Understanding AMD's Semi-Custom Strategy

by Anand Lal Shimpi on September 5, 2013 5:51 PM EST

With Microsoft’s acquisition of Nokia we are now living in a world where all three major client OS providers (Apple, Google and MS) all own/are device companies. Samsung gets an honorary seat at the table by virtue of making devices as well as most of the components inside those devices (and fabbing the ones they don’t make), on top of adding a fair bit of software customization of their own. That makes four companies with the ability to control most of the market, what happens to everyone else?

Both Google and Microsoft have stated publicly that acquiring device companies doesn’t mean that they want to stop working with outside partners. Naturally that’s what you’d expect Google and Microsoft to say to avoid overly angering existing partners shipping existing devices. In the long run however, companies like Acer, ASUS, Dell, HP, HTC, Lenovo and LG (among others) will find themselves in an interesting position, competing against their OS suppliers that also happen to be vertically integrated device makers.

I don’t expect that we’ll immediately transition to a world where there are only four brands of smartphones, tablets and notebooks. I suspect that all of the existing players, vertically integrated or not, will do their best to maintain/grow marketshare despite the threat of real consolidation. After all, a threat alone isn’t enough to force companies out of a market.

When faced with a very large competitor, you need a broad set of partners. It’s all of these other companies that AMD views as potential candidates (including Samsung it seems) for its semi-custom approach to silicon manufacturing.

