Intel Reports Q1 2015 Earnings: Lower PC Sales And Higher Data Center Revenues

by Brett Howse on April 14, 2015 11:00 PM EST- Posted in

- CPUs

- Intel

- Financial Results

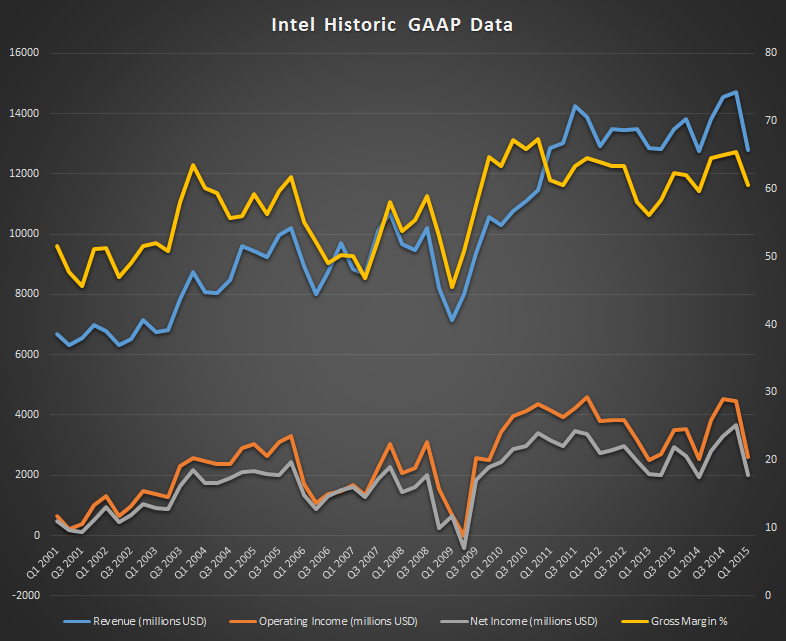

Intel released their Q1 2015 earnings today. The company posted revenues of $12.8 billion USD for the quarter which is down 13% from Q4 2014, and flat year-over-year. Gross Margin was 60.5%, which is up 0.9% over Q1 2014 and down 4.9% over last quarter. Operating Income came in at $2.6 billion, and Net Income was $2.0 billion, which was up 3% over Q1 2014 and down 46% as compared to their last quarter. Earnings per Share was $0.41, which is up 8% year-over-year and down 45% quarter-over-quarter.

There are a couple of notes to make about this year’s reporting structure. Last November it was made known that the Mobile division would merge with the PC Division. The Mobile division has long been a source of large operating losses mostly due to the contra revenue plan to boost Atom sales in tablets. It also should mean that mobile becomes as big of a priority for Intel as the PC CPU space, which should benefit the company in the long term with the push to lower power devices. For Q1 2015, Intel is no longer reporting the Mobile division as a separate reporting structure, and instead it will be combined into the Client Computing Group.

The new numbers will of course reflect this, so any year-over-year comparisons will also be compared with like-for-like data.

| Intel Q1 2015 Financial Results (GAAP) | |||||

| Q1'2015 | Q4'2014 | Q1'2014 | |||

| Revenue | $12.8B | $14.7B | $12.8B | ||

| Operating Income | $2.6B | $4.5B | $2.5B | ||

| Net Income | $2.0B | $3.7B | $1.9B | ||

| Gross Margin | 60.5% | 65.4% | 59.6% | ||

| Client Computing Group Revenue | $7.4B | -16% | -8% | ||

| Data Center Group Revenue | $3.7B | -10% | +19% | ||

| Internet of Things Revenue | $533M | -10% | +11% | ||

| Software and Services Revenue | $534M | -4% | -3% | ||

| All Other Revenue | $615M | 0% | +13% | ||

That being said, the Client Computing Group did not have an excellent quarter. Declining PC sales due to the slowing of corporate customers performing Windows 7 migrations has put a damper on this group. Revenue for the group was $7.4 billion, which is down 16% from last quarter, and down 8% from last year. Breaking the numbers down a bit further, desktop platform volumes were down 16% year-over-year, which is a pretty sharp decline. At the same time, the average selling price for desktop platforms went up 2% to help offset this loss. Notebook platforms on the other hand were up 3% year-over-year, but the average selling prices of notebook platforms went down 3%. Tablet volumes were up 45% as compared to Q1 2014. Compared to Q4 2014, the entire group had revenue down 16%, platform volumes down 18%, and average selling prices up 1%.

