a year ago. This is even though Q1 2016 was 14 weeks, versus 13 weeks in 2017.

| Intel Q1 2017 Financial Results (GAAP) | |||||

| Q1'2017 | Q4'2016 | Q1'2016 | |||

| Revenue | $14.8B | $16.4B | $13.7B | ||

| Operating Income | $3.6B | $4.5B | $2.6B | ||

| Net Income | $3.0B | $3.6B | $2.0B | ||

| Gross Margin | 61.8% | 60.9% | 59.3% | ||

| Client Computing Group Revenue | $7.976B | -12.6% | +5.7% | ||

| Data Center Group Revenue | $4.232B | -9.34% | +5.8% | ||

| Internet of Things Revenue | $721M | -0.7% | +10.8% | ||

| Non-Volatile Memory Solutions Group | $866M | +6.1% | +55.5% | ||

| Intel Security Group | $534M | -2.9% | -0.6% | ||

| Programmable Solutions Group | $425M | +1.2% | +18.4% | ||

| All Other Revenue | $42M | -35.4% | -16% | ||

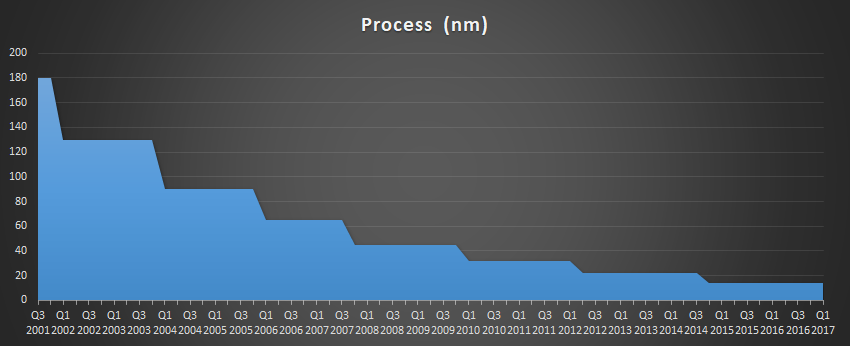

Intel’s Client Computing Group continued to have gains, with revenue for the quarter up 6% to $7.976 billion. Significantly for Intel, operating income for this segment jumped from $1.885 billion a year ago, to $3.031 billion this year. While we’ve seen the company forced to slow down its movement to smaller processes, the current 14nm node has been well refined and the Kaby Lake processors have been solid performers. The next generation 10nm node is looking very promising though, with Intel claiming 25% better performance and 45% lower power consumption versus Kaby Lake thanks to the density improvements.

The Data Center Group also had gains, with revenues up 6% year-over-year to $4.232 billion, although the growth has slowed somewhat. Operating income for the group was $1.487 billion for the quarter, down from $1.764 billion a year ago. This will be an interesting space to watch with increased competition in both the x86 and ARM space, but Intel will be releasing new Xeon chips as well with a change in branding.

The Internet of Things Group continued to show gains as well, with revenue up 11% year-over-year to $721 million, and up 35% since Q1 2015, so in two years they have seen some substantial growth in this segment.

Non-Volatile Memory Solutions Group had the largest jump in revenue, with revenue up 55% to $866 million. However, this group also saw an operating loss increase to $129 million, compared to a $95 million loss a year ago. This should be an exciting segment to watch though with Intel bringing their Optane products to market, with both the DC P4800X SSD and Optane caching memory. If you haven’t checked out those reviews yet, they are well worth the read, and 3D XPoint definitely brings some advantages even on a Gen 1 product.

Intel’s Security Group is showing its final mention in their earnings, since Intel’s divestiture of the group closed on April 3, 2017, and subsequently it will fall in to the “All Other” category starting next quarter. Revenue for this group was pretty flat, at $534 million, compared to $537 million a year ago. Operating income was up to $95 million though, from $85 million last year.

The Programable Solutions Group, which is Intel’s FPGA segment, had a revenue increase of 18% to 425 million, and an operating income of $92 million, compared to an operating loss of $200 million a year ago.

Finally, the All Other category had revenues of $42 million and an operating loss of $1.082 billion.

Looking towards next quarter, Intel is forecasting revenues of $14.4 billion, plus or minus $500 million, and a gross margin around 62%, give or take a couple of points.

Source: Intel

21 Comments

View All Comments

asodfngoinaios - Monday, May 1, 2017 - link

Well, obviously. AMD has only released enthusiast desktop chips so far. Would anyone sensible expect Zen to hurt Intel in markets where it doesn't compete at all?We'll see what happens when the server and mobile parts drop in a few months. Based on how dominant Ryzen is for the enthusiast desktop market, I expect it to do pretty well.

zepi - Friday, April 28, 2017 - link

Ryzen was launched on 2nd of March. It wouldn't have much time to impact intels sales yet.bcronce - Sunday, April 30, 2017 - link

Intel's R&D budget is 3x AMD's gross revenue. I'm sure AMD will impact Intel, but there is a large difference of scale between them.Meteor2 - Friday, April 28, 2017 - link

Obvious Zen isn't going to affect Intel overnight. But I think 2017 will be Intel's best year, as it gets the most out of 14 nm, for a long time in the future. Their microarchitecture lead is disappearing to IBM, AMD and ARM, their FPGA (and Phi) stuff doesn't really compete with Nvidia, and GlobalFoundary's decision to skip 10 nm to work on cracking a real 7 nm means their process lead may have gone by 2020.Gondalf - Friday, April 28, 2017 - link

To IBM?? ....come on LOL ex Big Blue has lost any grip and most of the revenue. To AMD? assuming Intel will stand without doing nothing. ARM ? yes in handset.GloFo?? this is the more funny statement. Right now GloFo has not the track record and the technology to steal the process lead to UMC, you figure Intel. GloFo is manufacturing under license and a nice pertentage of revenue goes to Samsung.

Your words are fine for TSMC or Samsung.

name99 - Friday, April 28, 2017 - link

"The next generation 10nm node is looking very promising though, with Intel claiming 25% better performance"Seriously? You believe that? Good luck...

(And the site that's making the claim seems to be broken. When I click on the link all I get is a spinning cursor...)

Intel have officially said that they expect the first round of 10nm transistors to be slightly SLOWER than their now optimized 14nm transistors. Which means that to get 25% improvement they'd need either a dramatically improved IPC or a dramatically rebalanced pipeline that can sustain higher frequencies. Both would be an enormous departure from their pattern over the last ten years or so.

------

"Finally, the All Other category had revenues of $42 million and an operating loss of $1.082 billion."

Way to bury the lede! Loss of $1 billion on $14 billion of revenue is not nothing...

What exactly is being hidden in that All Other? Is that where the MobilEye purchase gets accounted for? (That was $15 billion, but I don't know the details of how that splits into cash vs shares, or the schedule of payments.)

Gastec - Sunday, August 20, 2017 - link

The "All Other" is and has always been related to CEO and board "activity" :)LuckyWhale - Friday, April 28, 2017 - link

62% margin, huh?!! I guess that's the profit margin you command when you have little competition because you blocked or killed all competition through underhandedness years ago. Hope Ryzen does its best to lower that shameful number somehow.patrickjp93 - Saturday, April 29, 2017 - link

Given IBM's profit margin on their own products is in the 300% area, 62% is nothing.anoldnewb - Sunday, April 30, 2017 - link

profit margin = profit / sales (revenue) it rarely exceeds 100%