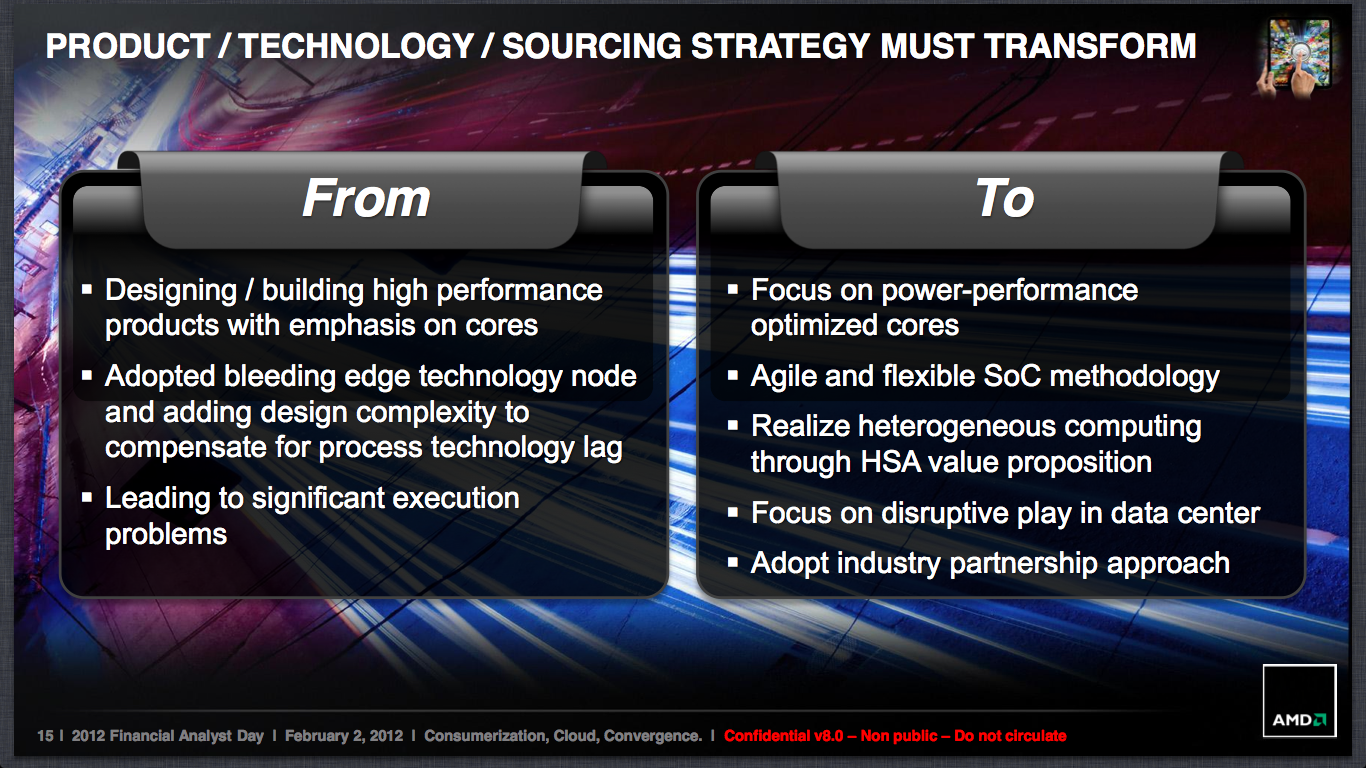

Last year AMD’s new CEO Rory Read talked about delivering semi-custom silicon, similar to what AMD does in game consoles, to OEMs who want to differentiate. At the time I didn’t really get how this strategy would work but I think I now have better insight into the theory. If we assume that Apple and Samsung will remain major players in the consumer device space, both of these companies have heavily invested in developing their own software and SoCs. If you’re an OEM looking to compete with either (or both), you need the same assets. As a company that isn’t Apple or Samsung however, you don’t have the resources to truly integrate vertically and become a silicon manufacturer as well as run a profitable business. AMD hopes that there will be at least a couple of enlightened players in the device space who realize they need a silicon strategy to differentiate but don’t have the resources/expertise/desire to become a silicon player.

The idea here is that AMD would then provide those OEMs with a semi-custom SoC, where they could choose their own IP blocks (video decode/encode, CPU cores, GPU, etc...), and help give them competitive parity or ideally even an advantage over the larger players. Counting on the bigger guys having higher overhead, being less agile and having to make larger profits should, at least on paper, give the smaller players a fighting chance.

It took me a while to understand AMD’s semi-custom strategy, but seeing how things have shaken up over the past few months I think I can understand it a lot better than what it was first floated at AMD’s Financial Analyst Day last year.

The other thing I think I understand a lot better now is why former Lenovo President & COO, Rory Read, was chosen as the man to run AMD. I’ve met most of the new guard at AMD and generally came away quite impressed. The challenge set in front of them is nothing short of insane, but the company has put together a good combination of leaders and visionaries to at least stage a comeback. The big unknown for me was always Rory. Until a few months ago I’d never even met the guy - I’d only heard him speak to analysts, and the nature of those conversations just wasn’t up my alley.

I finally had the opportunity to speak with Rory a few months ago in Austin in a much more candid setting. It was during that meeting that he laid out his strategy for AMD, and it was then that I understood why he was there.

Rory’s playbook for AMD is actually very similar to how he ran things at Lenovo. Lenovo was stuck in a similar position not too long ago: it had a relatively high margin enterprise business that it used to fund and grow a much lower margin consumer business. The new AMD strategy is quite similar.

Traditional margins on x86 CPUs are nothing short of tremendous. The fabless semiconductor manufacturers that compete with Intel don’t operate on anywhere near the same margins. AMD used to play in the same space Intel did, and as a result was often viewed as disappointing as their margins wouldn’t hold up. The problem was that although AMD shed its fab burden, its margins were always viewed as needing to be up at Intel levels. That perception has to change.

Rory’s strategy is to use high margin revenues from existing markets (e.g. PC client, GPUs) and use it to fund a low cost structure expansion into new markets. On paper it’s a sound approach, but the unexpected quick decline of AMD PC sales/shipments threw a wrench in the plan.

The company had to shrink in order to deal with lower than expected revenues than what Rory had planned on when he first took the job almost two years ago. Based on what Raja Koduri told me after he joined a few months ago, it seems like it’s working:

“Raja returns to a very different AMD than the one he left. I asked him what’s different and he responded by saying the AMD he left acted like a company that was 10x its size. Today, AMD is a much smaller and more agile company. Raja believes AMD is in a better position to take advantage of new opportunities vs. being in the hopeless position of never being able to catch up in mature markets.”

So you take the higher margin PC revenues, and use them to invest in lower cost products in new markets. Rory expects semi-custom silicon to see heavy use in these new markets by the way. Lower cost typically means lower margin, which is something the new AMD is ok with. Making Intel margins (or even traditional AMD margins) is tough, in these new markets AMD just needs to be making better margins than the ARM players as the company transitions from being fully PC supported, to PC + additive revenue from these new markets and finally to a position where AMD’s revenues are dominated by these new revenue sources. What are the new markets in specific? Getting anyone at AMD to answer that question today is tough, but I suspect the first place to look is among all of those other players I talked about earlier. The companies tasked with competing with these vertically integrated powerhouses could rely heavily on AMD.

At the end of the day, Rory Read is at AMD because he knows how to navigate a low margin business and run it efficiently to the point where he can use gains in one area to fund another (at Lenovo he took China and Commercial sales to buy him more wiggle room in consumer client). I finally get the plan, now all that’s left is to see if it’ll work.

51 Comments

View All Comments

Hrel - Tuesday, September 10, 2013 - link

I think this is the right approach for AMD. Good to see them finally diversifying. Still, I'd love to see them reach per core parity with Intel, on a performance/watt basis. Or at least within 10%, given their manufacturing disadvantage.