The Data Center Group had almost the polar opposite, with revenue of $3.7 billion which is up 19% year-over-year, with platform volumes up 15%, and average selling prices up 5%. Compared to Q4 2014, revenue was down 10% with volumes down 7% and average selling price also down 3%.

The Internet of Things group is still relatively small at Intel, but posted an 11% year-over-year growth with revenues now coming in at $533 million. This is a 10% drop as compared to Q4 2014.

Software and Services is roughly the same size of overall business as IoT, with revenues at $534 million, which was down 3% year-over-year and 4% quarter-over-quarter.

The “All Other” segment which includes non-volatile memory (NAND flash memory), SoCs for wearables and emerging computing, and corporate expenses had revenues of $615 million, up 13% year-over-year and flat quarter-over-quarter.

Intel bought back 26 million shares in Q1, meaning they have repurchased 203 million shares back since Q1 2014.

In Q2 we should start to see the new Atom chips come to market, and devices like the Surface 3 have already been confirmed to be running the latest 14 nm Atom chip. Also, there should be some talk of Skylake, which is the next Intel Core architecture, although details may be scarce until Q3.

On the financial side, Intel is forecasting revenue of $13.2 billion plus or minus $500 million for Q2, with a Gross Margin of 62%. For the full year, Intel is expecting revenue to remain flat.

Source: Intel

11 Comments

View All Comments

TheJian - Sunday, April 19, 2015 - link

This decline is because they keep having to give away 4.1B a year to compete with ARM...LOL. By NVDA Intel, or slowly die as other fabs take you over, your profits continue to shrink (allowing them to spend more than you on fabs), and you just get weaker and weaker over time. As profits go, so does R&D at some point. It won't be long (another year of polish on android 64bit probably) and Intel will be facing a fully loaded ARM PC, with power that is good enough (say 70-100w chip desktop/15-40w laptops) to steal some REAL market share in laptop/PC. ARM can double the size of their current dies on a newer process shortly and slap a heatsink/fan on them to run at 3.5-4.5ghz just like Intel at roughly the same wattage top to bottom. The difference is they'll sell them for $200 or so vs. Intel's 350 i7 Devils canyon etc. They'll probably have dual/tri boots of Android64, linux (some format, ubuntu? redhat? etc), and maybe SteamOS by then. Changing the cpu/windows out will further hurt DX12/WINTEL monopoly, and cut a full PC price by $200-300. I'm talking all the same parts of a PC, discrete NV card and all. Just a change of cpu/windows. This will happen right in time for all the unreal 4 engine (unity 5, etc) games that push arm up into the desktops and finally out of mobile. Then come the apps (games first, then apps) that can use such a PC.Either Intel/MS buys NV or the have zero defense soon to a huge swath of users who've never used WINTEL (grew up on mobile/android or ios). Those younger people (and some old I guess) will opt for a far cheaper PC with good enough SOC in it, or for more power by one with NV Discrete cards too (with 8-32GB, SSD's, HD's, 500-1000 psu's etc etc). Of course they may have to bid against google, samsung, apple and possibly even amazon. I think that's about all that would be interested, with amazon probably not as good of a fit and least likely buyer. Perfect fit for Google or Samsung as both sell devices, samsung has fabs (and about to lose a patent case that could be really bad), google could switch to NV's FAR cheaper car solution, gaming chips for their nexus devices & gain gaming chops adding tegrazone (since google is pushing gaming on android as fast as possible) along with great server stuff from NV for datacenter, grid stuff etc. Intel/NV hate each other so maybe it's only a bidding war with MS/Goog/Samsung really. Or maybe Jen just thinks they'll win in the end anyway on gaming, as AMD goes down further and they end up suing the crap out of everyone in patent suits on mobile while they all try to catch NV game experience with devs, drivers etc.

Things are about to get very rough for WINTEL's side, with signs it's been happening for quite a while already. You know you have problems when you start hiding your mobile losses. MS doesn't just give away their next OS for nothing either. ;) FEAR. Too late though, I think the sheer numbers of android is too large (MS responded far to late) and another shrink or two of chips, new revs and games galore+more polished 64bit OS and this whole market gets turned on it's wintel head. Pro stuff will hang out longer on wintel obviously, but they could easily both lose a huge part of general market share (people who browse, get email. game, play with photos, etc).